This scenario plays out constantly for business owners across construction, security, healthcare, and dozens of other industries. The COI is one of the most frequently requested business documents in the U.S., yet many owners only learn what it is when a deadline is already pressing.

This guide covers everything you need to know: what a COI is, when you'll need one, what it contains, the difference between a certificate holder and an additional insured, and how to get one fast.

TL;DR

- A Certificate of Liability Insurance (COI) is a one-page document proving your business has active liability coverage.

- It's issued by your insurer or broker at no additional cost beyond your existing policy premium.

- You'll typically need one for client contracts, commercial leases, license applications, and events.

- A COI is not your insurance policy — the recipient gains no coverage rights from receiving it.

- With an active policy in place, most standard COIs are issued the same day, often instantly.

What Is a Certificate of Liability Insurance?

A COI is an official summary of your business's liability insurance — issued on the ACORD 25 form — confirming coverage is active. It's evidence of coverage, not the policy itself.

ACORD (Association for Cooperative Operations Research and Development) is a non-profit organization that created standardized insurance forms. The ACORD 25 is the industry's accepted liability certificate — recognized by state procurement offices, general contractors, landlords, and licensing boards across the US.

A COI does NOT:

- The full insurance policy

- A document that grants legal rights to whoever receives it

- Something that can be altered or fabricated — doing so is a criminal offense

Louisiana's Department of Insurance classifies knowingly producing a false COI as a criminal offense carrying fines up to $5,000 or imprisonment up to 5 years. Delaware law similarly prohibits certificates with false or misleading information.

COI vs. Declaration Page — What's the Difference?

Both documents summarize your policy, but they serve different audiences:

| Document | Who It's For | Purpose |

|---|---|---|

| Declaration (dec) page | The policyholder | Internal reference; generated automatically with the policy |

| Certificate of Liability Insurance | Third parties | Proof of coverage shared with clients, landlords, licensing boards |

The dec page stays with you. The COI is what you share when someone else needs to verify your coverage.

When Do You Need a Certificate of Liability Insurance?

The short answer: more often than most business owners expect.

Client Contracts

When working with larger companies or enterprise clients, they typically require a COI before any work begins. Their concern is straightforward: if your work causes property damage or bodily injury, they want your insurance to respond, not theirs. According to Travelers, contractual risk transfer programs rely on COIs and additional insured endorsements to confirm that vendors carry adequate coverage.

Commercial Leases

Most landlords and property managers require tenants to carry general liability insurance before signing a lease. If an injury occurs on the premises — a client slips, a fire spreads to an adjacent unit — the landlord wants your coverage to respond first. Hiscox confirms that most commercial leases require tenants to carry liability insurance to protect against property damage and bodily injury claims.

Professional Licensing

Many regulated industries require proof of insurance to obtain or renew a license. Examples from state requirements include:

- Washington contractors — must provide a certificate of general liability insurance to register with the state's L&I board

- Minnesota residential contractors — must carry at least $100,000 per occurrence / $300,000 aggregate and submit an ACORD certificate at licensing

- Texas electrical contractors — minimum $300,000 per occurrence / $600,000 aggregate required with each license application

- Texas master plumbers — must maintain at least $300,000 commercial general liability and submit a signed COI

- New York security agencies — minimum $100,000 per occurrence / $300,000 aggregate, with a signed COI submitted at application

Requirements vary significantly by state and profession. Always verify the specific limits and forms each licensing authority requires before applying.

Events, Venues, and High-Risk Industries

Event organizers routinely require COIs from photographers, caterers, AV vendors, and other service providers before allowing them on-site. In construction, project owners may require subcontractors to carry $1 million or more per occurrence and name the general contractor as an additional insured.

If your business operates in any of these industries, expect stricter minimums and more detailed endorsement requirements:

- Construction and general contracting

- Trucking and commercial transportation

- Security guard agencies

- Manufacturing and industrial operations

What Information Does a Certificate of Liability Insurance Include?

The ACORD 25 form organizes coverage information into clear, standardized fields. Here's what you'll find:

Identifying information:

- Named insured (your business name and address)

- Producer/insurer name and contact information

- Policy number

Coverage types in force — the form includes separate sections for:

- Commercial General Liability (CGL)

- Commercial Auto

- Workers' Compensation / Employers' Liability

- Umbrella / Excess Liability

Key limits shown for general liability:

| Limit Type | What It Means |

|---|---|

| Per-occurrence limit | Maximum the insurer pays for all claims from a single incident |

| General aggregate | Total maximum paid across all covered losses during the policy period |

| Products/completed operations aggregate | Separate aggregate applying to claims from completed work |

Policy effective and expiration dates — these confirm whether coverage is currently active. Certificate holders often track these dates and will request a renewed COI as expiration approaches.

