Introduction

Picture this: one of your work trucks runs a red light on the way to a job site. Two vehicles are hit, three people injured, and a nearby storefront takes significant damage. Total damages reach $800,000 — but your commercial auto policy only carries $300,000 in coverage.

That gap is yours to fill — out of pocket, from your business accounts, equipment, or personal assets.

This scenario plays out more often than contractors expect. Commercial auto liability claim severity rose 78% between 2014 and 2023, far outpacing general inflation at 29% over the same period. Choosing limits that felt adequate two years ago may leave you dangerously exposed today.

Three standards shape what limits contractors actually need: state law, federal FMCSA regulation, and private construction contracts. This guide walks through all three — plus the operational factors that determine your real exposure — so you leave with a number you can defend to a client, a regulator, or a judge.

TL;DR

- Commercial auto liability limits cap what your insurer pays per accident; anything beyond that limit is your financial responsibility.

- State minimums are legal floors, not project-ready contractor limits — some property damage thresholds are as low as $10,000.

- Most GCs and project owners require a $1,000,000 CSL before a subcontractor can start work or get paid.

- The right limits depend on your vehicle types, fleet size, driving geography, and total business assets at risk.

- A commercial umbrella policy is typically the most cost-efficient way to reach higher total limits beyond your base auto coverage.

What Are Commercial Auto Insurance Limits?

Commercial auto insurance limits define the maximum dollar amount your insurer will pay for a covered accident involving a business vehicle. Once that ceiling is reached, every dollar of remaining damages becomes the business owner's problem — whether that means legal judgments, settlements, or repair costs paid directly.

Split Limits vs. Combined Single Limit (CSL)

Most contractors will encounter two limit structures:

Split limits divide coverage into three separate caps:

- Bodily injury per person

- Bodily injury per accident (all injured parties combined)

- Property damage

A 100/300/100 policy means $100,000 per injured person, $300,000 total for all bodily injury per accident, and $100,000 for property damage. Hit those internal caps in any category, and the overage falls on you — even if the other pools still have money left.

A Combined Single Limit (CSL) replaces those internal boundaries with one unified pool covering all bodily injury and property damage from a single accident — allocated wherever claims demand it. If a $1,000,000 CSL policy covers an accident with $700,000 in injury claims and $250,000 in property damage, it handles both without internal caps creating gaps.

The Insurance Information Institute identifies $500,000 and $1,000,000 as common commercial auto CSLs, with many insurers recommending $1,000,000 as the baseline for business coverage.

Why Limit Structure Matters for Contractors

Split-limit policies create real gaps in multi-party accidents. A construction crew vehicle that hits two workers and damages an adjacent property might exhaust the per-person bodily injury cap while property damage claims are still outstanding — or vice versa. CSL eliminates those internal boundaries entirely — which is why most commercial construction contracts require CSL rather than split-limit formats. If your contracts specify minimum coverage, they almost certainly mean CSL.

The Three Standards That Govern Contractor Limits

Commercial auto limits for contractors answer to three distinct authorities. A policy that satisfies one can still fail the others. The highest applicable standard always controls.

State Statutory Minimums

Every state requires minimum liability coverage to register a vehicle and operate on public roads. These floors vary significantly:

| State | Minimum Liability Structure |

|---|---|

| Florida | $10,000 PIP + $10,000 property damage |

| Arizona | $25,000/$50,000/$15,000 |

| California | $30,000/$60,000/$15,000 |

| New York | $25,000/$50,000 BI + $10,000 property damage |

| Maine | $50,000/$100,000/$25,000 or $125,000 CSL |

| Alaska | $50,000/$100,000/$25,000 |

State minimums were designed around personal sedan accidents, not commercial collisions involving heavy trucks, equipment trailers, or vehicles operating near job sites with multiple bystanders.

A Florida contractor meeting the state's $10,000 property damage minimum would exhaust that limit in a minor fender bender with a newer vehicle. It's a registration requirement, not meaningful financial protection.

