The problem? Standard general liability insurance doesn't cover what actually goes wrong in these businesses. A mechanic takes a customer's car out for a road test and gets rear-ended. A hailstorm hits your lot. A customer's vehicle is stolen from your service bay overnight. General liability won't respond to any of those scenarios.

This article covers what garage insurance actually includes, which carriers write the best policies in North Carolina, and what separates adequate coverage from a policy that holds up when you need it.

TL;DR

- Garage insurance bundles premises liability, auto operations liability, and customer vehicle coverage — general liability alone leaves major gaps

- NC motor vehicle dealers must provide garage liability insurer and policy details at license renewal — it's a state requirement

- Top providers for NC garage businesses include Travelers, Auto-Owners, Utica National, Nationwide, and The Hartford — each suited to different operation types

- Pricing turns on operation type, claims history, inventory value, payroll, and limits — work with carriers that actively write garage risks

- A multi-carrier broker delivers competitive options across the right carriers from a single application

What Is Garage Insurance and Who Needs It in North Carolina?

The Core Definition

Garage insurance is a commercial policy built around the ISO CA 00 05 Garage Coverage Form — a standard form that extends liability beyond what general liability covers. It combines three exposures in one policy structure:

- Premises liability — bodily injury or property damage occurring on your business property

- Auto operations liability — accidents involving vehicles your business controls, including customer cars during road tests

- Garagekeepers coverage (via ISO CA 99 37 endorsement) — physical damage to a customer's vehicle while it's in your care, custody, and control

That last piece is what general liability policies routinely miss. If a customer's car is stolen from your lot, flooded during a storm, or damaged by an employee, garagekeepers coverage responds. General liability does not.

Who Needs It in NC

Any NC business that takes possession of customer vehicles should carry garage insurance. That includes:

- Auto repair shops and service stations

- Franchise and independent car dealerships

- Body shops and paint shops

- Tow truck operators

- Auto detailers

- Emissions testing centers

- Parking facilities

The licensing requirement is most explicit for dealers. NCDMV's 2025 Dealer Renewal Packet requires applicants to provide the garage liability insurance company underwriter's name and policy number — the agent's name alone is not accepted.

No universal NC mandate covers every repair shop by name, but franchise agreements and county-level licensing frequently impose equivalent requirements.

North Carolina's Specific Risk Profile

NC businesses face three exposures that make adequate coverage non-negotiable:

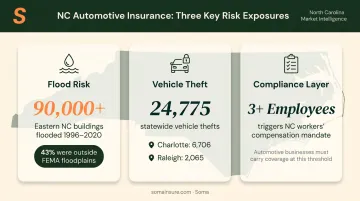

- Flood risk beyond the coast: NC DEQ's 2026 advisory floodplain data shows 90,000+ Eastern NC buildings flooded between 1996 and 2020 — 43% were outside mapped FEMA floodplains, meaning standard flood assumptions don't hold.

- High urban vehicle theft: NC SBI's 2024 crime report recorded 24,775 statewide motor vehicle thefts — Charlotte-Mecklenburg alone accounted for 6,706, with Raleigh adding 2,065.

- Stacked compliance requirements: Shops with three or more employees must also carry workers' compensation under NC Industrial Commission rules — a separate mandate that layers on top of garage insurance.

Top Garage Insurance Providers in North Carolina

The following carriers were selected based on coverage breadth, NC market presence, claims service reputation, and fit for different garage business types.

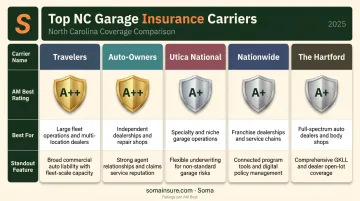

Travelers

Travelers ranks No. 2 nationally in commercial auto by direct premiums written, according to NAIC market share data — that scale translates to deep familiarity with automotive risks. Their dedicated Industry Edge for Auto & Truck Dealers package goes well beyond basic garage liability.

| Coverage Area | Details |

|---|---|

| Key Coverages | Garage liability, garagekeepers, commercial auto, auto E&O, cyber liability, EPLI, umbrella/excess |

| Best For | Franchise dealerships, multi-location businesses, operations needing broad customization |

| Notable Feature | Bundled cyber liability and excess coverage in a single dealer package — relevant for dealerships handling customer financial data under FTC Safeguards Rule requirements |

