What many business owners don't realize is that fleet insurance isn't a completely different product from commercial auto coverage. It's a specialized form of it, designed for multi-vehicle operations. Choosing the wrong structure doesn't just create administrative friction — it can mean coverage gaps, higher per-vehicle costs, and compliance exposure as the fleet grows.

This article breaks down the structural differences between the two, how each is priced, who qualifies for fleet coverage, and how to decide which approach fits your operation.

TL;DR

- A commercial auto policy covers business-owned vehicles, typically structured per vehicle with named driver requirements.

- Fleet insurance is a commercial auto variant that bundles multiple vehicles under one policy, often with "any driver" flexibility.

- Fleet policies generally offer unified renewals, simpler administration, and more flexible driver coverage as your vehicle count grows.

- Standard commercial auto suits businesses with one to two vehicles; fleet coverage becomes advantageous at three or more.

- The right choice comes down to vehicle count, driver rotation frequency, and how complex your operations are.

Fleet Insurance vs. Commercial Auto: Quick Comparison

| Feature | Commercial Auto Policy | Fleet Insurance |

|---|---|---|

| Coverage scope | Individual business vehicles, each listed separately | Two or more vehicles under one consolidated policy |

| Driver structure | Named/listed drivers per vehicle | Often "any driver" — any licensed employee can operate any vehicle |

| Administration | Separate policies, renewals, and documents per vehicle | One policy, one renewal, one point of contact |

| Cost structure | Each vehicle priced on its own risk profile | Fleet priced on aggregate risk; often lower per-vehicle cost at scale |

| Scalability | Adding a vehicle may require a new policy or endorsement | Mid-term vehicle additions are typically simpler adjustments |

What Is a Commercial Auto Policy?

A commercial auto policy is the foundational coverage for any vehicle owned by — or used primarily for — a business. According to the Insurance Information Institute, the Business Auto Coverage Form is the standard form many insurers use, and it covers cars, trucks, trailers, and vans used on public roads.

Standard coverage components typically include:

- Bodily injury and property damage liability

- Collision and comprehensive physical damage

- Uninsured/underinsured motorist coverage

- Medical payments or personal injury protection

- Hired and non-owned auto (HNOA) — covers employees using personal or rented vehicles for business purposes, but not physical damage to those vehicles

Who Needs a Standard Commercial Auto Policy?

Commercial auto works best when vehicle use is predictable and driver assignments are consistent. Think: one service van driven by the owner, a company car assigned to a sales rep, or a pickup truck used by a solo contractor.

Industries where individual commercial auto policies are common include:

- Real estate agencies and independent consultants

- Solo contractors and small trade businesses

- Small retailers with one delivery vehicle

- Food service operations with a single company vehicle

What does it cost? According to The Hartford, average commercial auto premiums run around $574/month ($6,884/year), though rates vary widely by business type, vehicle, and use. Progressive's 2024 data puts monthly averages at $272 for contractor autos and $954 for for-hire transport trucks — a range that shows how much industry and vehicle type shape the final number.

What Is Fleet Insurance?

Fleet insurance is a commercial auto policy structured to cover multiple business vehicles under a single consolidated policy. Rather than pricing each vehicle individually, insurers assess the aggregate risk of the entire fleet — factoring in total vehicle count, vehicle types, driver history across all employees, average mileage, and fleet safety programs.

The qualification threshold varies by carrier and source. The 2024 Commercial Automobile Insurance Manual defines fleet as five or more self-propelled automobiles under one ownership (trailers excluded from the count). Progressive sets its threshold at 10 or more vehicles.

The threshold is ultimately carrier-specific — some will write fleet policies starting at two or three vehicles, others not until five or ten.

The "Any Driver" Provision

One of the most operationally significant differences between fleet and individual commercial auto is driver structure. Many fleet policies can be written with an "any driver" provision, meaning any licensed employee can operate any vehicle in the fleet without being individually listed.

For businesses with rotating staff, seasonal workers, or high driver turnover, this isn't a minor convenience — it's essential. A named-driver commercial auto policy creates real exposure if an unlisted employee drives a vehicle and is involved in an incident.

