Introduction

Picture this: an autonomous semi-truck merges into your lane on I-10, clips your vehicle, and sends you to the hospital. When you ask who's responsible, the answer isn't a name — it involves a software company, a fleet operator, a sensor manufacturer, and an insurance market that wasn't built for any of this.

That confusion is real, and it's becoming more common. Aurora launched commercial driverless trucking operations in Texas in 2024. Torc, Gatik, and others are expanding deployments across multiple states. The technology is moving faster than the legal and insurance frameworks designed to handle it.

This guide covers three things:

- Who bears legal liability when an autonomous truck crashes

- How insurance claims work differently when the "driver" is software

- What payout factors actually matter for victims and fleet operators alike

TLDR

- Liability can fall on the AV technology provider, the trucking company, parts manufacturers, or a human operator — sometimes all at once

- Standard commercial truck policies may not cover software defects, AI decision failures, or cyberattacks

- Multiple deep-pocketed defendants and long-term injuries can push recoveries well above typical truck crash settlements

- Black box data from the autonomous system is the most critical evidence in any AV accident claim

- Most AV fleet operators carry policies with coverage gaps they haven't identified yet

Who Is Liable When an Autonomous Truck Crashes?

Traditional truck accident liability starts with one question: what did the driver do wrong? Autonomous truck cases don't have that anchor. The entire system comes under scrutiny — the software, the hardware, the company that deployed it, and everyone involved in its operation.

No public court ruling has definitively resolved how fault divides among AV system providers, carriers, and manufacturers in a commercial trucking crash. What exists is a framework built from traditional negligence law, product liability doctrine, and a growing body of legal commentary — applied to facts that courts are still encountering for the first time.

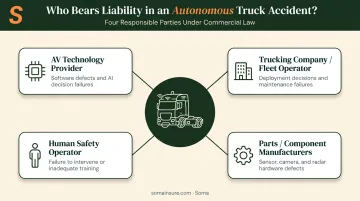

Potential Liable Parties

The AV Technology Provider: When the software makes a faulty decision — misreading lane markings, failing to detect a pedestrian — the company that designed and deployed it faces product liability exposure. The 2018 Uber fatality in Tempe, Arizona (a passenger vehicle, not a truck) was an early signal that technology providers cannot disclaim responsibility simply because the vehicle was in autonomous mode.

The Trucking Company / Fleet Operator: Carriers cannot escape liability by replacing a human driver with automation. A company's decision to deploy autonomous technology is likely treated as acceptance of the operational risk it creates. That exposure grows when the carrier:

- Failed to maintain software updates

- Operated outside the system's approved Operational Design Domain (ODD) — the defined geographic, weather, and road conditions the ADS was designed for

- Skipped manufacturer-required system checks

The Human Safety Operator: Many current autonomous trucks require a human monitor — in the cab or remotely. Distraction, failure to intervene, or inadequate training creates negligence exposure for both the operator and their employer, alongside the AV provider.

Parts and Component Manufacturers: Sensors, cameras, radar arrays, and braking systems can fail independently of the software. Each manufacturer of a defective component can be named as a separate defendant — expanding both the pool of liable parties and the total insurance coverage available.

Comparative Fault Still Applies

In some states, a victim's own contribution to the accident reduces or eliminates recovery. Georgia's modified comparative fault rule under O.C.G.A. § 51-12-33 bars recovery entirely if the plaintiff is 50% or more responsible.

Fault must be apportioned by percentage among all parties — including nonparties like maintenance contractors. That rule applies in AV cases the same as any other.

How Insurance Works Differently for Autonomous Truck Accidents

Standard commercial auto liability policies were written assuming a human driver. When the "driver" is an algorithm, those policies develop real gaps — particularly around software defects, AI decision failures, and product liability events that a standard commercial auto form may exclude entirely.

Product Liability vs. Operator Liability

The central insurance question in any AV truck crash is: was this a driver error or a technology defect?

- Driver/operator error → the carrier's commercial auto policy typically responds

- Technology defect (software bug, sensor failure) → the claim may need to flow through the AV developer's product liability policy instead

In many accidents, both policies are triggered simultaneously, creating multi-party coverage disputes where each insurer argues the other should pay first.

