With over 70,000 bars and nightclubs operating across the US, the stakes are high. A single uncovered liquor liability claim can run into six or seven figures. This guide breaks down what bar insurance actually costs, which policies you need, what drives premiums up or down, and where most owners leave themselves exposed.

TL;DR

- Most bars spend $5,000–$12,000 per year across all required policies; nightclubs routinely exceed $20,000.

- Liquor liability is a separate policy from general liability. Standard GL won't cover alcohol-related incidents — and one drunk-driving lawsuit without it can be financially devastating.

- Most GL policies exclude assault and battery outright. Without a separate endorsement, bar fight claims are typically denied at the door.

- Alcohol sales percentage, operating hours, and entertainment type drive costs the most — and adjusting them is the fastest way to lower your premiums.

How Much Does Bar Insurance Cost?

Bar insurance doesn't have a single price. Total cost depends on venue type, risk profile, geographic location, and which policies you're stacking. Underestimating these costs leads to two common mistakes: owners either underinsure and carry dangerous gaps, or they buy generic policies that miss hospitality-specific exposures entirely.

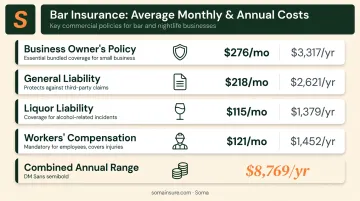

The most reliable way to understand costs is at the individual policy level. According to Insureon's bar insurance cost data (updated October 2024):

| Policy | Average Monthly Cost | Average Annual Cost |

|---|---|---|

| Business Owner's Policy (BOP) | $276/month | $3,317/year |

| General Liability | $218/month | $2,621/year |

| Liquor Liability | $115/month | $1,379/year |

| Workers' Compensation | $121/month | $1,452/year |

These are averages. A bar's actual stack will vary based on venue type and risk factors.

Small Neighborhood Bar or Tavern

A low-risk neighborhood bar — limited entertainment, moderate alcohol volume, earlier closing hours — sits at the lower end of the spectrum. Stacking the core policies above, most taverns in this category pay $5,000–$9,000 per year across their full coverage program. Key characteristics that keep costs down: no dance floor, closing before midnight, food service alongside alcohol, and a clean claims history.

Sports Bar

Sports bars carry more risk than neighborhood taverns. Crowd surges during games, extended weekend hours, and high alcohol volume all push premiums higher. Expect $8,000–$15,000 per year for a typical sports bar, with the upper range applying to large-format venues running late hours on game nights.

Nightclub or High-Volume Venue

Nightclubs sit at the top of the cost range. Dance floors, DJs, late-night operations past 2 a.m., and high-capacity crowds create a fundamentally different risk profile. Premiums for this category can reach $25,000–$50,000 or more annually, and some venues — particularly those with prior claims history or aggressive entertainment programming — face even higher costs or outright declinations from standard markets.

Bar type is the single most impactful variable underwriters evaluate — and it's why two bars on the same block can carry very different premiums.

What Types of Insurance Do Bars Need?

No single policy is sufficient for a bar. Most owners need several coverage types working together — and the gaps between those policies, particularly around liquor liability and assault and battery, are exactly where the most expensive claims tend to fall.

General Liability Insurance

GL covers the basics: customer slip-and-falls, property damage caused by bar staff, and advertising injury claims. Standard limits are $1 million per occurrence / $2 million aggregate, and bars pay an average of $218/month ($2,621/year) for this coverage.

What GL does not cover: alcohol-related injuries, assault and battery incidents, or claims arising from entertainment. For a bar, GL alone is a starting point — not a complete insurance program.

Liquor Liability Insurance

Liquor liability is a standalone policy — the standard ISO Commercial General Liability form explicitly excludes claims arising from the business of selling or serving alcoholic beverages. Most bar owners don't realize this until they have a claim.

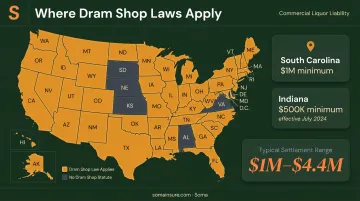

Why it matters: 43 states and the District of Columbia have some form of dram shop law, which means bars can be held legally responsible when an intoxicated patron causes injury or death after leaving the premises. Settlements in these cases routinely reach $1 million to $4.4 million.

