In May 2025, Aurora launched commercial driverless heavy-duty trucking on the Dallas-Houston corridor — completing over 1,200 driverless miles with no safety driver aboard. Gatik has been running fully driverless middle-mile deliveries for Walmart in Arkansas since 2021. This isn't a future scenario. It's happening now, on public roads, with commercial freight.

The problem: standard commercial auto policies assume a licensed human driver sits behind the wheel. When no one does — or when an algorithm is making the driving decisions — the question of who pays for an accident becomes genuinely unresolved. Courts are working it out case by case. Regulators are writing rules state by state. And most existing trucking policies haven't caught up to either.

This guide breaks down the liability shift, the regulatory patchwork, how insurance products are evolving, and what your business needs to do before your next policy renewal.

TL;DR

- Liability is shifting from drivers to manufacturers and software developers, and most existing auto policies don't cover that

- No federal AV insurance law exists; state rules vary wildly, with minimum coverage thresholds ranging from $2M to $5M in some states

- Underwriters now evaluate technology profiles, route certifications, and cybersecurity posture instead of driver MVRs

- Premiums won't drop soon; expensive sensor repairs and scarce claims data keep costs elevated for now

- Audit your current policy for AV-related exclusions — autonomous operation, tech failures, and cyber — before any deployment

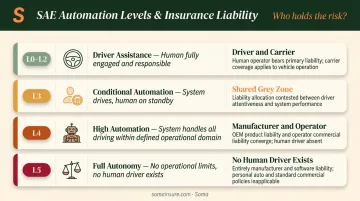

What SAE Automation Levels Actually Mean for Your Insurance

The SAE's six-level framework (L0 through L5) determines whether your existing policy covers a claim or your insurer denies it. Understanding where your vehicles fall on that scale is a coverage question, not just a technical one.

Here's how the levels map to insurance exposure:

| SAE Level | What It Means | Who's Primarily Liable |

|---|---|---|

| L0–L2 | Driver assistance; human must remain fully engaged | Driver and carrier |

| L3 | System drives, but human must be ready to intervene | Shared — grey zone |

| L4 | System handles all driving within a defined route/domain | Manufacturer + operator |

| L5 | Full autonomy, no operational limits | No human driver exists |

The inflection point for insurance purposes is L4. At this level, the Automated Driving System (ADS) performs the driving task and handles fallback responses within its Operational Design Domain. Aurora's commercial Texas operation runs an SAE L4 system — meaning the vehicle is certified to operate without human input on specific routes.

Most commercial autonomous trucks operating today sit at L4 within corridor-specific routes, sometimes with a safety driver on standby. That "supervised autonomy" creates a liability overlap: both driver liability and product liability can apply to the same incident simultaneously, and most standard policies aren't written to handle that split.

Why this matters for your policy:

- The automation level determines which insurance product is triggered

- It affects who is listed as the named insured

- It controls what evidence is required to file — or contest — a claim

Before your next renewal, confirm the certified SAE level for each vehicle in your fleet — and ask your broker whether your current policy language explicitly addresses that level. Policies written for L2 operations don't automatically extend to L4 deployments.

The Liability Shift: From the Driver's Seat to the Tech Stack

Why Traditional Policies Break Down

Commercial trucking insurance is built on one foundational assumption: human error causes accidents. FMCSA's Large Truck Crash Causation Study found driver-related critical reasons in 87% of crashes where the large truck was assigned the critical reason. The entire actuarial model — premiums, loss ratios, indemnification structures — is calibrated to that baseline.

When an algorithm is driving, that baseline disappears. No uniform federal framework has emerged yet. Insurers, courts, and regulators are each developing their own approach — often in conflict with one another.

Three Legal Theories Now in Play

Attorneys handling autonomous truck accident cases are currently working through three primary theories:

- Products liability — defective hardware or software caused the crash; the manufacturer is responsible

- Negligence — the operator failed to intervene when required, or skipped a software update; the fleet is responsible

- Vicarious liability — the trucking company is held responsible for the AV's actions as an extension of its commercial operations

Fleet owners and owner-operators face exposure under all three simultaneously.

