Many fleet operators know commercial auto coverage is required. Fewer understand how directly it affects their ability to keep vehicles moving, absorb accident costs, and maintain contracts. A gap in coverage doesn't just create a compliance problem — it creates an operational one.

This article breaks down why commercial auto insurance is operationally essential for fleet operations, what the real cost of inadequate coverage looks like, and how to structure a policy that actually matches your risk.

TL;DR

- Commercial auto insurance is legally required for business-owned vehicles in nearly every U.S. state — personal auto policies explicitly exclude business-use vehicles

- Consolidated fleet policies reduce administrative overhead and per-vehicle cost versus managing separate policies for each vehicle

- FMCSA regulations (49 CFR Part 387) set federal liability minimums at $750,000+ for many for-hire carriers — real verdicts regularly exceed that

- Operating without coverage exposes a business to uncapped liability, vehicle downtime, regulatory penalties, and contract disqualification

What Is Commercial Auto Insurance for Fleet Operations

Commercial auto insurance covers vehicles owned or leased by a business — providing three core protections:

- Liability coverage — bodily injury and property damage to third parties

- Physical damage coverage — repairs or replacement for the business's own vehicles

- Medical payments — costs for occupants injured in a covered accident

It's a distinct product from personal auto insurance, which explicitly excludes vehicles used primarily for business purposes. The Insurance Information Institute confirms this: if a vehicle is used primarily in business, a personal auto policy likely provides no coverage at all.

Fleet coverage is a specific structure within commercial auto. Rather than managing a separate policy per vehicle, fleet coverage consolidates all business vehicles under a single contract: one renewal date, one billing cycle, one claims contact. Some carriers apply this structure starting at two vehicles; others require five or more.

A fleet policy doesn't just simplify paperwork. When a driver causes a serious accident, adequate commercial auto coverage means the insurer absorbs liability claims, vehicle repairs, and legal defense costs. Without it, those costs land directly on the business's balance sheet.

Key Advantages of Commercial Auto Insurance for Fleet Operations

Financial Protection Against High-Cost Liability Claims

Fleet vehicles — trucks, vans, cargo carriers — generate accident claims that can exceed what most businesses can absorb out of pocket. Commercial auto liability coverage handles third-party medical bills, property damage, and legal defense when a fleet driver causes an accident. That coverage is what keeps a bad day from becoming a business-ending event.

The numbers here are stark. ATRI research found that the average verdict in large-truck crash cases above $1 million grew from $2.3 million in 2010 to $22.3 million in 2018 — a 51.7% annual increase, compared to 1.7% standard inflation over the same period. Cases with verdicts above $1 million rose 235% between 2005–2011 and 2012–2019.

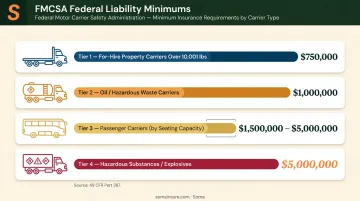

Federal minimums reflect this exposure. Under 49 CFR Part 387, FMCSA requires:

- $750,000 for many for-hire property carriers (vehicles over 10,001 lbs GVWR)

- $1 million for carriers transporting oil, hazardous waste, or hazardous materials

- $5 million for carriers transporting specified hazardous substances or explosives

- $1.5 million–$5 million for passenger carriers depending on seating capacity

The Insurance Information Institute recommends $1 million in business auto coverage, with $500,000 as the floor. Given verdict trends, fleets operating heavy vehicles should treat those federal minimums as a starting point, not a ceiling.

More vehicles on the road mean more exposure events per year — and commercial auto liability coverage scales with that risk. A single uninsured accident involving bodily injury can produce a judgment that exceeds everything else on the balance sheet.

Operational Continuity Through Physical Damage Coverage

Commercial auto insurance includes collision and comprehensive coverage for the fleet's own vehicles. When a van is totaled, a truck is stolen, or equipment is damaged in a hailstorm, physical damage coverage funds repairs or replacement — rather than pulling from operating cash flow.

The downtime cost makes this concrete. Fleet Maintenance reported that vehicle downtime can cost fleets $448 to $760 per day per vehicle. Multiply that across multiple vehicles sidelined by an uninsured incident, and the revenue impact accumulates — missed deliveries, violated SLAs, client penalties.

Physical damage coverage converts that disruption into a claims process, freeing fleet managers to focus on getting vehicles back on the road.

When physical damage coverage matters most:

- High-theft metro areas where vehicle theft rates are elevated

- Extreme weather regions prone to hail, flooding, or severe storms

- Fleets with high-value specialized equipment (refrigerated trucks, aerial lifts, medical transport vehicles)

- Operations where a single vehicle handles a disproportionate share of revenue

Regulatory Compliance and Multi-Jurisdiction Protection

Commercial auto insurance is legally mandated for business-owned vehicles in 49 U.S. states. For fleets crossing state lines, compliance must be maintained in every jurisdiction of operation — and state minimums vary significantly.

California's general vehicle liability minimum is $30,000/$60,000/$15,000, but motor carrier permit requirements range from $300,000 to $5 million depending on vehicle type and cargo. Missouri's minimum is $25,000/$50,000/$25,000. Federal FMCSA requirements layer on top for interstate carriers, starting at $750,000.

Operating without required coverage isn't just a compliance gap — it carries direct financial penalties. FMCSA's penalty schedule lists:

- $18,170 for failing to maintain required financial responsibility

- $11,876 for operating without required registration or authority

A well-structured fleet policy addresses this by meeting the highest applicable minimums across all jurisdictions of operation — eliminating the risk of a coverage gap that creates regulatory exposure before any accident occurs.

