Dram shop lawsuits can run into seven figures. A single incident — an over-served guest who causes a car accident after leaving your dining room — can trigger legal defense costs, settlements, and judgments that no amount of good intentions will offset.

This article breaks down exactly what each policy covers, where they differ, and why restaurants that serve alcohol need both working together.

TL;DR

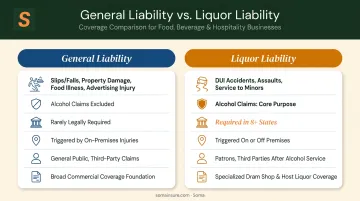

- General liability covers everyday operational risks (slips, falls, food-related illness, property damage) — but explicitly excludes alcohol-related claims.

- Liquor liability fills that gap, covering claims from over-service: drunk driving accidents, patron-on-patron assaults, service to minors.

- Dram shop laws exist in 43 states and DC — your restaurant can be sued for what an intoxicated guest does after leaving.

- Most liquor liability policies require active GL coverage first — any restaurant serving alcohol needs both, not one or the other.

General Liability vs. Liquor Liability: At a Glance

Here's how the two policies compare side by side:

| Dimension | General Liability | Liquor Liability |

|---|---|---|

| What it covers | Slips/falls, property damage, food illness, advertising injury | Claims from alcohol service: DUI accidents, assaults, service to minors |

| Alcohol-related claims | Explicitly excluded | Core purpose |

| Legally required? | Rarely by law; often required by leases/lenders | Required in at least 8 states; often tied to liquor license |

| Typical claim trigger | Customer injury on premises, food allergy, vendor property damage | Intoxicated patron causes harm on or off premises |

| Relationship | Foundation policy | Required add-on layer |

Restaurant owners should know that the ISO Commercial General Liability form (CG 00 01) contains an explicit liquor liability exclusion. It's a deliberate design — any business in the alcohol service trade is carved out, regardless of how infrequently they serve drinks.

These two policies address entirely separate liability theories, which is why carrying only one leaves a real gap in coverage.

What Does General Liability Insurance Cover for a Restaurant?

General liability is the foundational policy every restaurant needs. It covers third-party claims from normal daily operations — bodily injury, property damage, product liability — regardless of whether alcohol is involved.

What GL Actually Covers

The four core coverage categories most relevant to restaurants:

- Bodily injury — a customer slips on a wet floor near the host stand and breaks a wrist

- Property damage — a kitchen fire spreads and damages the neighboring business

- Product liability — a patron has an allergic reaction to an undisclosed ingredient

- Personal/advertising injury — a competitor claims your promotional material is defamatory

AmTrust data shows more than 1 million guests are injured in foodservice slip-and-fall accidents annually, costing the industry roughly $2 billion per year. Food-related illness claims carry similar weight — one peer-reviewed study estimated a single outbreak can cost a fast-casual restaurant between $6,330 and $2.1 million depending on scale.

The Alcohol Exclusion — No Gray Area

The ISO CGL form excludes bodily injury or property damage when the claim stems from causing intoxication, serving an already-intoxicated guest, or serving a minor — provided the insured is in the business of selling or serving alcohol.

A concrete example: an intoxicated patron trips and injures another guest on your premises. Even though the injury happened inside your restaurant, GL denies the claim because intoxication is the root cause. That exposure falls to liquor liability, which is a separate policy restaurants that serve alcohol need to carry.

GL and the BOP Option

Understanding what GL excludes is one side of the equation — how you buy it is the other. For most small to mid-sized restaurants, GL is bundled into a Business Owner's Policy (BOP), which pairs GL with commercial property coverage at a lower premium than purchasing both separately. A standalone GL policy makes more sense for larger restaurants with complex property situations or those needing customized limits.

Premium factors that directly affect your GL cost:

- Location and local litigation environment

- Square footage and seating capacity

- Annual revenue

- Prior claims history

What Does Liquor Liability Insurance Cover for Restaurants?

Liquor liability — sometimes called dram shop insurance — covers claims that arise specifically from your restaurant's alcohol service. The key distinction from GL: this coverage protects you from what happens because of how you served alcohol, including incidents that occur after the patron has left your premises.

Dram Shop Laws and Why They Matter

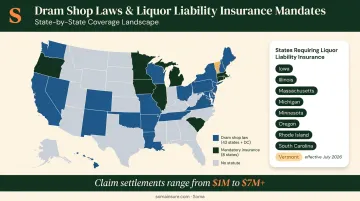

Dram shop statutes allow injured third parties to sue the establishment that served the alcohol. The scope varies by state, but according to FindLaw, 43 states and DC have some form of dram shop law. Even in states without a statute, civil lawsuits under common law negligence remain possible.

At least 8 states currently mandate liquor liability insurance as a condition of holding an on-premises alcohol license:

- Iowa, Illinois, Massachusetts, Michigan

- Minnesota, Oregon, Rhode Island, and South Carolina

- Vermont joins this list effective July 1, 2026

The financial exposure from these claims is severe. Court records and plaintiff firm summaries document settlements and judgments ranging from $1 million to over $7 million in restaurant-specific dram shop cases.

What Liquor Liability Covers (and What It Doesn't)

Covered scenarios:

- An intoxicated diner leaves your restaurant, causes a DUI accident, and the injured driver sues you

- A visibly drunk patron is served another drink, then assaults another guest

- A minor presents a fake ID, is served, and is later involved in an incident

What's typically not covered:

- The intoxicated patron themselves (they're the insured cause, not the victim)

- Claims arising from your own employees' intoxication while on duty

Server Training Is an Insurance Issue, Not Just a Legal One

If your servers lack documented training certifications and a claim is filed, some carriers will reduce or contest coverage outright. Insurers specifically look for state-recognized certifications like TIPS or ServSafe Alcohol as evidence of responsible service practices.