AM Best Rating: A++

Auto-Owners Insurance

Auto-Owners is a regional carrier with strong Southeast presence, an A++ AM Best rating, and consistent claims handling through dedicated agent relationships. Their garage product is specifically built for dealerships and repair shops across multiple vehicle types — motorcycles, boats, RVs, and farm equipment included.

| Coverage Area | Details |

|---|---|

| Key Coverages | Garage liability, garagekeepers, dealer's blanket (inventory), inland marine, mechanics E&O |

| Best For | Independent repair shops, small-to-mid-size dealerships, businesses with significant tool and equipment value |

| Notable Feature | Dealer's Blanket Reporting Form discount — report inventory monthly and earn premium reductions based on actual exposure |

AM Best Rating: A++

Utica National

Utica National has focused on auto dealerships for decades, covering every dealer type: franchised new car and truck sales, non-franchised used car lots, and franchised motorcycle dealers including Harley-Davidson and BMW. Their standout feature is how they structure liability protection — combining general liability and garage liability into a single blanket policy rather than two separate ones.

| Coverage Area | Details |

|---|---|

| Key Coverages | Blanket general + garage liability, garagekeepers, dealers' physical damage, dealer E&O (title, odometer, prior damage), customer rental coverage |

| Best For | All dealer types, motorcycle and powersports dealers, businesses wanting maximum liability protection in a single policy |

| Notable Feature | Combines GL and garage liability into one high-limit blanket policy — eliminates the gap between two separate policies |

AM Best Rating: A (Excellent)

Nationwide

Nationwide actively writes auto service and repair businesses, holds an A AM Best rating, and offers 24/7 claims service. Their business owners policy for repair shops bundles core coverages with endorsements that address operational risks standard policies skip.

| Coverage Area | Details |

|---|---|

| Key Coverages | Garage liability (bundled with GL by class code), garagekeepers, commercial property, workers' comp, employee tool coverage |

| Best For | Service stations, fuel and repair combo operations, businesses needing loss control resources |

| Notable Feature | Lost key and tumbler coverage plus transit pollutant clean-up endorsements — particularly useful for full-service garages handling fuel systems |

Nationwide is also one of Soma's active carrier partners, which means NC automotive businesses quoting through Soma can access this market directly.

The Hartford

The Hartford serves over 1.3 million small business customers and holds an A+ AM Best rating, with in-house claims adjusters handling commercial auto and property claims — not outsourced adjusters following a script.

| Coverage Area | Details |

|---|---|

| Key Coverages | Garage liability, garagekeepers, inland marine (tools), workers' comp, commercial property |

| Best For | Mechanics and repair shops with significant tool inventory and multi-employee operations |

| Notable Feature | In-house claims adjusters with 24/7 access — faster resolution for shops with continuous vehicle throughput |

What Does a Complete Garage Insurance Policy Cover in North Carolina?

The Core Coverage Stack

A complete NC garage policy combines four layers:

- Garage liability — covers third-party bodily injury and property damage arising from your operations, including accidents involving customer vehicles your employees are driving

- Garagekeepers coverage — covers physical damage to customer vehicles in your care from fire, theft, vandalism, collision, or weather; available as direct primary (pays regardless of fault) or direct excess (pays over the customer's own insurance)

- Commercial auto — covers business-owned vehicles, including service trucks, loaners, and shuttle vehicles

- Commercial property — covers your building, equipment, and inventory against fire, storm, theft, and other covered perils

What Garage Insurance Does Not Cover

These exclusions catch NC shop owners off guard:

- Employee injuries — requires separate workers' comp (mandatory for NC businesses with 3+ employees)

- Pollution and chemical damage — fuel, oil, and solvent contamination typically excluded unless a specific endorsement is added

- Cost of redoing faulty work — the defective repair itself is not covered; only resulting damage to third parties may be

- Business-owned vehicles damaged on the lot — covered under commercial auto or dealers' physical damage, not garage liability