The Multi-Party Problem

A single autonomous truck accident can involve multiple responsible parties with overlapping liability:

- The trucking company (operational decisions, route authorization)

- The AV software developer (algorithm behavior)

- The sensor manufacturer (hardware defects)

- The fleet manager (failure to apply software updates)

No single commercial auto policy was designed to coordinate liability across that chain. That gap is compounding a separate plaintiff strategy: attorneys are arguing that autonomous systems should have prevented any crash — meaning manufacturers may face exposure even when the AV system wasn't the direct cause.

In response, several carriers are now adding AV-specific indemnification carve-outs that explicitly exclude coverage for algorithm-driven decisions, shifting that exposure back to the technology provider.

Drivers Aren't Off the Hook Yet

Drivers haven't been fully absolved. California, Florida, Texas, and New York all maintain requirements — in various forms — that operators remain capable of taking manual control during supervised autonomous operations. That means driver negligence claims remain live alongside product liability claims during this transition period.

The Regulatory Patchwork: State Laws, Federal Gaps, and What's Coming

No Federal Standard Exists

The SELF DRIVE Act passed the House in 2017 but was never enacted. The AV START Act didn't become law either. NHTSA proposed a voluntary framework called AV STEP in January 2025, but it carries no binding requirements. For now, trucking companies operating across state lines must navigate 50 different state-level approaches — many of which conflict.

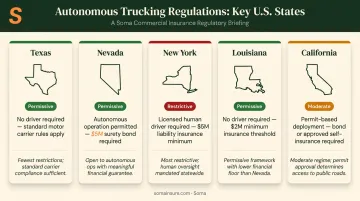

Key State Contrasts

The variation isn't minor. It's fundamental:

| State | Human Driver Requirement | Insurance/Bond Minimum |

|---|---|---|

| Texas | Not required if statutory conditions met; ADS treated as operator | Standard motor carrier requirements |

| Nevada | Fully autonomous operation permitted if requirements met | $5M bond or insurance for testing |

| New York | Licensed driver physically present required | $5M insurance policy required |

| Louisiana | No conventional driver required if statutory conditions met | $2M liability coverage minimum |

| California | Permit-based; heavy vehicles now authorized but tightly regulated | Bond or self-insurance certificate required |

A truck leaving Dallas in full legal compliance can become non-compliant (or uninsured) the moment it crosses into a more restrictive state. For any interstate operator, that's an active exposure, not a theoretical one.

What a Federal Framework Would Change

When federal AV legislation eventually passes, it will likely standardize:

- Minimum liability coverage thresholds by automation level

- Liability allocation rules between operators and manufacturers

- Mandatory crash data disclosure requirements

- Uniform definitions of "operator" when no human is present

U.S. lawmakers are also studying the UK's Automated Vehicles Act 2024, which requires insurers to pay accident victims first and then recover from vehicle makers. A similar shift in the U.S. would fundamentally restructure how commercial trucking policies are written and priced.

Until that federal framework exists, route-by-route compliance reviews aren't optional — they're the minimum due diligence for any fleet running autonomous trucks across state lines.

How Insurance Products Are Evolving for Autonomous Fleets

The Product Shift

Standard commercial auto policies focus almost entirely on driver behavior. They review MVRs, accident histories, and CDL experience. For autonomous operations, that review process is becoming irrelevant.

Munich Re notes that AV trucking underwriting now requires evaluation of technology maturity, safety validation, operational design domain, cybersecurity protocols, and regulatory permissions — none of which appear in a traditional trucking submission.

What Underwriters Are Now Asking For

Instead of a driver list and MVR pull, expect underwriters to request:

- Sensor types and redundancy configurations (LiDAR, radar, cameras)

- Software provenance and version history

- Total autonomous miles logged, supervised vs. driverless

- Operational Design Domain documentation (which routes, weather conditions, speed ranges)

- Cybersecurity protocols and incident response procedures

- Remote monitoring capabilities and staffing

Fleets that can't produce this documentation should expect coverage denials, steep premium increases, or both.

Premium Outlook: Short-Term vs. Long-Term

Premiums are unlikely to fall soon. Several factors are keeping costs elevated:

- Sensor replacement costs are substantial (LiDAR arrays, radar systems, camera clusters)

- Actuarial loss data for autonomous trucking is nearly nonexistent

- Legal uncertainty around liability allocation makes claims unpredictable

- State-specific minimums in testing jurisdictions start at $2M–$5M

RAND and Deloitte both project that as autonomy matures and safety data accumulates, risk will migrate away from human-error claims toward technology and product liability — potentially reducing per-mile costs long-term. But that transition is measured in years, not months.