Additional fields:

- Certificate Holder box — identifies who the COI is being sent to

- Description of Operations — can specify the project, contract, or location the certificate relates to

- Additional Insured / Waiver of Subrogation checkboxes — these determine whether the certificate holder is covered under your policy and whether your insurer can pursue recovery costs against them

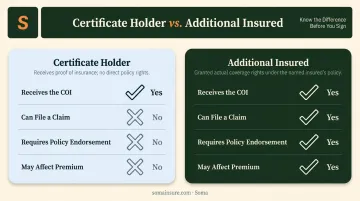

Certificate Holder vs. Additional Insured: Key Differences

This distinction trips up a lot of business owners, and getting it wrong can create real problems.

Certificate holder — the party who receives the COI as proof that coverage exists. Being listed here means nothing more than that: they receive the document and are entitled to notification if the policy is cancelled. They cannot file a claim under your policy. As the ACORD 25 form itself states, the certificate "is issued as a matter of information only and confers no rights upon the certificate holder."

Additional insured — a party added directly to your insurance policy, typically through an endorsement, giving them the right to make claims under that policy if a covered incident occurs. That's a different level of protection entirely.

Here's a quick comparison:

| Certificate Holder | Additional Insured | |

|---|---|---|

| Receives the COI | Yes | Yes (typically) |

| Can file a claim | No | Yes |

| Requires a policy endorsement | No | Yes |

| May affect your premium | No | Possibly |

Why This Matters in Practice

Clients in construction, real estate development, and event management routinely require vendors to name them as additional insureds — not just certificate holders. The Nonprofit Risk Management Center confirms that a certificate without an additional insured endorsement does not provide additional insured status, regardless of what the COI says.

Before signing any contract, confirm whether the other party wants to be a certificate holder, an additional insured, or both — then make sure your policy reflects it.

How to Get a Certificate of Liability Insurance

The process is straightforward — but it starts with having a policy.

Step 1: Get an active policy

No policy, no COI. If your business doesn't yet have general liability insurance, that's the first step. For most straightforward businesses, standard carriers can issue coverage quickly.

For industries that standard markets routinely decline — construction, security agencies, trucking, manufacturing, hospitality — a specialized broker like Soma can help place coverage that other brokers won't touch.

Step 2: Request the COI

Once your policy is active, contact your broker or insurer to request the certificate. According to The Hartford, a COI request can take less than five minutes online and is delivered instantly in most cases. Custom certificates — those requiring additional insured endorsements or specific project descriptions — may take longer depending on the carrier.

Step 3: Submit and monitor expiration

Forward the COI to the requesting party and track your policy's expiration date. For ongoing contracts or multi-year leases, set a calendar reminder at least 30 days before expiration. An expired COI can trigger a contract violation or work stoppage — especially on construction projects where continuous coverage is a contractual requirement. Staying ahead of renewals is just as important as getting the certificate in the first place.

How Much Does a Certificate of Liability Insurance Cost?

The COI document itself is free. Requesting one from your insurer or broker costs nothing. It's simply a summary of your existing policy.

The real cost is the underlying general liability policy. Premium varies based on:

- Industry type and risk exposure

- Coverage limits selected

- Business size (revenue, employees)

- Location

- Claims history

- Years in business

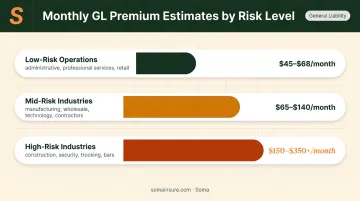

Current market estimates put small business general liability premiums at roughly $45–$68 per month for lower-risk operations, based on figures from Insureon and The Hartford. Higher-risk industries — construction, security, bars, trucking — typically pay more, and limits requirements from clients or licensing boards may push those numbers higher.

If your contracts or licenses specify minimum limits, those requirements dictate what you actually need — not just what's cheapest. A broker who works regularly with your industry (construction, security, trucking, hospitality) will know those thresholds and can match your policy to them from the start, avoiding gaps that show up when a certificate gets rejected.

Frequently Asked Questions

Do I need a certificate of liability insurance if I have an LLC?

An LLC protects your personal assets but does not replace business insurance. Clients, landlords, and licensing boards require a COI regardless of your legal structure — and an LLC without a general liability policy has no COI to provide.

What is the difference between a certificate holder and an additional insured?

A certificate holder receives the COI as proof of coverage but cannot file claims under your policy. An additional insured is added to the actual policy via endorsement and has the right to make claims under it. That distinction carries far more weight than simply being named on a certificate.

Is a certificate of liability insurance the same as a declaration page?

Both documents summarize policy details, but the dec page is your internal reference document. The COI is designed to be shared with third parties — clients, landlords, licensing agencies — as formal proof of coverage.

How long does it take to get a certificate of liability insurance?

With an active policy, a standard COI is typically issued the same day — often instantly through an online portal. Certificates requiring endorsements or custom language may take one to two additional business days depending on the carrier.

What happens when my certificate of liability insurance expires?

An expired COI signals that the underlying policy has lapsed or not yet been renewed. Businesses under active contracts should renew before expiration. Waiting until after risks contract violations, work stoppages, or loss of a professional license.

Can a certificate of liability insurance be faked or altered?

Altering or fabricating a COI is insurance fraud and carries serious criminal penalties, including fines and imprisonment. Any party receiving a COI can verify its authenticity directly with the issuing insurer.