Optional Endorsements Worth Considering

Some of the exclusions above can be addressed with targeted add-ons. For NC operations, these endorsements cover real gaps:

- Auto Errors & Omissions — protects against claims of faulty diagnostics, missed defects, or improper repair work

- Employment Practices Liability (EPLI) — important for shops with multiple employees

- Cyber Liability — required for dealerships handling customer financing data under the FTC Safeguards Rule (breach notification required within 30 days for incidents affecting 500+ consumers)

- Umbrella/Excess Liability — extends limits above the base policy for high-exposure operations

How to Choose the Right Garage Insurance Policy in NC

What Actually Matters in Carrier Selection

When comparing policies, evaluate these factors:

- NC market appetite: Some carriers write garage risks selectively — confirm the carrier actively writes your business type in your county before binding

- Coverage breadth: Garagekeepers coverage is sometimes an add-on, not a default; ask specifically whether it's included

- Financial strength: AM Best ratings of A or better indicate the carrier can pay large claims without delay

- Claims handling: In-house adjusters (The Hartford is a good example) typically resolve claims faster than outsourced teams

- Fit for your operation: A sole-mechanic shop and a 10-rooftop dealership group have fundamentally different risk profiles — your policy should reflect that

Common Mistakes NC Garage Owners Make

Knowing what to look for is only half the equation. These are the mistakes that cost NC garage owners the most:

- Buying standard general liability and assuming it covers customer vehicles — it doesn't

- Skipping garagekeepers because it seems optional — if a customer's car is damaged in your bay, you'll wish you had it

- Not reviewing policy limits against actual inventory value — a $500,000 vehicle inventory insured under a $250,000 limit leaves real exposure

- Ignoring E&O coverage for repair and diagnostic services — one disputed repair claim can exceed your base liability limits

Conclusion

The best garage insurance policy for your NC automotive business isn't about picking the largest carrier — it's about matching the coverage structure to your actual operation. A franchise dealership handling customer financing needs blanket liability and cyber coverage. An independent repair shop with $80,000 in tools needs solid garagekeepers and inland marine. A service station needs endorsements that standard repair shop policies don't include.

Finding the right carrier is where most business owners get stuck. Garage insurance is a specialty commercial line, which means quoting it efficiently requires going to carriers that actually want to write it — not standard markets that decline the risk or underprice it. Soma works with Nationwide, Chubb, Markel, Liberty Mutual, and a network of hundreds of carrier partners, placing garage risks across North Carolina — including harder-to-insure operations that standard markets pass on.

If you're an NC automotive business owner ready to get the right coverage structure, get a customized garage insurance quote through Soma. One application reaches multiple carriers, with fast turnaround and no weeks spent chasing brokers.

Frequently Asked Questions

How much is garage liability insurance per month?

Garage liability alone typically runs $100–$200 per month, though NC-specific benchmarks vary by carrier. Your actual cost depends on operation type, claims history, payroll, inventory value, and coverage limits. A full stack including garagekeepers, commercial auto, and workers' comp will run significantly higher, so get carrier quotes for an accurate number.

What is the difference between garage liability and garagekeepers insurance?

Garage liability covers third-party bodily injury and property damage caused by your business operations — including road test accidents and on-premises incidents. Garagekeepers covers physical damage to a customer's vehicle while it's in your shop's care, custody, and control. Most NC automotive businesses need both; they address completely different exposures.

Do auto repair shops in North Carolina need garage insurance?

NC doesn't mandate garage insurance universally, but dealers must provide garage liability documentation during NCDMV license renewal. Franchise agreements, county licensing, and basic liability exposure make it a practical necessity regardless — general liability policies don't cover customer vehicle damage.

What does garage insurance not cover?

Common exclusions include:

- Employee injuries (covered by workers' comp)

- Pollution or chemical damage

- The cost of redoing faulty work itself

- Damage to your own business vehicles (covered under commercial auto or dealers' physical damage)

E&O endorsements can address some workmanship-related claims, but the base garage policy won't.

How many quotes should I get for garage insurance in North Carolina?

Get at least three quotes — but only from carriers with genuine appetite for garage risks in NC. A multi-carrier broker like Soma lets you compare options across the right markets with a single application, rather than completing separate submissions for each carrier individually.