Average cost: $115/month ($1,379/year) — though this figure rises sharply with alcohol sales volume. The primary pricing variable is the percentage of total revenue that comes from alcohol sales. Some states also mandate minimum coverage limits: South Carolina requires at least $1 million; Indiana (effective July 1, 2024) requires $500,000.

Business Owner's Policy (BOP)

A BOP bundles general liability and commercial property insurance at a lower combined rate than buying both separately. Bars pay a median of $276/month ($3,317/year) for a BOP, which covers the physical space — equipment, furniture, inventory, sound systems, glassware, and signage.

One important caveat: not all bars qualify. Carriers restrict BOP eligibility based on operating hours, entertainment type, and venue capacity. High-risk operations — nightclubs, late-night venues, large-capacity bars — typically need a commercial package policy instead.

Workers' Compensation Insurance

Bar staff face above-average injury risk: late hours, alcohol in the environment, glass, kitchen hazards, and physical altercations all contribute. Workers' comp covers medical costs and lost wages for injured employees — bartenders, barbacks, kitchen staff, and security personnel alike.

Average cost for bars: $121/month ($1,452/year). Coverage requirements vary by state:

- Most states: Required as soon as you have any employees

- Texas: Optional for most private employers

- Ohio, North Dakota, Washington, Wyoming: Required, but must be purchased through the state fund — not a private carrier

Assault and Battery Coverage

This is the most dangerous gap in a standard bar insurance program. ISO form CG 40 51 01 26 is an endorsement that explicitly excludes bodily injury arising from assault or battery — and bar and nightclub policies frequently include this exclusion either by default or as a sublimit.

Without an A&B endorsement, claims from bar fights, bouncer incidents, and parking lot altercations result in a flat coverage denial. A&B endorsements typically carry sublimits of $100,000–$500,000.

Standalone A&B policies can provide $500,000–$1 million in coverage. Physical altercations are among the most frequently reported incidents at bars — a single uninsured fight can generate a six-figure claim with no policy response.

Key Factors That Drive Bar Insurance Costs

Underwriters evaluate bar accounts across several specific dimensions. Understanding these helps you anticipate what you'll pay — and where you have real leverage to lower premiums.

Alcohol Sales Percentage

The ratio of alcohol revenue to total revenue is one of the most closely watched underwriting metrics. Businesses with alcohol revenue above 30% face increasingly difficult coverage conditions as that percentage climbs toward 50–75%. A bar where alcohol represents 80% of revenue pays dramatically more for liquor liability than a restaurant where drinks represent 20% of sales.

Practical implication: adding a food menu or expanding food offerings can noticeably reduce this ratio and lower your liquor liability premium.

Operating Hours

Late-night hours correlate directly with claim frequency. Research published in Alcohol and Alcoholism found that each one-hour change in bar closing times was associated with roughly a 16% change in violent incidents in city centers during weekend nights. Underwriters price this relationship directly.

Bars closing past midnight pay more; those open past 2 a.m. pay significantly more. Even shifting closing time by one hour can affect your renewal premium.

Type of Entertainment Offered

Each entertainment type adds incremental risk — and incremental cost. Live music brings stage liability and sound equipment exposure. DJ nights and dance floors increase altercation risk. Karaoke and hosted events add slip-and-fall and ticketing liability. Mechanical bulls and similar attractions typically fall outside standard bar policy terms entirely and require separate event coverage.

Before booking entertainment, confirm your policy explicitly covers performer injury and rented equipment — most standard bar policies do not.

Location and Legal Environment

Location affects premiums two ways: physical risk (local crime rates, natural disaster exposure) and legal environment. States with aggressive dram shop statutes and high claim frequencies push liquor liability rates up — not just locally, but across carriers' national books.

The scale of that pressure becomes concrete when you look at specific markets. In South Carolina, insurers have lost $1.77 for every $1.00 of premium earned since 2017, and some bars have seen annual premiums jump from $8,000 to $54,000 within two years.

Claims History and Security Measures

Prior assault, liquor liability, or slip-and-fall claims can significantly increase premiums at renewal — or trigger a declination. A bar with documented security protocols and a clean claims record occupies a very different underwriting position. Security investments that improve that profile include:

- Surveillance camera systems covering entrances, bar areas, and parking

- ID scanners with age-verification logs

- TIPS-certified bartenders and servers (recognized by over 70 insurance companies nationwide for potential premium discounts)

- Written policies for handling intoxicated patrons and closing-time procedures

- Trained, documented security staff

What Most Bar Owners Miss About Insurance Costs

The Assault and Battery Gap

Most bar owners assume their general liability policy covers what happens when a fight breaks out. It almost never does. Without a specific A&B endorsement, any claim arising from a physical altercation — bar fight, bouncer incident, parking lot confrontation — gets denied. This is the most common and most costly gap in a standard bar insurance program, and it's entirely avoidable.