New Coverage Types to Know

In the meantime, the market is adapting. When reviewing or shopping for coverage, ask about:

- AV-specific commercial auto liability — hybrid policies blending auto and product liability

- Cyber insurance riders — covering hacking, data breach, and remote system compromise

- Usage-based / per-mile insurance — premium tied to telemetry data rather than flat annual rates

- Embedded insurance — bundled with AV platform subscriptions from technology vendors

- Product liability endorsements — explicitly covering software failure as a covered peril

These products are still maturing, and not every carrier offers all of them. One caution on self-insurance: some large autonomous fleets are absorbing accident risk internally rather than purchasing third-party policies. For smaller operators without substantial capital reserves, a single large claim under this model can threaten the business entirely.

What Trucking Businesses Should Do Now

Step 1: Conduct an Immediate Policy Audit

Pull your current commercial auto, general liability, and cargo policies and look specifically for:

- Exclusions referencing "autonomous operation" or "automated driving systems"

- Technology failure exclusions that could apply to sensor or software malfunctions

- Cyber event exclusions that might extend to vehicle systems

- Language requiring a "licensed operator" in the vehicle at the time of loss

Most legacy policies contain language written before autonomous trucks existed. A claim filed while the ADS was engaged could be denied on a technicality buried in the exclusions section.

Step 2: Review Your Vendor Contracts

If you're working with an autonomous technology provider, your agreement with them matters as much as your insurance policy. Confirm:

- Who assumes liability when the ADS is engaged

- What warranties apply to software performance and update obligations

- Whether the vendor carries adequate product liability insurance

- Who controls data access after an incident for claims purposes

Gaps in these agreements don't just create legal uncertainty — they can shift full liability onto the fleet operator by default.

Step 3: Find a Broker with Specialty AV Market Access

Those contract and policy gaps point to the same problem: standard commercial lines brokers typically don't have access to the specialty carrier capacity needed to write AV-related exposures. Getting the right coverage requires someone who understands both commercial trucking and the autonomous vehicle insurance market.

Soma places coverage for trucking fleets operating across multiple states with non-standard risk profiles. With direct access to carriers including Markel, Kinsale, Chubb, and others, Soma can identify where your current policy falls short and place the right coverage before a claim exposes the gap.

Frequently Asked Questions

Who is liable if an autonomous truck causes an accident?

It depends on the SAE level and the failure's cause. At lower automation levels, the driver and fleet carrier bear primary responsibility. At L4, claims shift toward the AV manufacturer or software developer — though fleet operators typically remain in the claim chain, and multiple parties are often named in the same case.

Do owner-operators still need commercial truck insurance if the truck drives itself?

Yes. Physical damage, cargo, and auto liability coverage remain required at every automation level. The obligation doesn't disappear; it expands — semi-autonomous operations add technology-related exposures on top of traditional requirements, especially when operators are expected to monitor or take manual control.

What states currently allow commercial autonomous truck operations?

Texas, Nevada, Louisiana, and Arizona are among the most permissive states for driverless commercial truck operations. New York requires a licensed driver present; California regulates heavy-duty AVs under separate permit rules. Requirements vary by route, so verify each state on your run — not just your home state.

How will autonomous trucks affect commercial insurance premiums?

Short-term, expect premiums to hold steady or rise — sensor repair costs are high and actuarial data is thin. Longer term, analysts including RAND and Deloitte project per-mile cost reductions as safety records build and risk shifts away from human error. Volatility is more likely than a predictable trend during the transition.

What types of insurance coverage do autonomous trucking fleets actually need?

The core package includes AV-specific commercial auto liability, product liability covering software and hardware failures, cyber insurance for hacking and data breach scenarios, and cargo coverage. These may need to be coordinated across multiple policies or bundled into a single AV-specific program — standard mono-line policies typically won't cover all four exposures.

How are insurers underwriting autonomous trucks differently from traditional fleets?

Underwriters are moving away from driver-based criteria — MVRs, accident histories, CDL records — toward technology-based criteria. Expect requests for sensor specifications, autonomous miles logged, Operational Design Domain documentation, cybersecurity protocols, and remote monitoring capabilities. Fleets that can't produce this technical documentation will find coverage harder to place and more expensive when they do.