For contractors, construction business owners, and project estimators, understanding how GL premiums are built is genuinely useful. The calculation isn't arbitrary. It follows a formula driven by your trade type, your revenue or payroll, your location, and your claims record. Get any of those inputs wrong — or let your subcontractor COI file go stale — and an audit can surface a bill that wipes out margin on an entire project.

This article breaks down the full calculation process, from initial class code assignment through year-end audit reconciliation, and covers the most common places contractors get caught off guard.

TL;DR

- Your GL premium quote is a deposit on estimated risk — the carrier reconciles it against your actual financials at the year-end audit.

- The two biggest cost drivers are your trade class code (sets the base rate) and your exposure base (gross receipts or payroll), which scales the premium to your actual business volume.

- Uninsured subcontractors are the most common audit trap — carriers reclassify their payments as your payroll if you can't produce valid COIs.

- Claims history, geographic location, and coverage limits all function as modifiers that push your final rate up or down.

- A broker with access to multiple carriers ensures you're correctly classified from day one, so you're not overpaying on a mismatched code.

How GL Insurance Premiums Are Calculated for Contractors

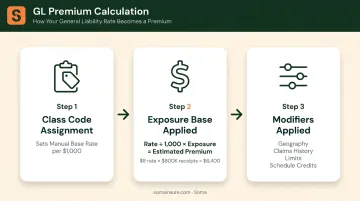

The California Department of Insurance describes commercial GL rating using a straightforward formula: rate × exposure = premium. For contractors, that breaks down into three sequential steps.

Step 1: Trade Classification Is Assigned

Before any numbers are run, the underwriter assigns an ISO class code that matches your type of work. Verisk defines approximately 1,000 class codes used to determine the appropriate loss cost for a given operation.

ISO's 2024 GL update added over 100 new classifications — including a split between residential and commercial project work for contractors.

The class code does two things: it identifies the nature of the work and sets the manual base rate — the dollar amount charged per $1,000 of exposure. A roofing contractor and an interior painter may have similar revenues, but their base rates reflect very different historical loss profiles.

Getting that code wrong has real consequences:

- A contractor filed under a lower-risk code may face coverage denial if a claim falls outside that code's scope

- A GC coded as a specialty trade can face audit penalties when actual operations don't match

Step 2: Exposure Base Is Applied

Once the class code is established, the base rate is multiplied by the contractor's exposure base. According to Frankenmuth's 2024 Premium Audit Guide, GL premium bases include:

- Gross sales — total charged for operations, rentals, and fees (excluding taxes)

- Payroll — used for certain artisan trade codes (rough carpentry, interior carpentry, and similar)

- Total cost — the sum of all subcontracted work, including labor, materials, equipment, and fees

The Big I confirms that ISO's Commercial Lines Manual applies "Total Cost" rates per $1,000 of total cost for contractor and subcontractor placements. The formula works like this:

(Rate per $1,000 ÷ 1,000) × Exposure = Estimated Premium

A contractor projecting $800,000 in gross receipts for the year, assigned a class code with a rate of $8 per $1,000, would produce a raw estimated premium of $6,400 before any modifiers are applied.

Step 3: Modifiers and Adjustments Are Applied

The raw calculation is a starting point. Underwriters then layer on rating factors that shift the final number:

- Geographic territory — state and local conditions act as multipliers on the base

- Claims history — prior losses trigger surcharges; clean records may qualify for preferred pricing

- Coverage limit adjustments — higher per-occurrence or aggregate limits increase cost

- Schedule credits — documented safety programs or industry certifications can reduce the final rate

The premium produced after these adjustments becomes your deposit premium — the carrier's best estimate at policy inception. Because actual revenues, payroll, or subcontractor costs often differ from projections, the true cost is only confirmed at year-end audit.

