Introduction

Independent contractors now represent a substantial slice of the U.S. workforce. The Bureau of Labor Statistics reported 11.9 million people working as independent contractors as their primary job — and MBO Partners counted 72.9 million total independent workers in 2025, spanning delivery drivers, construction tradespeople, field service professionals, and gig workers across every sector.

What most of these workers share: a vehicle they use for business, and a personal auto policy that won't cover them when it matters.

Commercial auto insurance for independent contractors typically runs $100 to $400+ per vehicle per month in 2026, depending on vehicle type, coverage level, state, and how heavily the vehicle is used for work.

Skipping proper coverage — or buying the wrong policy type — can mean a fully denied claim, personal liability for third-party injuries, and no vehicle repair coverage at all.

Here's what 1099 workers need to know: 2026 cost benchmarks, the coverage types that actually apply, what drives premiums up or down, and how to avoid paying for the wrong policy.

TL;DR

- Cost range: Roughly $100–$400+ per vehicle per month; averages run ~$245/month for small fleets and ~$272/month for contractor vehicles

- Higher costs: Daily high-mileage use, heavy vehicles, new businesses without loss history, high-litigation states, and elevated liability limits

- Lower costs: Clean driving records, light or occasional business use, lighter vehicles, bundled policies

- Most important: Personal auto nearly always excludes business use. One at-fault accident while working can result in a fully denied claim.

How Much Does Independent Contractor Auto Insurance Cost in 2026?

Commercial auto insurance does not have a single fixed price. Two contractors with identical vehicles can pay very different premiums based on what they haul, how far they drive, and what state they operate in. Budgeting without understanding these variables leads to one of two problems: being underinsured when a claim hits, or overpaying for coverage that doesn't fit the actual risk.

The two most common mistakes:

- Assuming a personal auto policy covers work-related driving (it almost never does)

- Choosing the cheapest available policy without checking whether the liability limits meet client contract requirements

Typical Cost Ranges by Coverage Level

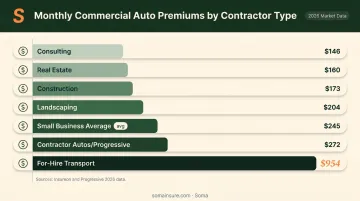

According to Insureon's commercial auto cost data updated March 2026, the average commercial auto premium is $245/month for small business customers, with annual costs ranging from under $375 to over $16,000.

Progressive's commercial data puts contractor autos at $272/month on average, while for-hire transport trucks average $954/month — a gap that reflects how dramatically vehicle use and cargo type affect premiums.

Here's how costs break down by contractor profile:

| Contractor Type | Approximate Monthly Average |

|---|---|

| Consulting businesses | $146/month |

| Real estate professionals | $160/month |

| Construction contractors | $173/month |

| Landscaping businesses | $204/month |

| Overall small business average | $245/month |

| Contractor autos (Progressive) | $272/month |

| For-hire transport trucks | $954/month |

Sources: Insureon (updated May 2026), Progressive Commercial (2024 data)

These figures reflect full commercial auto policies. They don't include tools and equipment in the vehicle (covered under inland marine insurance) or employee injuries (handled by workers' compensation). The three tiers below show what each coverage level actually buys you.

Liability-Only Coverage

This tier covers bodily injury and property damage liability at or near state minimums — the floor, not the ceiling.

It fits contractors who use a personal vehicle only occasionally for work, lower-risk professionals like consultants and freelancers, or those adding Hired and Non-Owned Auto (HNOA) to an existing general liability or BOP policy.

Liability + Physical Damage

This level adds collision and comprehensive coverage alongside liability above state minimums — protecting both your vehicle and third-party claims.

Good fit for contractors driving daily, those with financed or leased vehicles, and anyone in moderate-risk work where losing the vehicle would stall business operations.

Full Commercial Coverage with Higher Limits

What's included: $1M+ combined single limit (CSL) liability, uninsured/underinsured motorist, hired and non-owned auto, and medical payments coverage.

Best for: High-mileage delivery and logistics contractors, construction and trade contractors whose client contracts require $1M+ limits, and any contractor whose vehicle is their primary business asset.