Specialized AV Insurance Products

The market is catching up. Two developments worth tracking:

- Liberty Mutual and TuSimple announced a partnership in May 2021 to study Level 4 autonomous truck safety and develop tailored insurance solutions for scaled deployments

- Travelers currently markets insurance specifically for autonomous vehicle technology companies, including business auto coverage and CyberRisk Tech products

Some insurers are developing autonomous vehicle endorsements that cover:

- AI decision-making failures

- Remote monitoring system failures

- Cybersecurity breaches affecting vehicle control systems

- Software update errors that alter driving behavior

The No-Fault Discussion

A separate policy debate is underway. According to RAND's research on autonomous vehicles and auto insurance, regulators and industry advocates are exploring no-fault compensation frameworks where victims receive payment regardless of fault — funded jointly by technology providers and fleet operators. No federal law has codified this framework yet, but the structure matters for how future claims may be filed and settled.

Coverage Gap Awareness

For fleet operators running AV trucks today, the practical risk is straightforward: most standard commercial trucking policies were not written with autonomous systems in mind, and exclusions for software failures or AI decisions may go unnoticed until a claim is denied.

Soma works with carriers across trucking and technology sectors to help fleet operators identify those gaps, then places coverage with carriers that specifically address AV operations — including cyber liability for connected vehicle systems.

What Insurance Payouts Look Like: Damages You Can Claim

The categories of compensable damages in an autonomous truck accident largely mirror those in traditional truck crashes. What changes is the scope of recovery: multiple liable parties mean multiple insurance towers, which can increase total compensation beyond what a single-defendant case would produce.

Economic Damages

These are the quantifiable losses:

- Medical expenses — emergency care, surgery, rehabilitation, assistive devices, and ongoing treatment costs

- Lost wages — current income lost during recovery, plus future earning capacity if the injury is disabling

- Property damage — repair or replacement value of the damaged vehicle

Long-term and disabling injuries can push claim value well beyond baseline figures. According to the Insurance Information Institute, the average auto bodily injury liability claim reached $28,278 in 2024 — but severe trucking injuries involving multiple surgeries, permanent disability, or extended rehabilitation push settlements far beyond that baseline.

Non-Economic Damages

These are harder to quantify but often represent the largest share of total recovery in serious cases:

- Pain and suffering from the physical injuries

- Emotional distress and anxiety

- PTSD — documented by NIH research as a frequent outcome after severe vehicular crashes, and compensable in personal injury cases across most jurisdictions

- Loss of enjoyment of life

Documenting psychological treatment — therapy records, psychiatric evaluations, prescription history — is essential to recovering PTSD-based damages. Without that documentation, insurers and defense attorneys will minimize or dispute the claim entirely.

Fatal crashes follow a different recovery path entirely.

Wrongful Death Claims

When an autonomous truck accident is fatal, surviving family members may recover:

- Funeral and burial expenses

- Loss of financial support

- Loss of companionship and consortium

AV wrongful death cases frequently target the technology company as a deep-pocketed additional defendant. Uber's confidential settlement with the Herzberg family in 2018 (reached quickly after a driverless vehicle fatality) suggests that technology companies may prioritize early resolution to avoid rulings that set adverse legal precedent across their entire industry.

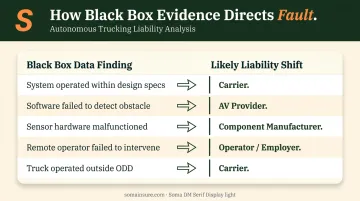

The Role of Black Box Data in Claims and Liability Disputes

Every autonomous truck generates a continuous stream of sensor data, camera footage, and AI decision logs. In the seconds before a crash, that data captures the truck's speed, sensor classifications, system alerts, and whether any human operator intervened.

That record is the most important evidence in any AV accident claim — and also the most contested.

What the Data Can Prove

Depending on what the logs show, liability shifts in different directions:

| Data Finding | Likely Liability Shift |

|---|---|

| System operated within design specs | Toward carrier's maintenance and operational decisions |

| Software failed to detect obstacle | Toward AV technology provider |

| Sensor hardware malfunctioned | Toward component manufacturer |

| Remote operator failed to intervene | Toward operator and their employer |

| Truck operated outside ODD | Toward carrier for unauthorized deployment |

Access and Disclosure Tensions

Technology providers often assert proprietary rights over their algorithms and internal data logs. Victims and their attorneys need that same data to prove the system failed.