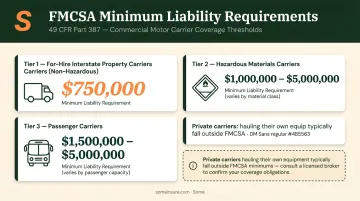

Federal FMCSA Requirements

FMCSA rules apply to a narrower population than many contractors assume. The key thresholds under 49 CFR Part 387:

- $750,000 — for-hire interstate property carriers with GVWR of 10,001 lbs or more, non-hazardous cargo

- $1,000,000–$5,000,000 — hazardous materials carriers, depending on material classification

- $1,500,000–$5,000,000 — passenger carriers

A contractor hauling their own tools and equipment across state lines is generally a private carrier, not a for-hire motor carrier. Private carriers transporting their own cargo don't require FMCSA operating authority. That said, a truck and trailer combination exceeding 10,001 lbs GVWR operating interstate does trigger the need for a USDOT number — a separate registration requirement distinct from minimum insurance amounts.

If your operations involve regulated hazardous materials or crew transport that meets FMCSA passenger thresholds, federal minimums become directly relevant and substantially higher.

Contractual Requirements from GCs and Project Owners

Private construction contracts impose the strictest and most practically relevant standard for most working contractors. General contractors and project owners require a Certificate of Insurance (COI) before allowing subcontractors to mobilize or receive payment.

The widely recognized industry benchmark is $1,000,000 CSL for automobile liability covering owned, hired, and non-owned autos. Real-world examples confirm this:

- Colorado DOT's standard insurance requirements specify $1,000,000 each accident CSL for all auto categories

- AIA A101 Exhibit A public project examples reference $2,000,000 per accident for contractor auto liability

Failing to carry the required limits constitutes a contract breach that can delay mobilization, hold payment, or disqualify a bid entirely. The COI must reflect the required limits, and GCs commonly require additional insured status on the auto policy as well.

When contract requirements change or a new project demands higher limits, having a broker who can issue updated COIs quickly through an established carrier network — like Soma — removes a common mobilization bottleneck before it becomes a work stoppage.

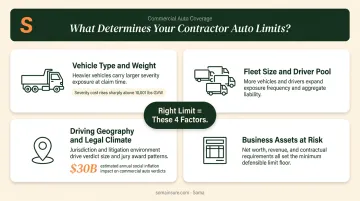

Key Factors That Determine the Right Limits for Your Business

The $1,000,000 CSL is a floor, not a ceiling. Your actual exposure depends on what you're driving, how often, where, and what you stand to lose if a claim exceeds your policy.

Vehicle Type and Fleet Composition

Heavier vehicles cause more damage. FMCSA estimated the comprehensive cost of a fatal large-truck crash at $14,578,771 in 2022, with injury crashes averaging $383,168 and non-injury CMV crashes at $46,612.

Even a non-injury commercial vehicle accident can exceed state property damage minimums of $10,000–$15,000. Work trucks with permanent upfits — tool shelving, compressors, lift gates — dump trucks, and vehicles towing heavy equipment represent substantially higher severity potential than a standard passenger vehicle.

If your truck causes a serious injury, a $1M limit may cover less than half the claim. Let severity drive your limit selection, not just your premium budget.

Fleet Size and Driver Pool

More vehicles plus more drivers equals more exposure opportunities. Underwriters review motor vehicle records (MVRs) for all listed drivers, and larger or less-experienced driver pools typically factor into both pricing and appropriate limit recommendations.

One critical detail: unlisted drivers who cause accidents can trigger claim denials. Every employee who regularly drives a company vehicle should be on the policy. The administrative cost of keeping that list current is far lower than a denied claim.

Driving Geography and Legal Climate

Geography affects exposure in two ways:

- Frequency: Contractors operating in dense urban areas, navigating active road construction zones, or traveling multi-state routes face higher accident probability than those making short rural drives.

- Legal climate: Some jurisdictions are far more litigious than others. Social inflation — driven by plaintiff-friendly venues and nuclear verdicts — contributed $30 billion to commercial auto claim costs from 2012 to 2021, according to the Insurance Information Institute. A $1,000,000 limit that feels adequate in one state may fall short in a plaintiff-favorable jurisdiction where jury awards routinely exceed policy limits.

Asset Protection and Financial Exposure

Those verdict risks land directly on your balance sheet. Your limits should reflect what you stand to lose — and who you are as a business:

- Sole proprietors: Personal assets are exposed when a judgment exceeds business coverage

- Growing contractors: A GC managing a $5M project pipeline carries far more to protect than a two-person crew

- Fleet operators: Each additional vehicle multiplies severity potential, not just frequency

If a $2,000,000 claim landed tomorrow, what would the gap cost your business?