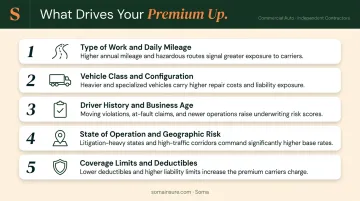

Key Factors That Affect the Cost of Independent Contractor Auto Insurance

Commercial auto premiums are underwritten on business-specific risk variables, not just personal driving history. A contractor's occupation, vehicle type, and operating geography all factor into the final rate — and those variables routinely push quotes well above what personal auto policies show.

Type of Work and Daily Vehicle Use

This is the single biggest premium driver. A delivery driver covering 200+ miles per day represents fundamentally different exposure than a consultant driving to client meetings twice a week. Insurers price for how frequently the vehicle is on the road and what it's doing when it's there.

High-frequency business use categories that typically attract higher premiums:

- Courier and delivery work

- Construction site visits and material transport

- Landscaping and field service routes

- Any role where the vehicle is essentially a mobile office used five days a week

Vehicle Class and Configuration

Moving from a passenger sedan to a cargo van to a Class 3 pickup raises premiums at each step. Vehicles with permanent upfitting (ladder racks, service bodies, built-in tool storage) may require additional underwriting disclosure and affect the vehicle's stated insured value.

The FMCSA designates vehicles with a gross vehicle weight rating (GVWR) of 10,001 pounds or more as commercial motor vehicles, which triggers different regulatory and insurance requirements.

Driver History and Business Operating Age

Both the individual motor vehicle record (MVR) and the business's operating history factor into underwriting. Contractors with clean records pay less — violations, at-fault accidents, and DUIs increase premiums materially.

New businesses (typically under 2–3 years) often face a new venture surcharge because insurers have no loss history to underwrite against. Working with a broker like Soma, which specializes in placing coverage for operations that standard markets surcharge or decline, can help newer contractors access competitive terms they wouldn't find on their own.

State of Operation and Geographic Risk

State minimum liability requirements vary widely, and high-litigation states — California, Florida, and New York — carry materially higher base premiums. Urban operating environments increase both the frequency and severity of potential losses compared to rural routes.

Coverage Limits and Deductible Choices

Higher liability limits increase premiums, but state minimums are often well below what client contracts require. The trade-off on deductibles runs the other direction: higher deductibles reduce monthly premiums but mean more out-of-pocket cost when a claim occurs.

What Coverage Do Independent Contractors Actually Need?

Coverage needs start with one question: is this a dedicated business vehicle, or a personal vehicle occasionally used for work? The answer determines whether you need a standalone commercial auto policy or whether HNOA added to an existing business policy is sufficient.

Commercial Auto Liability (Bodily Injury and Property Damage)

This is the foundational coverage. It pays for injuries and property damage caused to others when the contractor is at fault while driving for business. State minimums rarely match what client contracts demand — $1M CSL is the standard requirement in many construction, logistics, and professional services contracts.

Physical Damage: Collision and Comprehensive

Collision covers at-fault accidents. Comprehensive covers theft, vandalism, fire, and weather events. Lenders and lessors typically require both.

Contractors whose vehicle directly generates income — a plumber's van, a delivery contractor's cargo vehicle — should carry both regardless of lender requirements. Losing the vehicle means losing revenue.

Hired and Non-Owned Auto (HNOA) Insurance

HNOA covers the contractor's liability when using a personal or rented vehicle for business — it does not cover physical damage to the contractor's own vehicle. It's the right fit for occasional business use of a personal car. It is not sufficient when a personal vehicle functions as the contractor's primary work vehicle.

What Commercial Auto Does NOT Cover

Be clear on the gaps:

- Tools and equipment stored in or transported by the vehicle — covered under tools and equipment insurance or inland marine

- Employee injuries in a vehicle accident — handled by workers' compensation

- Cargo being transported — requires a separate cargo or inland marine policy

Soma structures HNOA as a standalone placement or as part of a broader general liability or BOP policy, depending on the contractor's risk profile. Its construction insurance program bundles tools and equipment coverage with contractor liability — a useful combination for tradespeople who carry significant tool inventory.