Disclosure requirements vary by jurisdiction. Key regulatory checkpoints include:

- Federal (NHTSA): Mandatory crash reporting for ADS-equipped vehicles under the Standing General Order on Crash Reporting; a voluntary transparency evaluation program was proposed in 2024

- Texas: One of the most active AV trucking states, with recording device obligations and serious bodily injury reporting requirements built into its AV authorization framework

Practical advice: Request preservation of the truck's data through legal counsel immediately after an accident. AV data logs may be overwritten on a rolling basis, and delay can permanently destroy the most critical evidence in your case.

What Autonomous Trucking Operators Must Know About Coverage

Fleet operators deploying autonomous trucks are almost certainly running ahead of their insurance coverage. Standard commercial truck policies weren't written for this risk, and most carriers haven't updated their underwriting appetite to match it.

That gap has real consequences. A single AV accident could expose a fleet operator to:

- The victim's full damages across all categories

- Legal defense costs across multiple suits (against the carrier, the ADS developer, and potentially both)

- Regulatory fines for operating outside FMCSA or state AV authorization requirements

- Reputational and operational consequences if the incident triggers regulatory review

Coverage Stack for AV Fleet Operators

Operators should evaluate whether they carry all four layers:

- Primary commercial auto liability — updated or endorsed to explicitly include AV operations; verify it doesn't exclude software-driven incidents

- Product liability — critical if the operator is also integrating or customizing AV technology onto the vehicle

- Cyber liability — covers remote system hacks, ransomware affecting vehicle control software, and connected fleet data breaches (NMFTA research on heavy-vehicle cybersecurity identifies serious vulnerabilities in connected commercial vehicle systems)

- Umbrella / excess liability — Class 8 trucks carry enormous loss potential; standard primary limits are frequently inadequate in severe injury cases

Soma works with trucking companies and technology-integrated fleets to place coverage across all four layers — sourcing quotes from carriers that already understand AV risk, including Markel, Chubb, and Kinsale, so operators aren't waiting on brokers learning the account type from scratch.

Frequently Asked Questions

Who is liable if a self-driving semi-truck crashes?

Liability can fall on the AV technology provider, trucking company, software developer, hardware manufacturers, or a human safety operator — and multiple parties often share fault at once. Investigators determine the split by analyzing sensor data, maintenance logs, software version records, and the truck's Operational Design Domain documentation.

How much can you get in a settlement after being hit by a semi-truck causing long-term injuries and PTSD?

Payouts vary based on injury severity, liable parties, and available coverage. Documented PTSD and long-term injuries raise non-economic damage awards considerably, and AV accidents often yield higher recoveries because they pull in multiple deep-pocketed defendants — technology companies included — across separate policies.

Does regular commercial truck insurance cover autonomous vehicle accidents?

Standard commercial auto policies frequently exclude software defects, AI decision errors, and product liability events. Fleet operators should review their policies for AV-specific exclusions and consider specialized endorsements or standalone autonomous vehicle coverage before deploying any automated driving technology.

What evidence should I collect after an autonomous truck accident?

Gather the police report, photos of the scene and all vehicle damage, and contact information for witnesses. Seek medical evaluation promptly — including for psychological symptoms. Above all, have an attorney formally request preservation of the truck's black box and sensor data before it is overwritten or withheld under proprietary claims.

Can the trucking company's insurance deny a claim if a software defect caused the crash?

Yes. Insurers may deny the carrier's policy by arguing the crash was a product defect rather than an operational failure. Legal and insurance professionals who understand AV liability can redirect the claim through the technology provider's product liability coverage, where it may properly belong.

What states currently allow fully driverless commercial trucks on public roads?

Texas, Arizona, and Florida are the most permissive, each allowing fully autonomous commercial operation when authorization requirements are met. California permits heavy-duty AV testing and deployment through a permit system rather than blanket approval. Operators must confirm state-specific authorization before each deployment regardless of where they run.