Introduction

The modern craft brewery isn't just a production facility — it's a hospitality venue. Taprooms, tours, ticketed events, and on-site tastings now define the business model, and that shift carries serious liability exposure most owners underestimate.

Many brewery owners treat liquor liability as a compliance formality. That's a costly mistake. A single overserving incident that ends in a DUI fatality can trigger a dram shop lawsuit with damages that dwarf the brewery's annual revenue. In states with no cap on dram shop damages, there's no ceiling on what a jury can award.

What follows is a data-driven look at claim patterns, legal trends, and real exposure benchmarks — so brewery owners can make informed decisions about coverage before a claim forces the issue.

TL;DR

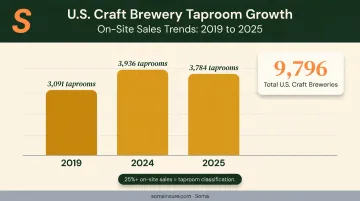

- The U.S. had 9,796 operating craft breweries in 2024, with nearly 4,000 taprooms serving alcohol directly to the public

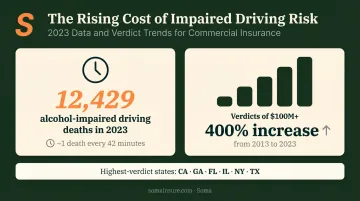

- 12,429 people died in alcohol-impaired driving crashes in 2023, creating dram shop exposure for the last establishment that served the driver

- Each of those incidents traces back to a licensed premises — making liquor liability coverage a direct operational concern

- California ABC decoy operations found 15–16% violation rates at licensed premises, making underage service a persistent operational risk

- Dram shop laws vary sharply by state; Texas and New York create significantly broader commercial liability than California or Florida

- Staff training and adequate policy limits remain the two most direct ways to reduce exposure and improve underwriting outcomes

The Craft Brewery Industry: Growth, Taprooms, and Rising Liability Stakes

A Taproom-Forward Business Model

According to the Brewers Association's 2024 industry report, there were 9,796 operating craft breweries in the U.S. in 2024. That same year, 3,936 taproom breweries were in operation — defined by the BA as establishments that sell 25% or more of their beer on-site without operating significant food services.

The taproom count has grown substantially from 3,091 in 2019, though it dipped slightly to 3,784 in 2025. The directional story is clear: on-premises alcohol service is now central to how craft breweries operate and generate revenue.

This shift matters for insurance. A brewery that only wholesales kegs to bars has a very different liability profile than one running weekend taproom hours, private event rentals, and ticketed beer releases. Once alcohol is served across the bar, the brewery becomes legally responsible for what happens next.

Scale Makes Survival Harder

The BA defines a craft brewer as producing 6 million barrels or fewer annually — roughly 3% of total U.S. beer sales volume. Most craft breweries produce far less than that ceiling. These are small, independently owned businesses operating on thin margins.

That scale matters in a liability context. Consider the gap between how different operators absorb the same claim:

- A national beer conglomerate can treat a seven-figure legal judgment as a line item

- A 15-barrel taproom in its fifth year likely cannot survive one

- Most craft breweries carry fewer than 10 employees and no dedicated legal or risk management staff

- Defense costs alone — before any settlement — can run into six figures

For small craft breweries, a single catastrophic liquor liability claim doesn't just hurt the bottom line. It can force closure before a verdict is even reached.

Key Liquor Liability Statistics Craft Breweries Need to Know

The DUI Connection Is the Core Exposure

NHTSA reported 12,429 alcohol-impaired driving deaths in 2023 — nearly one-third of all U.S. traffic fatalities. That works out to roughly one death every 42 minutes.

Every one of those incidents is a potential dram shop case. Under dram shop statutes, the last establishment that served the driver can be named in the resulting lawsuit. Craft brewery taprooms, where patrons may drive home after a flight of high-ABV beers, sit squarely in that exposure window.

Verdicts Can Be Catastrophic

Brewery-specific settlement averages aren't publicly tracked, but the hospitality sector produces extreme outcomes. In December 2019, a Texas jury awarded over $301 billion in a drunk-driving dram shop case — a figure described as largely symbolic given the defendant bar had closed. More relevant to smaller operators: Insurance Journal reported 27 U.S. court cases with awards exceeding $100 million in 2023, with verdicts above that threshold increasing nearly 400% from 2013 to 2023. California, Georgia, Florida, Illinois, New York, and Texas accounted for 61% of those large verdicts.

