When an establishment serves alcohol to a visibly intoxicated patron who then injures someone, South Carolina law allows the victim to sue — not just the drunk driver, but the business that kept pouring. Civil judgments, permit revocations, and insurance gaps can all follow.

That exposure changed significantly on January 1, 2026, when H.3430 (Act No. 42) took effect. The law rewrote liability caps, added a uniform "knowingly" standard across all alcohol types, and made server training mandatory statewide.

This guide covers what SC dram shop law requires, who faces liability, what H.3430 actually changed, and what businesses need to do to stay protected.

TL;DR

- SC dram shop liability comes from multiple statutes (§61-4-580 and §61-6-2220), not a single codified act

- Bars, restaurants, venues, and even social hosts can face liability for knowingly serving intoxicated or underage patrons

- As of January 1, 2026, establishment liability is capped at 50% of actual damages, and server training is now mandatory

- On-premises licensees open past 5 p.m. must carry at least $1 million in liquor liability insurance (credits can reduce that floor, but never below $300,000)

- Documentation of training, ID checks, and service refusals can be decisive in litigation

What Is South Carolina's Dram Shop Liability Law?

South Carolina does not have a single codified "Dram Shop Act." Instead, as the SC Supreme Court noted in Hartfield v. The Getaway Lounge & Grill, Inc. (2010), civil liability "arises out of criminal statutes" — primarily two:

- §61-4-580 (beer and wine): Prohibits permit holders and their employees from knowingly selling to anyone under 21 or to an intoxicated person

- §61-6-2220 (liquor): Prohibits licensees from knowingly selling liquor to persons in an intoxicated condition (amended by H.3430 to add "knowingly," covered in detail below)

Violating either statute can expose an establishment to civil liability, permit suspension, or revocation. Courts have recognized a private right of action for third parties harmed by overservice, meaning victims injured by intoxicated patrons can sue the business that served them.

The Insurance Requirement That's Been in Place Since 2017

Since July 1, 2017, Section 61-2-145 has required any business licensed to sell alcohol for on-premises consumption — and operating past 5:00 p.m. — to carry at least $1 million in liquor liability coverage. H.3430 updates how that requirement works (adding credits, a floor, and new policy-type distinctions), but the baseline obligation has been in place for nearly a decade.

Who Can Be Held Liable Under SC Dram Shop Law?

The statutes reach permit and license holders, their servants, agents, and employees. In practice, that covers a wide range of businesses:

- Bars and bar-restaurants (Hartfield; Christiansen v. Campbell)

- Hotel bars and sports clubs (Tobias v. Sports Club, Inc.)

- Event venues and concert halls

- Grocery stores selling beer to minors (Whitlaw v. Kroger Co.)

- Social hosts serving alcohol illegally to minors or visibly intoxicated persons

What a Plaintiff Must Prove

To succeed on a dram shop claim in SC, a plaintiff generally must establish:

- The defendant knowingly sold, furnished, or served alcohol to a person who was already intoxicated or underage

- That sale or service was the proximate cause of the plaintiff's injury

The "knowingly" standard doesn't require a server to have explicitly acknowledged a patron's intoxication. Under Hartfield, it includes what a reasonably prudent person would have observed — visible signs like appearance or behavior that signal intoxication to any reasonable observer.

Can an Intoxicated Person Sue the Alcohol Vendor?

SC law does permit intoxicated persons to bring their own claims. Christiansen v. Campbell (1985) established this, and Tobias confirmed that SC law "clearly extended the cause of action to the intoxicated person himself."

That said, permit holders can raise defenses including contributory negligence and assumption of risk. No categorical bar prevents intoxicated adults from recovering against a vendor under current SC case law — the outcome turns on the specific facts and which defenses apply.

Key Changes Under H.3430: What SC Dram Shop Law Looks Like in 2026

H.3430 was ratified May 8, 2025, signed May 12, 2025, and took effect January 1, 2026 for most provisions. Here's what changed:

Joint and Several Liability — Now Capped at 50%

Under the old rule (§15-38-15(F)), an establishment found even 1% liable for a plaintiff's injuries could be held responsible for 100% of damages. H.3430 removes that exception.