Personal Auto vs. Commercial Auto: The Coverage Gap

Most personal auto policies contain a formal business-use exclusion. According to the NAIC, personal auto insurance usually does not cover vehicles used for work purposes. Insureon states even more directly that personal auto insurers will likely reject a claim if an accident happens while driving for business.

That exclusion applies regardless of how infrequently the vehicle is used for work — and most contractors don't find out until after they've filed a claim.

Take a straightforward example: a contractor making a delivery gets into an at-fault accident. Without commercial coverage, they're personally responsible for:

- Vehicle repair costs

- Third-party medical bills

- Property damage liability

- Legal defense fees

Those costs can easily reach six figures on a serious accident.

The right policy depends on how often — and how heavily — the vehicle is used for business:

| Situation | Right Coverage |

|---|---|

| Occasional client meetings in personal vehicle | HNOA added to GL or BOP |

| Weekly site visits, low mileage | HNOA or light commercial auto |

| Daily business driving, primary work vehicle | Standalone commercial auto policy |

| Vehicle carries cargo, equipment, or employees | Standalone commercial auto policy |

How to Get the Right Coverage Without Overpaying

Before requesting quotes, organize the following information:

- How many days and miles per week the vehicle is used for business

- What liability limits client contracts or state laws require

- Whether the vehicle is owned, leased, or financed

- Whether additional drivers or vehicles may need to be added

Having this ready speeds up the quoting process — and makes it easier to compare offers on equal footing.

Compare Across Carriers

Rates for the same risk profile can vary by 30–50% across carriers. Working with a commercial insurance brokerage like Soma — which works with hundreds of carrier partners across complex and hard-to-insure risks — brings competitive options to one place, so contractors don't have to contact multiple insurers separately. Soma partners with carriers including Progressive, Nationwide, Liberty Mutual, Chubb, and Markel, among others.

Cost Management Strategies

- BOP bundling: Combining commercial auto with general liability in a Business Owner's Policy typically yields multi-policy discounts of 5–15%

- Clean driving record: Your MVR is one of the strongest factors carriers use to set premiums — a clean record pays off year over year

- Consider telematics: Progressive offers usage-based programs for commercial auto that can yield discounts for contractors who demonstrate safe driving behavior

- Review annually: Business scale and vehicle use patterns change — a policy priced for last year's operations may be costing you more than it should

Two Mistakes to Avoid

- Choosing minimum limits to minimize premium — state minimums are typically far below what an at-fault accident with serious injuries would cost, and well below what most client contracts require

- Failing to disclose full business use when applying — misrepresentation at application can result in claim denials or policy cancellations, which is worse than the premium you were trying to avoid

Frequently Asked Questions

How much does commercial auto insurance cost for independent contractors?

According to Insureon's 2026 data, the average is $245/month for small businesses, with Progressive pegging contractor autos specifically at $272/month. Delivery and high-mileage contractors pay more; consultants and occasional-use contractors typically pay less.

Does personal auto insurance cover me while I'm working as an independent contractor?

No. Most personal auto policies formally exclude business use. If your insurer determines the vehicle was being used for work at the time of an accident, the claim can be denied. Review your policy's business-use exclusions and consider commercial auto or HNOA coverage.

What is hired and non-owned auto insurance, and do independent contractors need it?

HNOA covers your liability when using a personal or rented vehicle for business — it does not cover physical damage to your own vehicle. It works well for contractors who use a personal car occasionally for work. If your vehicle is used daily for business, a full commercial auto policy is the right structure.

Can independent contractors deduct commercial auto insurance premiums as a business expense?

Yes. IRS Publication 463 allows a full deduction when a vehicle is used exclusively for business, including insurance costs. For mixed personal/business use, only the business-use portion qualifies — consult a tax professional for your specific situation.

What liability limits do independent contractors typically need?

State minimums are almost never sufficient for business use. Many client contracts require a minimum of $1M combined single limit (CSL), and contractors in high-risk trades or logistics should carry at least that to avoid personal exposure on major claims.

Do I need commercial auto insurance if I only use my personal vehicle occasionally for work?

For truly infrequent, low-risk use, HNOA added to a general liability or BOP policy may be sufficient. If your vehicle is regularly used for business, even without daily use, a full commercial auto policy is the right call given personal policies' business-use exclusions.