Introduction

A freight broker sends over their standard carrier packet. Buried in the insurance requirements section is a line asking the trucking company to add the broker as an "additional insured" on their Motor Truck Cargo policy. It looks like any other routine insurance request — the kind carriers process dozens of times a year on their CGL or commercial auto policies.

The problem is that MTC policies don't work like those policies. Agreeing to this request without understanding the mechanics can void the very coverage it was meant to create.

This post covers:

- What Motor Truck Cargo insurance actually is and how it's structured

- Why additional insured endorsements create a problem unique to this policy type

- Who is making these requests and what they're trying to protect

- What actually works instead of an additional insured endorsement

TL;DR

- Owned property exclusion risk: MTC policies cover cargo belonging to others — naming the cargo owner as an insured can void their coverage

- Freight brokers: Not carriers under federal law, so additional insured status on a carrier's MTC policy provides no real protection

- Certificate holder status satisfies most contractual verification needs without altering coverage

- Loss payee designation is the right tool for shippers with a direct financial interest in cargo

- Contingent cargo insurance is the correct solution for freight brokers, purchased on their own account rather than added to the carrier's policy

What Motor Truck Cargo Insurance Is Designed to Cover

Motor Truck Cargo (MTC) insurance is an inland marine form covering loss of property in the course of transit. OOIDA describes it specifically as insurance against "loss from legal liability for damage to goods or merchandise" — meaning it protects the carrier, not the cargo owner directly.

The Great American Motor Truck Cargo Coverage Form (CM 76 77) defines covered property as "property of others that you have accepted for transportation as a motor carrier under your tariff and bill of lading or other written contract." Coverage is triggered by the insured's legal liability as a motor carrier — not by the cargo owner's financial interest in the goods. That distinction shapes everything about how MTC policies are written and priced.

What MTC Typically Covers

Standard perils across most MTC forms include:

- Fire and explosion

- Collision and overturn

- Theft

- Water damage

- Loading and unloading accidents

Common add-ons include reefer breakdown (essential for temperature-sensitive freight), debris removal, and earned freight. Coverage applies while cargo is in transit, during loading and unloading, and in many forms extends to scheduled premises for short-term storage under 31 days when no storage charge is made.

The Ownership Architecture

The "property of others" framing isn't boilerplate. It's the structural foundation of how MTC policies are priced, underwritten, and worded. The insurer's risk calculation is based on one assumption: the carrier is responsible for someone else's property. When a shipper or broker demands to be added as an additional insured, that assumption starts to fracture — and coverage disputes follow.

How Adding Additional Insureds to MTC Policies Backfires

This is where the routine-looking request becomes a real problem.

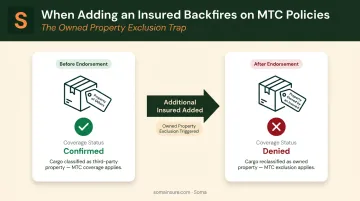

The Owned Property Exclusion

MTC policies almost universally exclude property owned by an insured under the policy. The NHF-501 2023 MTC form includes this limitation explicitly.

When a shipper is added as an additional insured, their cargo — which was previously "property of others" and therefore covered — legally becomes property owned by an insured. The exclusion triggers. Coverage for those goods disappears.

As MCIEF's industry paper on the topic puts it, the additional insured designation is a "sugar pill" — it looks like protection but may actually void the coverage the shipper was trying to secure. Overdrive has similarly reported that cargo policies almost always exclude property owned by an insured, meaning the endorsement can achieve the exact opposite of its intended purpose.

Why It Doesn't Work for Freight Brokers Either

Brokers face a different problem. Under 49 USC 13102, a broker is legally defined as someone who arranges transportation — distinct from a motor carrier who actually performs it. The Carmack Amendment (49 USC 14706) assigns liability to carriers — not to brokers acting as arrangers.

A broker doesn't hold the same legal liability as a carrier for goods in transit. Being named as an additional insured on the carrier's MTC policy doesn't grant meaningful protection — the insurable interest isn't structured the same way.

In practical terms, brokers seeking cargo coverage protection need their own contingent cargo policy, not an endorsement on the carrier's form. The additional insured route addresses the wrong legal relationship entirely.

The Underwriting Problem

Insurers price MTC policies based on the carrier's operations and loss history. Adding an additional insured expands the scope of who the insurer might have to defend or indemnify — with no corresponding underwriting adjustment. In practice:

- Some carriers refuse the endorsement outright on MTC policies

- Others issue a restrictive form that provides far less than the requesting party expects

- Some charge a meaningful additional premium and still limit the endorsement's scope

The Claim-Time Consequence

When a loss occurs and the insurer reviews an additional insured endorsement on an MTC policy, the path to denial is short: the claimant is an insured, the cargo belonged to an insured, and the owned property exclusion applies.

The shipper or broker gets nothing from the carrier's policy — and may have no time to pursue alternatives.

That outcome also lands on the trucking company. They agreed contractually to provide protection that the policy cannot actually deliver — which exposes them to breach of contract claims on top of the original cargo loss.

Who Asks for Additional Insured Status — and Why

The request shows up from two different directions, for different reasons.

Shippers are typically trying to protect the financial value of their goods in transit. They're accustomed to being named as additional insureds on vendor and contractor CGL policies — where the mechanism works cleanly — and assume the same rules apply here. They don't. CGL policies don't contain a "property of others" coverage grant that creates this conflict.