Key pricing variables for liquor liability:

- Alcohol-to-food revenue ratio (Chubb specifically uses 30% liquor receipts as an underwriting threshold)

- Hours of operation (late-night service increases exposure)

- Seating capacity

- Prior claims history

- State-required minimum limits

Those variables feed directly into a market that has tightened sharply. CRC Group reported in 2026 that even clean hospitality accounts are seeing liquor liability premiums of $25,000 to $50,000, driven by rising claim severity across bars, restaurants, and venues.

Key Differences Between General Liability and Liquor Liability for Restaurants

The Four Differences That Matter Operationally

1. Scope of covered claims: GL covers operational risks — premises injuries, food-related illness, vendor property damage, advertising disputes. Liquor liability covers alcohol-service risks: over-service, service to minors, off-premises DUI incidents. These are separate liability theories; one policy cannot substitute for the other.

2. Legal requirements: GL is rarely mandated by state law. Liquor liability is required by statute in at least 8 states and is frequently a condition of a liquor license or local permit. Failing to carry liquor liability in a mandate state risks license revocation, not just financial exposure.

3. Who the coverage protects: Both protect the restaurant against third-party claims, but from different sources. GL responds to anyone harmed by general business operations. Liquor liability responds specifically to third parties harmed by an intoxicated patron your restaurant served.

4. Claim severity profile: Alcohol-related lawsuits — particularly those involving DUI fatalities or serious injuries — tend to produce catastrophic damages. GL claims from slip-and-falls are frequent but generally lower in severity. Liquor liability claims are less frequent but far more likely to reach six or seven figures, which is why limits selection matters significantly.

Which Policy Should You Choose?

Understanding these differences makes the answer straightforward: it's not a choice between the two. GL is the required foundation — most liquor liability policies mandate that active GL coverage be in place first. Liquor liability fills a coverage gap that GL explicitly excludes. A restaurant carrying only GL while serving alcohol has zero coverage for every alcohol-related claim.

Quick situational guide:

| Restaurant type | GL needed? | Liquor liability needed? |

|---|---|---|

| Full-service restaurant with bar | ✅ Yes | ✅ Yes |

| Dry restaurant (no alcohol) | ✅ Yes | ❌ No |

| Occasional private events with BYOB | ✅ Yes | Evaluate host liquor coverage or event-based policy |

Soma works with carrier partners including Markel, Nationwide, and Liberty Mutual to place both coverages for restaurants — including late-night venues, high-occupancy establishments, and locations with prior claims history that standard markets decline. Both policies can often be placed through a single intake process, so you're not managing separate applications with separate brokers.

Conclusion

The decision framework is straightforward: if your restaurant serves, pours, or sells alcohol in any form — even occasionally — you need both policies in place. GL protects against the operational risks every restaurant faces. Liquor liability protects against the specific and serious legal exposure that comes the moment you hand someone a drink.

One uninsured liquor liability claim can easily exceed years of combined premium payments — dram shop verdicts in states like Texas and Florida routinely reach six figures, and legal defense costs alone can drain an uninsured restaurant before a verdict is even reached.

Before your next service, confirm:

- Your GL policy has been reviewed for the standard liquor liability exclusion

- A standalone liquor liability policy is in force (not assumed to be bundled)

- Your coverage limits meet your state's dram shop requirements

- Your policy reflects your actual alcohol sales volume

Review your current coverage now. If you're unsure whether your GL contains the standard liquor liability exclusion — it almost certainly does — or whether your liquor liability limits are adequate for your state's requirements, reach out to Soma for a coverage review. The turnaround is quick, and getting it wrong is far costlier than getting it right.

Frequently Asked Questions

Frequently Asked Questions

Is general liability the same as liquor liability?

No. They are two distinct policies covering different types of legal exposure. GL covers general operational claims like slips, falls, and property damage. Liquor liability covers claims arising from alcohol service, which GL explicitly excludes for businesses in the alcohol trade.

What does general liability cover for a restaurant?

GL covers:

- Third-party bodily injury (slip-and-fall)

- Property damage

- Product liability (food-related illness)

- Personal and advertising injury

It does not cover any claim where the sale, service, or furnishing of alcohol is a cause or contributing factor.

How much is general liability and liquor liability insurance?

Costs vary significantly based on revenue, location, seating capacity, and claims history. For liquor liability, the market has hardened — even clean accounts are seeing premiums of $25,000 to $50,000 according to 2026 wholesale broker data. Get a quote specific to your operation rather than relying on industry averages.

Do restaurants need both general liability and liquor liability insurance?

Yes, if alcohol is served. GL is the operational foundation and most liquor liability policies require it to be active. Liquor liability then covers the alcohol-specific claims that GL excludes. Carrying only one while serving alcohol leaves a direct and serious coverage gap.

What happens if a restaurant doesn't have liquor liability insurance?

The restaurant funds its own defense, settlements, and judgments for any alcohol-related claim — with no insurer responding. In dram shop states, those costs can reach six or seven figures. In states where liquor liability is required by law, operating without it also risks losing your liquor license.

Does liquor liability insurance cover restaurant employees?

Liquor liability primarily protects the restaurant from third-party claims brought by those harmed by an intoxicated patron. Whether employees qualify as additional insureds depends on the specific policy terms, so confirm coverage scope with your broker before making assumptions.