Underage Service Is a Persistent Operational Risk

California ABC compliance data shows 15–16% violation rates across thousands of licensed premises visited during decoy operations. Statewide, 7,747 premises were visited in one reporting period with 1,234 arrests resulting.

That's not a fringe problem. In busy taprooms with high traffic and multiple staff working simultaneously, a failed ID check is entirely plausible. The consequences compound quickly: underage service triggers both civil liability and administrative penalties (fines, license suspension) simultaneously. Those dual exposures translate directly into higher premiums at renewal.

Premium Trends Signal Industry-Wide Pressure

While brewery-specific premium data isn't publicly available, hospitality sector benchmarks tell the story directionally. CRC Group reports that clean liquor liability accounts in stressed markets are now seeing premiums between $25,000 and $50,000.

South Carolina examples illustrate how fast costs escalate:

- One bar went from $8,000 to $54,000 in two years

- Another jumped from $6,000 in 2020 to $65,000 in 2025

Across commercial P/C lines overall, premiums rose 7.7% in Q1 2024 — the 26th consecutive quarterly increase.

These increases reflect rising claim frequency and severity, not just market cycles. Underwriters are pricing in taproom-specific risks: high-ABV products, self-pour formats, and late-night service windows that other hospitality operators don't carry.

Most Common Liquor Liability Claims at Craft Breweries

Overserving and Off-Premises Incidents

The most financially severe claims typically don't happen inside the taproom. When a patron leaves visibly intoxicated and causes a crash, the brewery can be named in the resulting lawsuit — even though the incident occurred miles away. Under dram shop law, a brewery's liability doesn't end at the door — it follows the patron.

Underage Service

High-volume taproom environments create conditions where ID verification breaks down. Common failure points include:

- Sudden rushes at the bar during peak hours

- Multiple concurrent events with overlapping crowds

- Temporary or event-specific staff unfamiliar with verification protocols

Both civil damages and license-level penalties apply when a minor is served. The combination can be far more damaging than either alone.

Tour and On-Premises Injuries

Brewery tours compound liability in a specific way: guests are drinking while navigating production floors that include wet surfaces, stairs, fermentation tanks, and industrial equipment. A patron's intoxication both increases the likelihood of injury and can increase the brewery's degree of fault in the resulting claim.

Event and Festival Liability

Craft breweries increasingly host ticketed releases, private events, and participate in beer festivals. Two risks come with this territory:

- On-site events bring larger crowds and potentially unfamiliar event staff into the taproom

- Off-premises events (festivals, pop-ups) may not be automatically covered under a standard liquor liability policy — breweries need to verify policy language and add appropriate endorsements

High-ABV Products Accelerate the Risk

Craft beer's ABV range separates it sharply from mass-market products — and that gap matters for liability. Per Brewers Association style guidelines:

| Beer Style | ABV Range |

|---|---|

| American-style Lager | 4.1%–5.1% |

| American-style IPA | 6.3%–7.5% |

| Imperial/Double IPA | 7.6%–10.6% |

| Barley Wine / Wheat Wine Ale | 8.5%–12.2% |

| Dessert/Pastry Beer | 7% to 13%+ |

A patron drinking a flight of double IPAs reaches intoxication significantly faster than someone drinking domestic lager — and often without fully registering it. Some insurers and courts have factored ABV into their assessment of a brewery's liability for downstream incidents.

Dram Shop Laws and State-Level Liability Exposure

What Dram Shop Laws Actually Do

Dram shop statutes create a direct legal mechanism for holding alcohol-serving establishments liable for damages caused by intoxicated patrons. Most U.S. states have them, but the scope varies significantly. Research from the Community Guide found that dram shop liability laws were associated with a median 6.4% reduction in alcohol-related motor-vehicle deaths — a signal that courts and insurers treat these statutes seriously.

According to Justia's 50-state survey, states currently without dram shop statutes include Delaware, Kansas, Maryland, South Dakota, and Virginia. In states with statutes, damages caps vary widely:

- Connecticut: $250,000 cap

- Maine: $350,000 (excluding medical expenses)

- North Carolina: $500,000 per occurrence

- New Mexico: $50,000 per person / $100,000 multiple persons

Where Exposure Is Highest

Among the states where Soma operates, statutory analysis shows meaningful differences:

- Texas: Liability arises when it was apparent the person served was "obviously intoxicated to the extent the person presented a clear danger to self and others." The statute imposes no damages cap, creating broad commercial exposure.

- New York: New York's General Obligations Law (GOL 11-101) allows recovery including actual and exemplary (punitive) damages for injuries caused by unlawful alcohol sales. No statutory cap applies.