Under the new Section 61-2-147, when both a drunk driver and the establishment are found liable, the establishment's share of joint and several liability is capped at 50% of the plaintiff's actual damages. The drunk driver and other tortfeasors are included on the verdict form, and liability is allocated accordingly.

The "Knowingly" Standard Now Applies to All Alcohol Types

Previously, §61-4-580 (beer/wine) used "knowingly" but §61-6-2220 (liquor) did not — leaving open an argument for something closer to strict liability in liquor overservice cases. H.3430 adds "knowingly" to the liquor statute, aligning all three alcohol types under a consistent standard.

That means courts now apply the same liability test regardless of whether beer, wine, or liquor was served — a meaningful shift for establishments that primarily serve spirits.

Mandatory Server Training — Now Required Statewide

Effective 2026, servers and managers at on-premises licensed establishments must complete a state-approved alcohol server training program. Key details:

- Minimum 4 hours, online, with a proctored test

- Covers SC alcohol laws, ID verification, recognizing intoxication, refusal of service, and DUI liability

- Certificates valid for 3 years, must be kept on-site (physical or electronic)

- Compliance deadline: May 1, 2026 for existing employees; within 30 days of employment for new hires (note: the 60-day window applies specifically to the insurance credit, not the general mandatory deadline)

- SCDOR-approved programs include ServSafe Alcohol, 360training.com, LIQUORexam.com, and others listed at dor.sc.gov

Captive Insurer Eroding Policy Restriction

Under the old system, some captive insurers issued "eroding" policies where defense costs reduced the total coverage available to compensate victims. H.3430 bars captive insurance companies from issuing eroding or declining liquor liability coverage. Traditional admitted and surplus lines insurers are not expressly restricted by this provision. Businesses should review their own policy terms to confirm how defense costs are structured relative to coverage limits.

Beyond policy structure, H.3430 also imposes stricter requirements on certain venue types — particularly those near college campuses.

Special Provisions for Collegiate Venues (Effective May 2025)

Establishments at or near college sports venues face additional requirements that took effect immediately upon the Governor's signature:

- Mandatory server training for all sales personnel

- Random internal compliance checks

- Forensic digital ID systems at point of sale

- No beer or wine sales in student sections

- No sales to customers presenting vertical (under-21) ID cards

SC Liquor Liability Insurance: Requirements, Credits, and What Businesses Need to Know

The Baseline Requirement

On-premises licensees open past 5:00 p.m. must carry at least $1 million in liquor liability coverage (or a general liability policy with a liquor liability endorsement) on an annual aggregate basis. Failure to maintain coverage is grounds for permit suspension or emergency revocation.

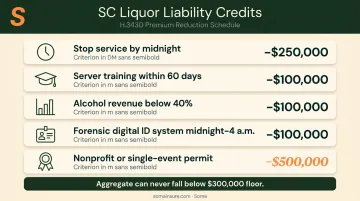

Five Credits That Can Reduce Your Required Aggregate

H.3430 creates a credit system that allows qualifying businesses to reduce their required minimum — but the aggregate can never fall below $300,000, regardless of how many credits apply.

| Credit | Reduction |

|---|---|

| Stop alcohol service by midnight for the full policy period | –$250,000 |

| All employees complete server training within 60 days of hire | –$100,000 |

| Alcohol revenue below 40% of total revenue | –$100,000 |

| Forensic digital ID system used between midnight and 4 a.m. | –$100,000 |

| Nonprofit or single-event special permit holder | –$500,000 |

A restaurant that closes the bar at midnight, keeps alcohol revenue under 40%, and completes server training could potentially reduce its required minimum to $550,000 — or lower depending on additional credits. Actual premium savings depend on carrier pricing, and businesses should confirm with a broker that their specific practices qualify for each credit.

Why Policy Type Now Matters More

The captive insurer restriction means defense costs under captive policies can no longer erode the coverage limit available to victims. For businesses with traditional (non-captive) admitted or surplus lines policies, eroding structures may still exist — and the difference can mean hundreds of thousands of dollars less available when a claim is paid.

