Introduction

A freight broker arranges a shipment. The carrier picks up the load, something goes wrong, and the cargo is damaged or stolen. The shipper files a claim — and the carrier's motor truck cargo insurer denies it. Maybe the policy lapsed. Maybe the commodity was excluded. Now the shipper is looking at the broker for recovery, and the broker is holding the bag on a six-figure loss they never expected to carry.

That gap is exactly what contingent motor truck cargo insurance is designed to fill.

This guide gives freight brokers, 3PLs, and logistics intermediaries a practical explanation of what this coverage is, who needs it, how claims get triggered, and how it compares to primary cargo insurance.

This guide gives freight brokers, 3PLs, and logistics intermediaries a practical explanation of what this coverage is, who needs it, how claims get triggered, and how it compares to primary cargo insurance.

According to CargoNet, cargo theft losses in the U.S. and Canada reached an estimated $725 million in 2025 — with average theft values climbing to $273,990 per incident.

TL;DR

- Contingent motor truck cargo insurance protects freight brokers and 3PLs when a carrier's cargo policy fails to pay

- It only activates after the carrier's insurer denies or cannot fulfill the claim — making it secondary by design

- Coverage typically includes legal defense costs, settlement payments, and third-party recovery efforts

- Does not replace the carrier's primary motor truck cargo policy

- Primary cargo insurance pays on a "first dollar" basis — no waiting on the carrier's policy to respond

What Is Contingent Motor Truck Cargo Insurance?

Contingent motor truck cargo insurance is a specialized liability policy for transportation intermediaries — freight brokers, property brokers, third-party logistics providers (3PLs), and domestic freight forwarders who arrange transportation but do not physically move freight themselves.

The word "contingent" describes exactly how the coverage works. It is secondary by design. The policy only activates when the underlying carrier's motor truck cargo (MTC) policy fails to respond — whether because the carrier's policy lapsed, excluded the commodity, denied the claim, or ran out of limits.

The Legal Boundary That Makes This Coverage Necessary

Under 49 U.S.C. § 14706 (the Carmack Amendment), carriers bear liability for actual loss or damage to cargo during interstate transit. Brokers, by contrast, are defined under 49 U.S.C. § 13102 as entities that arrange transportation — not motor carriers, not vehicle operators, not the party that physically moves the freight.

That legal separation doesn't make brokers immune from cargo claims. When a carrier's insurer denies a claim, shippers frequently name the freight broker in litigation as the most accessible recovery target. Contingent coverage is what protects brokers when that happens.

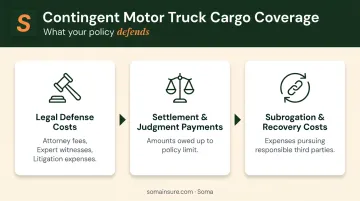

What the Policy Typically Covers

Three categories of costs fall under a standard contingent motor truck cargo policy:

- Legal defense costs — attorney fees, expert witness fees, and litigation expenses, even when the broker is ultimately not found liable

- Settlement and judgment payments — amounts owed if a court finds the broker partially or fully responsible, up to the policy limit

- Subrogation and recovery costs — expenses incurred pursuing responsible third parties after a covered loss

Contingent motor truck cargo coverage is not the same as cargo legal liability coverage. Cargo legal liability applies to carriers — or entities that present themselves as carriers — who issue bills of lading. Contingent coverage is strictly for intermediaries who arrange transportation without serving as the carrier of record.

Who Needs Contingent Motor Truck Cargo Insurance?

Freight Brokers

Freight brokers are the primary buyers of this coverage. No federal mandate requires brokers to carry it — FMCSA's financial responsibility requirement for property brokers is a $75,000 BMC-84 surety bond or BMC-85 trust, which is separate from cargo insurance entirely.

The practical driver is contractual. Many shipper agreements contain indemnity clauses that require the broker to assume responsibility for cargo loss if the carrier fails to pay. When those clauses are in play, contingent cargo coverage is not optional — it is what keeps those indemnity obligations from becoming out-of-pocket losses.

3PLs and Domestic Freight Forwarders

3PLs and freight forwarders arranging domestic ground transportation share the same core exposure as brokers — often with more moving parts. When a 3PL subcontracts a smaller regional carrier whose policy lapses mid-transit, the 3PL absorbs the financial fallout if contingent coverage is not in place.

Non-Asset-Based Logistics Companies

Non-asset-based intermediaries — those who own no trucks and rely entirely on contracted carriers — carry the highest dependency risk. If a contracted carrier's policy fails, a contingent policy is the only financial protection available. Without one, a single carrier default can become a direct, uninsured loss.

Who Does NOT Need This Coverage

- Motor truck carriers — they need primary MTC coverage, not contingent

- Shippers with their own cargo policy — they may need shipper's interest coverage instead

- Asset-based carriers acting as their own carrier of record — their primary policy already covers them directly

What Does Contingent Motor Truck Cargo Insurance Cover?

In-Transit Loss, Damage, and Theft

The policy covers cargo lost, stolen, or physically damaged while in transit under a contracted carrier — but only when the carrier's MTC policy has failed to respond. A common scenario: a freight broker contracts a carrier who subcontracts a smaller trucking firm. That sub-carrier's policy lapses. A theft occurs, the claim gets denied, and the broker's contingent coverage steps in to fill the gap.

CargoNet reported 2,646 confirmed cargo theft events in 2025, up 18% from 2024, with food and beverage topping the commodity theft list at 708 incidents. Electronics and copper also ranked high among organized crime targets in Q3 2025.

Legal Defense and Litigation Costs

Even when a broker is not ultimately found liable, defending a cargo lawsuit is expensive. A solid contingent cargo policy includes a duty to defend — meaning the insurer pays defense costs as they arise, not just at judgment. Without this language, you're covering attorney fees out of pocket during litigation even if you ultimately win. When evaluating any policy, confirm it includes duty-to-defend provisions — not just indemnity obligations.