Key Factors That Determine Your GL Premium

Trade Class Code and Work Type

The class code is the single biggest lever in the calculation. High-severity trades — roofing, excavation, framing — carry substantially higher base rates than lower-severity work like interior painting or flooring installation. The difference reflects decades of loss data tied to injury frequency, property damage severity, and completed operations claims by trade.

ISO's 2024 update further refined this by separating residential and commercial project classes for contractors, recognizing that the liability exposures on a commercial job site differ meaningfully from residential remodeling work.

Gross Receipts, Payroll, and Subcontracted Costs

These are the volume inputs that scale your premium up or down. More revenue means more job sites, more workers, and statistically more claims exposure. Three things worth knowing:

- Gross receipts is the primary exposure base for most contractor GL policies

- Payroll applies to specific artisan trade codes

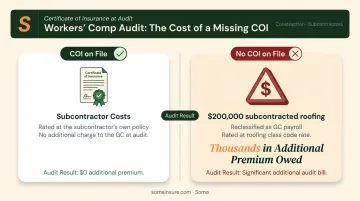

- Subcontracted costs are rated separately — but only if valid COIs exist for those subs

When COIs are missing, the auditor treats subcontractor payments as your own direct payroll, rated at the sub's trade class code. For a GC who subcontracted $200,000 in roofing work without collecting COIs, that entire amount gets reclassified and rated at roofing rates during audit. That reclassification can easily add thousands to the audit bill.

Geographic Location

Verisk identifies territory as one of three foundational inputs for any GL quote, alongside exposure and class code. State and local conditions — litigation climate, construction defect statutes, local labor laws, and property values — all function as multipliers on the base rate.

New York is a documented example. Two state statutes drive costs well above national averages for contractors working there:

- NY Labor Law 240: Imposes strict liability on owners, GCs, and agents for gravity-related injuries on covered construction work

- NY Labor Law 241: Requires safe conditions across all construction, excavation, and demolition sites

Neither statute has a direct equivalent in most other states, and carriers price both into every NY contractor GL policy written.

Claims History

Underwriters evaluate three to five years of loss run reports when pricing a renewal. Hamilton's Contractors Supplemental Application, for example, requires loss runs dated within 60 days of submission and covering the past five years.

What the loss runs communicate:

- Frequency — multiple small claims often concern underwriters more than a single large one

- Severity — large paid losses or open reserves signal potential for future exposure

- Trend — worsening patterns over recent years push rates up at renewal

New businesses without loss run history get priced conservatively by default — underwriters treat an unknown risk as standard or above-standard until a clean track record is established.

Coverage Limits and Deductibles

The standard limit structure for contractor GL typically starts at $1M per occurrence / $2M aggregate, as Hartford notes for most industries. Choosing higher limits increases premium, though the incremental cost per additional million tends to decrease as limits rise.

Raising your deductible reduces the upfront premium but transfers more out-of-pocket risk per claim. For contractors with strong cash flow and a clean loss history, this is a reasonable trade. For new businesses or high-frequency trades, a lower deductible provides more predictable cost control.

Umbrella or excess liability policies can extend coverage limits beyond the underlying GL policy — often more cost-effectively than buying higher primary limits outright.

How Year-End Audits Affect Your Final GL Premium

Why Audits Exist

Contractor revenues, payroll, and subcontractor usage all fluctuate throughout the year. The carrier's upfront premium is based on projections, not actual figures. At policy end, the carrier reconciles verified financial records against those projections. If actual exposure exceeded estimates, you owe additional premium. If actual exposure came in lower, you may receive a return — though many construction policies carry minimum premium provisions that limit how much you can get back.

Audit Formats

According to Frankenmuth's audit guide, carriers use three formats depending on contractor size and risk complexity:

- Mail/online self-report — for smaller, straightforward accounts

- Phone/virtual — remote review of digital records, used for mid-tier accounts or special circumstances

- In-person physical audit — for larger contractors, complex operations, or high subcontractor volume

The Uninsured Subcontractor Penalty

This is where most surprise audit bills originate. When a contractor cannot produce a valid COI covering the audit period for a subcontractor, the auditor charges those payments based on the type of work performed — typically at the total cost rate for the sub's trade classification.