- California: BPC 25602 generally places proximate cause of harm on the act of drinking rather than on serving (furnishing) alcohol, creating narrower exposure for adult service. BPC 25602.1 carves out a direct liability exception for serving an obviously intoxicated minor.

- Florida: Generally bars liability for furnishing alcohol to adults of lawful drinking age; liability can arise for willful unlawful service to minors or to known habitual drunkards.

Coverage Limits Need to Match the State

Some states have already moved to mandate minimum coverage. South Carolina requires $1 million minimum liquor liability coverage for licensed establishments. Indiana enacted a $500,000 minimum effective July 1, 2024.

Standard policies at $1M per occurrence / $2M aggregate may fall short in unlimited-damages states like Texas or New York. Consider whether your current structure covers:

- Catastrophic injury claims that exceed base policy limits

- Punitive damages in states where they're available (New York being a key example)

- Multi-claimant incidents where aggregate limits erode quickly

Umbrella or excess coverage is often necessary to bridge the gap between base policy limits and realistic worst-case exposure.

How Craft Breweries Can Reduce Liquor Liability Exposure

Staff Training

Responsible beverage service (RBS) training programs — including TIPS, LEAD, and state-mandated programs — give staff concrete tools for identifying signs of intoxication and handling refusals. Research shows RBS training increases refusals of service to visibly intoxicated customers — particularly when management actively reinforces the protocols.

California has made RBS training mandatory for on-premises servers since July 1, 2022, including brewery tasting rooms. Servers must register, complete approved training, and pass the ABC exam within 30 days of employment. Certification lasts three years. Even in states where training isn't required, many carriers view documented training programs favorably in the underwriting process.

Operational Protocols That Reduce and Document Risk

Training alone isn't enough without supporting systems:

- ID-checking procedures documented consistently, especially during high-volume taproom shifts

- Pour limits or drink tracking during ticketed events

- Safe-ride partnerships (Uber/Lyft codes, visible signage) that demonstrate proactive harm reduction

- Event-specific staffing plans with staff-to-patron ratios

Documentation matters as much as the protocols themselves. A brewery that can demonstrate it followed established best practices is in a materially stronger legal position than one that cannot.

Getting Coverage That Matches Your Actual Exposure

That documentation also matters when it's time to select coverage. Many craft brewery owners default to whatever coverage came with their general liability package — which often undershoots actual liquor exposure, particularly for high-ABV products, large events, or off-premises distribution.

Soma places hospitality and liquor liability coverage through carriers including Markel, Nationwide, and Liberty Mutual, and structures policies around a brewery's actual operations rather than a generic hospitality template. This includes accounts that standard markets decline: high-occupancy venues, operations with prior claims, and complex mixed-use facilities.

Frequently Asked Questions

What is liquor liability insurance, and do all craft breweries need it?

Liquor liability insurance covers claims arising from a brewery's sale or service of alcohol — overserving incidents, service to minors, and downstream injuries caused by intoxicated patrons. Any brewery serving alcohol on-site or distributing to bars and restaurants faces this exposure and should carry a dedicated policy, separate from general liability.

What are the most common triggers for liquor liability claims at craft breweries?

The three highest-frequency triggers are overserving that leads to off-premises DUI incidents, serving minors (particularly in high-volume taproom settings), and on-premises injuries during tours or events where patrons have consumed alcohol.

How much does liquor liability insurance typically cost for a craft brewery?

No verified brewery-specific average exists, but hospitality benchmarks show premiums for clean accounts ranging from $25,000 to $50,000 in hardening markets. Key cost drivers include taproom revenue, event frequency, prior claims history, and your state's dram shop liability exposure.

Does liquor liability coverage extend to off-premises events and beer festivals?

Standard policies do not automatically extend to off-premises events. Breweries participating in festivals, pop-ups, or external activations should review their policy language and confirm with their broker whether an endorsement or event-specific policy is needed.

What states have the strictest dram shop laws for craft breweries?

Texas and New York present the broadest exposure: neither caps damages under their statutes, and New York permits punitive awards. California and Florida carry narrower but real exposure for underage or high-risk service. Consult a broker familiar with your state's laws before setting coverage limits.

How can a craft brewery lower its liquor liability insurance premium?

The most effective levers are documented responsible beverage service (RBS) training, consistent ID verification protocols, and a clean claims history. Carriers weigh management practices heavily in underwriting, so written procedures translate directly into better pricing conversations — especially when placed through a broker who specializes in craft brewery coverage.