Beyond regulatory compliance, many shippers and enterprise clients require proof of commercial auto coverage as a contract condition. Any time a fleet enters a new shipping contract or client relationship, verifying that existing coverage meets the counterparty's requirements should be a standard step — not an afterthought.

What Happens When Commercial Auto Insurance Is Missing or Ignored

Operating without commercial auto coverage doesn't just create one problem — it creates several at once, and they tend to hit hardest when a business is least prepared.

Direct financial exposure:

- Every at-fault accident involving bodily injury or property damage becomes an out-of-pocket obligation — no insurer to absorb medical bills, vehicle repairs, or legal judgments

- A single serious accident can produce liability that exceeds the business's annual revenue

Operational disruption:

- Without physical damage coverage, a totaled or heavily damaged vehicle stays off the road until the business funds repairs

- Lost capacity cuts revenue and forces client commitments to go unmet

Regulatory and contractual fallout:

- FMCSA penalties up to $18,170 for failing to maintain required financial responsibility

- State vehicle registration suspension for lapsed or absent coverage

- Loss of operating authority

- Disqualification from client contracts that require proof of insurance

- Lasting reputational exposure in trust-dependent sectors — healthcare transport, delivery logistics, and construction — where an at-fault accident involving an uninsured vehicle can cost future contracts as much as it costs in court

How to Get the Most Value from Commercial Auto Insurance for Your Fleet

Fleet insurance works best when it's calibrated to actual operations. Providing underwriters with accurate data upfront — vehicle types, driver MVRs, annual mileage, routes, and cargo — produces coverage matched to real exposure rather than generic defaults.

Practices that directly reduce premiums over time:

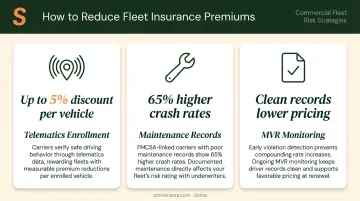

- Enroll in telematics programs: The Hartford offers eligible commercial fleets a premium discount of up to 5% per vehicle with qualifying telematics. Carriers use the data to verify safe driving behaviors rather than relying solely on historical loss runs

- Keep maintenance records current: FMCSA research found that motor carriers targeted for vehicle-maintenance interventions had a 65% greater future crash rate than carriers not targeted — maintenance isn't just a repair issue, it's a risk rating factor

- Run periodic MVR checks: clean driving records across the fleet directly affect pricing, and catching violations early prevents them from compounding into premium increases

Working with a specialized broker simplifies the placement process. Rather than approaching carriers individually — a process that can take weeks — brokers like Soma access hundreds of carrier partners through a single application.

For trucking and commercial fleet risks specifically, Soma places coverage through carriers including Chubb, Progressive, Kemper, and Ascend, covering hard-to-insure operations that standard markets decline: new ventures, drivers with violations, specialty commodities, and hazmat haulers.

For fleet operators who've been quoted high rates or turned away by standard markets, that access to specialized carriers often makes the difference between getting covered and going bare. Soma also handles DOT and FMCSA filings as part of the trucking insurance process, which removes a significant administrative burden from fleet managers operating under federal requirements.

Conclusion

For fleet operators, commercial auto insurance determines whether an accident costs a few weeks of paperwork or costs a business its operating authority. The exposure compounds with fleet size: more vehicles, more routes, more jurisdictions all mean more risk events — and more reasons adequate coverage needs to hold up.

Being underinsured consistently costs more than being properly covered. Consider what each of these scenarios actually costs:

- An uninsured judgment that exceeds bare-minimum liability limits

- A vehicle sidelined because physical damage coverage wasn't in place

- A contract lost because a certificate of insurance had lapsed

Any one of those outcomes typically exceeds what a well-structured fleet policy would have cost for the year.

Review coverage as the fleet evolves. A policy that fit a five-vehicle regional operation may not hold up for a fifteen-vehicle multi-state fleet. When coverage keeps pace with operations, fleet operators avoid the gaps that turn routine incidents into business-threatening claims. That's worth a policy review every time the fleet changes.

Frequently Asked Questions

Why is commercial auto insurance important?

Commercial auto insurance protects businesses from liability claims, vehicle repairs, and medical costs that personal auto policies explicitly exclude for business use. It also satisfies legal requirements in nearly every U.S. state — penalties for non-compliance apply even before an accident occurs.

At what point do I need commercial auto insurance?

Any vehicle used primarily for business purposes requires commercial auto coverage. This includes employee-driven company vehicles, delivery vans, and fleet trucks. If a personal policy is in place when a business-use accident occurs, the claim is typically denied outright.

What is the difference between fleet insurance and commercial insurance?

Commercial auto insurance covers any business-use vehicle, including a single vehicle. Fleet insurance is a specific structure of commercial auto coverage that consolidates two or more vehicles under one policy — simplifying administration and often reducing the per-vehicle premium compared to managing individual policies.

Does commercial auto insurance cover all drivers in my fleet?

Fleet policies generally extend coverage to any employee authorized to drive company vehicles, without requiring each driver to be individually listed. Driver MVR history still affects underwriting, but day-to-day management is significantly simpler.

How much does commercial fleet insurance typically cost?

Costs vary based on fleet size, vehicle type, driver records, cargo, and routes. Industry estimates range from $150 to $900 per vehicle per month depending on risk profile and coverage limits.

What happens if a fleet vehicle is in an accident without commercial auto coverage?

The business becomes directly liable for all costs out of pocket: repairs, medical bills, legal fees, and judgments. Operating without required coverage can also trigger FMCSA penalties up to $18,170, loss of operating authority, and disqualification from client contracts.