Vehicle Types and Add-Ons

Most fleet policies can cover mixed vehicle types. Travelers, for example, writes fleet coverage spanning passenger vehicles all the way to tractor-trailers. Progressive covers cars, vans, pickup trucks, SUVs, semis, and dump trucks. Nationwide covers cars, cargo vans, box trucks, and utility trucks but excludes semi-trucks — carrier appetite varies.

Common fleet policy add-ons include:

- Cargo coverage for businesses transporting goods

- HNOA coverage for employees using personal or rented vehicles

- Roadside assistance

- Telematics programs — Progressive's Smart Haul program, for instance, reports average savings of $1,056 for new for-hire truck customers who participate; Nationwide's Vantage 360 Fleet offers a 10% discount on select coverages for enrolled policyholders

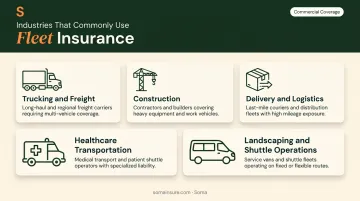

Industries Where Fleet Coverage Is the Norm

Fleet insurance is built for businesses where vehicles are core operational assets, not just supporting tools:

- Trucking and freight operations with rotating drivers and DOT/FMCSA compliance requirements

- Construction firms adding vehicles mid-term after new contracts, with shifting driver assignments

- Delivery and logistics companies running high vehicle counts on daily routes

- Healthcare transportation providers needing specialized coverage for ambulances and patient transport

- Landscaping and hospitality shuttle operations with mixed fleets and high-frequency daily use

Each of these industries carries distinct coverage requirements. Soma places fleet and commercial auto coverage across all of them — including trucking through carriers like Chubb, Progressive, Kemper, and Ascend — and handles DOT and FMCSA filings for regulated operations where required.

Key Differences Between Fleet Insurance and Commercial Auto Policies

Driver Assignment and Coverage Gaps

The named driver vs. any driver distinction has direct operational consequences. On a standard commercial auto policy, if an employee not listed on the policy drives a vehicle and causes an accident, coverage could be disputed or denied entirely.

Fleet policies with an "any driver" structure eliminate that gap — any licensed employee is covered, subject to the carrier's eligibility criteria. For businesses managing seasonal staff or growing headcounts, that flexibility is worth examining carefully.

How Claims Affect Your Rate

Under an individual commercial auto policy, one at-fault accident raises the rate for that specific vehicle — sometimes sharply. Under a fleet policy, a single claim is absorbed into the fleet's aggregate loss history. Whether that moderates the rate impact depends on your overall fleet's claims record, but the pooling effect reduces volatility for businesses with clean histories.

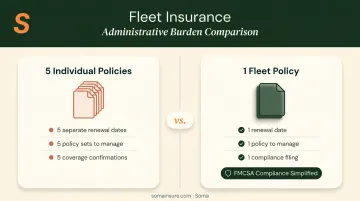

Administrative Efficiency at Scale

Managing five individual commercial auto policies means five renewal dates, five sets of documents, and five separate coverage confirmations when a client requests a certificate of insurance.

Fleet insurance consolidates that into one policy, one renewal, and one place to add or remove vehicles mid-term. For regulated businesses, FMCSA requires entities with operating authority to maintain proof of insurance on file — a single fleet policy makes that compliance straightforward compared to tracking documentation across multiple individual policies.

Cost Structure at Scale

Individual commercial auto policies price each vehicle on its own risk profile. As you add vehicles, each one is independently underwritten and rated. Fleet policies price on aggregate fleet risk, and the per-vehicle cost often improves as the fleet grows due to volume considerations and risk pooling.

No publicly available data source provides verified per-vehicle cost comparisons at specific fleet sizes. Actual savings depend on several factors:

- Fleet composition — vehicle types, ages, and use cases

- Driver history — MVR records across your workforce

- Claims record — your aggregate loss history over prior policy terms

- Carrier's risk appetite — willingness to write your industry and fleet size

The only reliable way to compare is to get quotes for both structures side by side.

Which Coverage Is Right for Your Business?

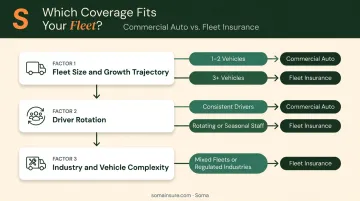

Three factors drive this decision more than any others.