Focusing Only on the Upfront Premium

The cheapest policy is rarely the cheapest outcome. A low-premium policy that excludes A&B, liquor liability, and entertainment exposures leaves the business exposed to uncovered claims that can easily exceed $500,000. The real cost comparison is premium paid versus maximum uninsured loss — and that math rarely favors the bargain policy.

Failing to Update Coverage After Operational Changes

Making operational changes without notifying your insurer can give the carrier grounds to deny a claim entirely. Common triggers include:

- Adding live entertainment or DJ nights

- Extending operating hours

- Hiring security or door staff

- Renovating or expanding the physical space

Policies should be reviewed at least 60 days before renewal. Any of these changes warrants an immediate conversation with your broker — not a note left for the next renewal cycle.

For bar owners with complex or hard-to-place programs, working with a specialized broker like Soma — which places late-night venues, high-occupancy nightclubs, and accounts with prior claims history — can help ensure coverage coordinates properly across carriers and gaps don't develop between renewals.

How to Lower Your Bar Insurance Costs

Invest in Staff Training and Documented Safety Protocols

TIPS certification is recognized by over 70 insurance companies nationwide as grounds for potential liquor liability premium discounts. Beyond the discount, documented responsible-service policies — written procedures for handling intoxicated patrons, checking IDs, managing last-call crowds — give underwriters evidence of proactive risk management. They also strengthen a legal defense if a dram shop claim goes to trial.

Bundle Policies and Compare Multiple Carriers

Combining GL and property coverage into a BOP saves money versus buying separately. Specialty hospitality carriers often bundle liquor liability and A&B into a single program, which eliminates the gap risk that exists when those coverages sit with different carriers. Get at least three quotes, and make sure at least one comes from a carrier that specializes in bar and nightclub accounts — standard commercial insurers frequently don't understand this risk category.

Reduce Operational Risk Factors Where Possible

Carrier pricing reflects operational behavior, not just coverage history. These four changes have documented underwriting impact:

- Add food service to reduce your alcohol-to-revenue ratio and lower liquor liability costs

- Close one hour earlier — late-night hours correlate directly with claim frequency

- Install cameras and ID scanners as documented security infrastructure

- Train and certify security staff to reduce A&B claim probability and strengthen your defense posture

Bars that file a claim with none of these in place typically face steep renewal increases. Bars that document their risk management investments beforehand give underwriters a reason to hold — or lower — their premiums at renewal.

Frequently Asked Questions

How much does it cost to insure a bar?

Most bars pay $5,000–$12,000 per year across their full coverage stack, including GL, liquor liability, property, and workers' comp. High-volume nightclubs and late-night venues can exceed $25,000–$50,000 annually depending on risk profile and coverage limits.

What kind of insurance do bars need?

The core stack includes general liability, liquor liability, a BOP or commercial property policy, and workers' compensation. Most bars also need assault and battery coverage as an endorsement or standalone policy, and high-entertainment venues may need additional event coverage.

Is liquor liability insurance the same as general liability insurance?

No, they are separate policies. The standard GL form explicitly excludes claims arising from the sale or service of alcohol. In any state with dram shop laws (43 states plus DC), operating without standalone liquor liability means a bar owner can be held personally liable for damages.

Does general liability insurance cover bar fights?

Most standard GL policies exclude assault and battery, meaning fight-related claims are denied without a separate A&B endorsement. This exclusion applies regardless of whether the bar's staff was directly involved.

How can bar owners lower their insurance premiums?

The most effective cost levers include:

- TIPS-certifying staff (recognized by 70+ carriers for premium discounts)

- Bundling policies with a specialty hospitality insurer

- Adding food service to lower your alcohol revenue percentage

- Maintaining a clean claims record with documented security protocols

Why might a bar be denied insurance coverage?

Common reasons include:

- Multiple prior claims or a history of assault incidents

- Very late operating hours (past 2 a.m.)

- High alcohol-to-food revenue ratios

- No documented security protocols

Specialty brokers who work in hard-to-place markets can often find coverage where standard carriers decline.