Before renewal, ask your broker directly: is this policy eroding or non-eroding, and who issued it?

Market Conditions Worth Knowing

That question matters more now because the market for liquor liability has been under pressure for several years. Insurance Journal reported in March 2024 that some carriers were charging double or triple for this coverage, with high-volume accounts being pushed toward surplus lines markets. SC's new mandatory $1 million requirement has added further pressure, particularly for late-night establishments and venues with high alcohol revenue ratios.

Soma places liquor liability and hospitality coverage through carriers such as Markel, Nationwide, and Liberty Mutual — including for late-night bars, high-occupancy venues, and accounts with prior claims that standard markets often decline.

What SC Alcohol-Serving Businesses Should Do Right Now

Immediate Compliance Steps

- Enroll servers and managers in a SCDOR-approved training program and document completion. New hires must complete training within 30 days. Keep certificates on-site.

- Assess credit eligibility before your next renewal — closing at midnight, keeping alcohol revenue under 40%, installing forensic ID systems, and having trained staff all reduce your required aggregate minimum.

- Review your current policy for eroding vs. non-eroding structure and whether it was issued by a captive insurer. If you don't know the answer, ask your broker.

Documentation Practices That Matter in Litigation

In litigation, records determine whether a court finds "knowing" service — and that finding can shift the entire outcome. Maintain:

- Server training certificates (on-site, current)

- ID check logs and any forensic ID system records

- Incident logs documenting service refusals

- Revenue records if relying on the alcohol revenue credit

Work the Credit Structure at Every Renewal

The new credit system rewards operational discipline with lower required minimums — and potentially lower premiums. A business that stops serving at midnight alone saves $250,000 off the required aggregate. Combined with server training and a low alcohol revenue ratio, those savings add up quickly.

Model these scenarios with a broker experienced in SC hospitality coverage before each renewal. Keep in mind: credits require documentation to claim — the reduction doesn't apply without records to support it. A broker like Soma, which places liquor liability coverage across SC hospitality accounts, can help you identify which credits your operation already qualifies for.

Frequently Asked Questions

What is South Carolina's dram shop law?

SC dram shop liability comes from multiple statutes — primarily §61-4-580 (beer and wine) and §61-6-2220 (liquor) — along with court precedent, rather than a single codified act. It holds alcohol-serving businesses liable when they knowingly serve visibly intoxicated or underage patrons who go on to cause harm to a third party.

Can a bar be sued for a drunk driving accident in South Carolina?

Yes. If a bar knowingly served an already-intoxicated patron who then caused an accident, the establishment can be held liable alongside the drunk driver. Under H.3430 (effective January 1, 2026), the bar's share of joint and several liability is capped at 50% of the plaintiff's actual damages.

What changed about SC dram shop liability in 2026?

Three main changes: (1) establishment liability is now capped at 50% of actual damages rather than potentially 100%; (2) the "knowingly" standard now applies to liquor as well as beer and wine; and (3) mandatory server training is required for all servers and managers at on-premises licensed establishments.

What insurance does a bar or restaurant need in South Carolina?

SC requires at least $1 million in liquor liability coverage (annual aggregate) for on-premises licensees operating past 5:00 p.m. Businesses can reduce that required minimum through qualifying credits, but the aggregate can never fall below $300,000 regardless of how many credits apply.

What is the "knowingly" standard under SC dram shop law?

"Knowingly" means the server knew or should have known the patron was intoxicated or underage, based on observable cues that a reasonably prudent person would recognize. Courts focus on what the server observed or could have observed in the moment.

How can a SC bar reduce its required liquor liability insurance minimum?

Available credits include:

- Stopping service by midnight: –$250,000

- Completing server training within 60 days of hire: –$100,000

- Keeping alcohol revenue below 40% of total revenue: –$100,000

- Using forensic ID systems between midnight and 4 a.m.: –$100,000

- Nonprofit or single-event status: –$500,000

Coverage can never be reduced below the $300,000 floor regardless of credits applied.