Factor 1: Fleet Size and Growth Trajectory

- 1–2 vehicles, no near-term growth: Individual commercial auto policies are sufficient and simpler to manage.

- 3+ vehicles, or actively adding: Fleet coverage becomes operationally and potentially financially advantageous. The administrative case alone is strong once you're managing multiple renewal dates and policy documents.

Factor 2: Driver Rotation vs. Consistency

- Same driver, same vehicle: Named-driver commercial auto works fine.

- Rotating drivers, seasonal staff, or high turnover: The any-driver provision in a fleet policy is essential. Managing named drivers across multiple policies in a growing operation is error-prone and creates gaps in coverage.

Factor 3: Industry and Vehicle Complexity

Trucking, construction, delivery, and healthcare transportation operations typically run mixed fleets — different vehicle classes with frequent mid-term changes. Adding a truck after winning a new contract shouldn't require restructuring your entire insurance program. Fleet policies handle this with a simple mid-term endorsement.

Getting the Right Structure

Once you know which structure fits, the next challenge is finding the right carrier for it. Fleet thresholds and coverage terms vary significantly — what qualifies as a fleet at one insurer may not at another. Comparing both structures on a true apples-to-apples basis requires access to multiple carriers and an understanding of how each one prices your specific operation.

Soma works with a broad network of carrier partners, including options for operations that standard markets surcharge or decline. That access matters when you're trying to avoid overpaying for the wrong structure — or finding out you have the wrong one after a loss.

Conclusion

The fleet insurance vs. commercial auto decision comes down to scale and how central vehicles are to your operations. Commercial auto policies work well for smaller, stable vehicle counts. Fleet insurance makes more sense once you're managing five or more vehicles, rotating drivers, or tracking vehicles across multiple states.

The structure that worked at two vehicles often breaks down at eight. When your fleet grows — whether that means adding trucks, reassigning drivers, or crossing state lines — revisiting your coverage type is a necessary part of that transition, not an afterthought. A broker who knows commercial auto can identify the right structure quickly and keep gaps from opening during the shift.

Frequently Asked Questions

What is the difference between fleet insurance and individual commercial auto policies?

Individual commercial auto policies cover one vehicle at a time with named drivers assigned per vehicle. Fleet insurance bundles multiple vehicles under one policy, often with any-driver coverage, and prices risk across the entire fleet rather than per vehicle.

What is considered a fleet in commercial auto insurance?

The threshold varies by carrier. The 2024 Commercial Automobile Insurance Manual defines fleet as five or more self-propelled automobiles under one ownership; Progressive's fleet insurance page sets its threshold at 10 or more vehicles.

Is fleet insurance cheaper than insuring vehicles individually?

Fleet insurance typically offers lower per-vehicle costs at scale due to volume pricing and aggregate risk assessment, but no published data provides guaranteed savings at specific fleet sizes. Actual cost depends on your fleet composition, driver records, vehicle types, and the carrier's underwriting appetite. Get quotes for both structures and compare them directly before committing.

Can a fleet policy cover different types of vehicles?

Most fleet policies can cover mixed fleets — cars, vans, trucks, and specialty vehicles — under one policy. Carrier eligibility varies: Travelers covers fleets from passenger vehicles to tractor-trailers; Nationwide covers cargo vans and box trucks but excludes semi-trucks. Verify your specific vehicle mix is eligible before you bind coverage.

Does fleet insurance cover any driver, or only named drivers?

Many fleet policies can be structured with "any driver" coverage, meaning any licensed employee can operate any vehicle in the fleet. Standard commercial auto policies typically require named drivers to be listed per vehicle. Driver eligibility criteria (such as minimum age and MVR review requirements) still apply under any-driver provisions.

When should a business switch from individual commercial auto to fleet insurance?

Evaluate fleet coverage when you reach three or more vehicles, when driver rotation becomes common, or when managing separate policy renewals and documentation starts creating administrative burden or compliance risk. Businesses in regulated industries — such as trucking or healthcare transportation — should assess fleet structure even earlier given the compliance documentation requirements.