Coverage Components Beyond Liability Limits

Liability limits get the most attention, but three other coverage components matter equally for contractor operations.

Physical Damage: Collision and Comprehensive

Physical damage coverage protects your own vehicles — collision handles accident damage, comprehensive covers theft, vandalism, weather, and other non-collision perils. Soma's commercial auto placements bundle both liability and physical damage, so contractors cover the full vehicle exposure under one policy.

Three situations where physical damage coverage is non-negotiable:

- Financed or leased vehicles — lenders require it as a loan condition

- High-value work trucks — replacement costs routinely exceed $80,000–$100,000 with upfits

- Custom-equipped fleets — specialized tools and bodies raise the stakes significantly

Deductible selection directly affects premium. Higher deductibles reduce cost but increase out-of-pocket exposure per incident, so set them at a level the business can actually absorb.

Hired and Non-Owned Auto (HNOA) Coverage

HNOA fills a gap that catches many contractors off-guard. If an employee drives their personal vehicle to a job site, picks up materials in their own truck, or rents a vehicle for a project — and causes an accident — the business can be held liable. Personal auto policies generally exclude work-related use, leaving the employer exposed.

HNOA coverage extends the business's liability protection to those scenarios. Limits should mirror the base commercial auto policy, and the coverage can be added as an endorsement to an existing commercial auto policy or included within a broader commercial auto program.

Umbrella and Excess Liability

A commercial umbrella policy sits above the base commercial auto policy and activates once the underlying limit is exhausted. It's typically the most cost-efficient path to higher total coverage — often more economical than simply raising the base auto limit to $2,000,000 or beyond.

Umbrella policies cover commercial auto, general liability, and employer's liability simultaneously — a single policy lifting multiple lines at once. For contractors bidding public projects or larger commercial work, umbrella coverage is frequently a contract requirement. The underlying commercial auto limits must be in place and adequate before the umbrella can attach properly.

How Soma Can Help

Soma is an independent commercial insurance brokerage with access to hundreds of carrier partners — including Chubb, Liberty Mutual, Nationwide, and Markel — placing coverage for contractors with mixed fleets, upfitted vehicles, and operations that standard markets price poorly.

Soma's risk management team helps contractors build the right coverage structure from the ground up. That includes:

- Setting appropriate CSL levels and umbrella layers

- Adding physical damage and HNOA where needed

- Reviewing GC and project owner contract requirements before mobilization

- Issuing updated COIs quickly when vehicles, drivers, or contracts change

For contractors who've held up a job start waiting on a broker to return a call or reissue a certificate, that turnaround speed matters.

Frequently Asked Questions

What do commercial auto insurance liability limits like 250/500/100 mean?

This is a split-limit format: $250,000 per injured person, $500,000 total bodily injury per accident, and $100,000 for property damage. Once any cap is reached, the contractor pays the remainder out of pocket, even if other pools still have coverage available.

Are 50/100/50 commercial auto limits sufficient for contractors?

While 50/100/50 may satisfy DMV registration minimums in some states, it falls well below the $1,000,000 CSL required by most construction contracts. A serious multi-injury accident can exhaust those limits quickly, leaving significant personal and business financial exposure.

What is a Combined Single Limit (CSL) and why do contractors need it?

A CSL provides one unified coverage pool for all bodily injury and property damage in a single accident. Most GCs and project owners specifically require a $1,000,000 CSL on contractor COIs — split-limit policies often don't satisfy those contractual requirements even when the numbers look comparable.

Do contractors need commercial auto insurance if employees drive their own vehicles to job sites?

Personal auto policies typically exclude work-related use, meaning the business can be held liable for an accident with no coverage in place. Hired and Non-Owned Auto (HNOA) coverage protects the business when employees use personal or rented vehicles for company business.

Is a $1,000,000 commercial auto liability limit required by law?

No — $1,000,000 CSL is a contractual standard set by GCs and project owners, not a state legal mandate. State minimums are much lower. However, failing to carry the required contractual limit can breach a subcontract, delay mobilization, or disqualify a bid entirely.

Does a commercial umbrella policy count toward commercial auto limit requirements?

Yes, in most cases. A commercial umbrella extends total limits above the base commercial auto policy and is commonly counted toward contract liability requirements. The underlying commercial auto policy must carry adequate limits first; the umbrella cannot substitute for an insufficient base policy.