For general contractors who regularly use specialty trade subs, keeping a current COI file is an operational finance issue, not just a paperwork one. The practical steps:

- Require COIs before any subcontractor starts work

- Verify the coverage period extends through the work dates

- Maintain a separate record of materials vs. labor costs in subcontractor payments — auditors can reduce the ratable exposure when records clearly separate material costs

Consequences of Ignoring an Audit

Audit noncompliance is expensive. Integrity Insurance notes a penalty of up to 2x the estimated annual premium. Frankenmuth's guide states that some states allow charges up to 3x the estimated premium. The specific multiplier depends on the carrier and state.

Beyond the financial penalty, noncompliance affects renewal eligibility and restricts future access to standard A-rated carriers. Once flagged for noncompliance, contractors are typically forced into the surplus lines market — where premiums run higher and coverage terms are less favorable.

Common Misconceptions About GL Calculation

"My Quote Is My Final Cost"

Contractors who treat the initial premium as a fixed expense get caught when revenues or payroll come in higher than projected. The quote is a deposit against estimated risk. Mid-year tracking of actual financials against projected figures allows you — or your broker — to request adjusted installments before the audit closes, smoothing out the final settlement.

"All Contractors Are Rated the Same Way"

General contractors, artisan trade contractors, remodeling contractors, and subcontractors are assigned different class codes, rated using different exposure bases and rates. A contractor filed under the wrong code — whether intentionally or by default — can face audit penalties when actual operations don't match, or find a claim denied because the work type wasn't covered under the assigned classification.

Classification decisions happen at submission, not after problems arise. Soma's Risk Management Team works with carrier partners including Chubb, Liberty Mutual, and Kinsale to get the right code placed from day one — because a correct classification is what holds up at audit and at claim time.

"Subcontractor Payments Don't Affect My Premium"

Subcontracted costs are a rated exposure on most contractor GL policies. Whether those costs increase your own premium depends entirely on whether valid COIs exist. With COIs, the risk transfers to the sub's policy. Without them, the exposure lands on yours — rated at the sub's trade class code, which may be considerably higher than your own.

Frequently Asked Questions

How much does $1,000,000 general liability insurance cost?

According to Hartford's contractor GL data, construction businesses average $1,351 per year for GL coverage, with contractors paying around $824 per year for a $1M policy. High-risk trades like roofing or excavation, and high-litigation states like New York, will push actual costs well above these figures.

Is general liability insurance based on payroll or gross receipts for contractors?

It depends on the class code. Certain artisan trades use payroll as the exposure base, while most contractor GL policies for larger operations use gross receipts. Subcontracted costs are typically rated separately, with the treatment determined by whether valid COIs are on file.

What happens if my actual revenue exceeds my estimated premium at audit?

The carrier issues an additional premium bill. The calculation applies the policy's base rate to the excess exposure beyond what was originally projected. Minimum premium provisions are common in construction policies, meaning underestimates don't always produce equal return credits in the other direction.

Does a new contracting business pay more for general liability insurance?

Yes. Without multi-year loss run history, underwriters default to more conservative pricing. Carriers typically request years in business, prior trade experience, and principal CVs for operations under three years old — documenting these thoroughly at submission can help moderate initial costs.

How does my trade classification affect my GL premium calculation?

The class code sets the manual base rate per $1,000 of exposure. A roofing contractor and an interior painting contractor running identical revenues will produce very different premiums because the base rates tied to their respective class codes reflect their trade's loss history. The rate gap between low- and high-hazard trades can easily double or triple the final premium on the same revenue figure.

Can I lower my general liability premium after filing a claim?

Premiums typically increase at renewal following a claim. Over time, documented safety programs and a clean subsequent record help offset the increase — and shopping coverage across multiple carriers matters, since each weights loss history differently.