Freight brokers are usually trying to manage downstream risk from shippers who hold them responsible when cargo is lost or damaged. Their instinct is to get coverage under the carrier's policy rather than buy their own. The right tool for brokers is contingent cargo insurance — a policy the broker purchases on their own account — not an endorsement on the carrier's MTC policy.

Additional insured requests are routine in commercial contracting — on CGL, commercial auto, and umbrella policies — so it's easy to assume the mechanism transfers cleanly across all lines. MTC is the clearest example of where it doesn't, and understanding why each party is asking is the first step toward steering them toward coverage that actually works.

Certificate Holder, Loss Payee, and Contingent Cargo: The Right Tools

There are three designations worth understanding clearly. Here's how they compare:

| Designation | Who It Protects | What It Provides | Right for MTC? |

|---|---|---|---|

| Certificate Holder | Broker or shipper needing proof of coverage | Evidence of policy existence, limits, dates, and cancellation notice | Yes — satisfies most verification needs |

| Loss Payee | Shipper with direct financial interest in cargo | Direct payment rights for covered losses without becoming an insured | Yes — avoids the owned property exclusion |

| Additional Insured | Any party needing insured status | Full insured rights under the policy | No — triggers owned property exclusion on MTC |

| Contingent Cargo | Freight broker | Broker's own policy that steps in when carrier MTC fails | Yes — correct broker solution |

Certificate Holder

As IIABA's certificate guidance explains, a certificate of insurance "is informational only, confers no rights, and does not amend, extend, or alter coverage." That's precisely what makes it the right tool for most contractual verification purposes — it documents that the carrier has MTC coverage without touching the policy's coverage structure.

For the majority of freight contracts requiring "proof of insurance," certificate holder status fully satisfies the business need.

Loss Payee

A loss payee is entitled to receive insurance proceeds for covered losses in which they have a financial interest — without becoming an insured under the policy. It doesn't trigger the owned property exclusion. The Great American MTC form explicitly permits the insurer to pay owners of covered property directly, making this designation structurally sound for shippers.

For shippers who need direct payment rights rather than proof of coverage, loss payee is the right designation to put in the contract.

Contingent Cargo Insurance

Roanoke Group describes contingent motor truck cargo insurance as coverage for transportation intermediaries when the carrier's insurance does not respond — whether due to exclusions, insufficient limits, or carrier insolvency. This is the broker's proper risk management tool.

Rather than attempting to attach to the carrier's MTC policy (where they have no legal standing as a carrier), brokers purchase their own contingent cargo policy. It responds when the carrier's coverage fails. That structure matches the broker's actual legal position as an intermediary — and holds up when a claim is contested.

How Trucking Companies Should Handle These Requests

When a freight contract lands in your inbox with an additional insured requirement on the MTC policy, here's how to work through it.

Step 1 — Read the contract language precisely. There is a material difference between a contract requiring a "certificate of insurance" and one explicitly demanding "additional insured" status. Many contracts use these terms loosely or interchangeably. Don't agree to an endorsement based on a vague reading — confirm what the contract actually requires.

Step 2 — Contact your insurance broker before responding. Before committing to anything in writing, call your broker. Your specific MTC form may prohibit the endorsement, issue it in a restricted form, or require additional premium. At Soma, the Risk Management Team reviews trucking clients' coverage across carrier partners including Progressive, Chubb, Kemper, and Ascend — the MTC policy language varies by carrier, and that variation matters when an endorsement request comes in.

Step 3 — Offer a certificate of insurance first. In most cases, providing a certificate with the requesting party listed as certificate holder satisfies the contract requirement. If the contract truly requires additional insured status, bring your broker into the conversation to evaluate whether a loss payee endorsement or a referral to contingent cargo coverage is the stronger, more enforceable solution.

Don't agree to a contractual obligation you may not be able to fulfill. A carrier that promises additional insured status, receives a policy that denies the claim under the owned property exclusion, and then faces a breach of contract dispute is in a worse position than one that pushed back on the request at contract time.

That's where carrier access and MTC policy fluency matter most — catching these conflicts at contract time, not at claim time.

Frequently Asked Questions

What is an additional insured on a cargo policy?

An additional insured on a cargo policy is a third party added by endorsement. Unlike on general liability policies, this designation can trigger the owned property exclusion on an MTC policy — eliminating coverage for that party's goods rather than protecting them.

What is Motor Truck Cargo insurance?

Motor Truck Cargo insurance is an inland marine policy covering a motor carrier's legal liability for loss or damage to freight belonging to others during transit. It protects the carrier, not the cargo owner directly, and is structurally distinct from both commercial auto liability and general liability insurance.

Can a freight broker be listed as an additional insured on a trucker's MTC policy?

The endorsement can be requested, but it provides no real protection. Brokers are legally distinct from carriers under 49 USC 13102 and don't hold a carrier's legal liability for freight in transit. Brokers needing protection should purchase their own contingent cargo coverage instead.

What is the owned property exclusion in Motor Truck Cargo insurance?

This exclusion prevents MTC policies from covering cargo owned by anyone designated as an insured under the policy. Adding a shipper as an additional insured can inadvertently convert their goods from "property of others" (covered) to "property owned by an insured" (excluded).

What is the difference between a loss payee and an additional insured on a cargo policy?

A loss payee receives claims payments for covered losses without becoming an insured — so the owned property exclusion is never triggered. This makes loss payee status a safer and more reliable designation for shippers with a financial interest in cargo, compared to additional insured status.

Will adding an additional insured to my MTC policy increase my premium?

Carrier responses vary: some refuse the endorsement on MTC policies outright, others charge additional premium, and some issue a restricted form with limited practical value. Confirm the terms with your broker before committing to this in a contract.