Key question to ask your broker: Does the policy trigger defense coverage when a claim is filed, or only after liability is established?

Common Exclusions

Coverage has limits. Most contingent cargo policies exclude:

- Acts of war or terrorism

- Intentional damage or misconduct by the insured

- Losses caused by delay (not physical loss or damage)

- High-risk commodity classes — electronics, pharmaceuticals, tobacco, precious metals, liquor — which may require a broader form or primary policy

Modes of Transportation

While the name says "motor truck," coverage may extend to rail, intermodal, or short-sea shipping legs depending on the specific policy form. Check the policy form directly — or ask your broker to confirm covered modes before you bind — because assuming intermodal coverage without verifying it is a common and costly mistake.

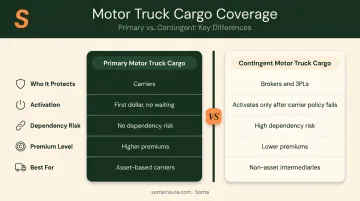

Contingent vs. Primary Motor Truck Cargo Insurance

The fundamental difference comes down to one question: does coverage depend on the carrier's policy responding first?

| Attribute | Primary Motor Truck Cargo | Contingent Motor Truck Cargo |

|---|---|---|

| Who it protects | The carrier transporting the freight | The broker or 3PL arranging transportation |

| When it activates | First dollar — pays directly on covered claims | Only after the carrier's policy fails to respond |

| Dependency risk | None — does not rely on another policy | High — follows the carrier's coverage quality |

| Cost | Higher premiums, broader protection | Lower premiums, narrower trigger |

| Best suited for | Asset-based motor carriers | Non-asset freight brokers, 3PLs, forwarders |

The contingent model carries a real dependency risk. If a carrier's insurer denies a claim because the commodity is excluded from their policy, the contingent policy may follow that same denial. The broker's coverage is only as good as the carrier's coverage gap allows it to be.

Carrier vetting directly affects whether contingent coverage can activate at all. Confirming that every contracted carrier holds active, adequate motor truck cargo insurance before a load moves is the only way to close that gap.

How Contingent Cargo Insurance Claims Work

The Claim Trigger Sequence

A contingent claim does not start with the broker — it starts with the carrier's policy failing. The typical sequence:

- Cargo is lost, stolen, or damaged during transit

- The shipper files a claim with the carrier's MTC insurer

- The carrier's insurer denies the claim, or the carrier has no valid coverage

- The shipper pursues the freight broker directly — through litigation or demand letter

- The broker submits a claim to their contingent cargo insurer

- The contingent insurer steps in to provide defense and/or indemnification

Documentation Requirements

To successfully trigger a contingent policy, the broker must demonstrate three things:

- A valid claim was submitted to the carrier's insurer

- The carrier's policy failed to respond (denial letter, lapse confirmation, or documented non-response)

- The broker is being held legally responsible for the loss

Documentation discipline starts well before any claim. Keep organized records of carrier contracts, certificates of insurance, bills of lading, and carrier vetting correspondence. A broker who cannot produce these records faces a harder path to recovery under their contingent policy.

The Financial Exposure Without Coverage

Those documentation gaps translate directly to financial risk. Average cargo theft values hit $273,990 per incident in 2025 — and high-value loads run far higher. A single denied carrier claim can wipe out a brokerage's operating capital.

In Tryg Insurance v. C.H. Robinson Worldwide (No. 17-3768), a court held a freight intermediary liable as a carrier based on contractual arrangements alone. No bad intent required. Without contingent coverage in place, that liability has nowhere to go but the broker's balance sheet.

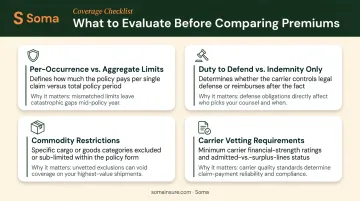

How to Get the Right Contingent Motor Truck Cargo Coverage

When evaluating policies, focus on these factors before comparing premiums:

- Per-occurrence vs. aggregate limits — Per-occurrence limits are generally more favorable for brokers handling diverse freight, since a single large claim does not exhaust annual coverage

- Duty to defend vs. indemnity only — A duty-to-defend provision pays legal costs as they arise; indemnity-only policies reimburse costs after the fact, which creates cash flow exposure

- Commodity restrictions — Confirm whether your freight mix includes any excluded categories (electronics, pharma, tobacco, precious metals) and whether a broader form or primary policy is necessary

- Carrier vetting requirements — Some policies require documented certificate collection and carrier insurance verification as a condition of coverage

Underwriters evaluating these submissions typically want to see:

- Annual freight volume and commodity mix

- Five years of loss history

- Sample broker-carrier agreements

- Shipper contracts that impose additional cargo liability obligations

Soma works with freight brokers and 3PLs to find the right market for contingent cargo submissions — placing coverage with carriers including Chubb, Markel, Liberty Mutual, and Nationwide across hundreds of markets through a single application.

Frequently Asked Questions

What is the difference between contingent and primary motor truck cargo insurance?

Primary cargo insurance pays claims directly on a "first dollar" basis without relying on the carrier's underlying policy, making it broader but more expensive. Contingent cargo insurance only activates after the carrier's own policy has failed to respond, making it cheaper but narrower in scope.

Who is required to carry contingent motor truck cargo insurance?

No federal mandate requires freight brokers to carry this coverage. FMCSA requires a $75,000 surety bond for property brokers, not cargo insurance. That said, many shipper contracts and freight awards make contingent coverage a practical commercial necessity.

What triggers a contingent cargo insurance claim?

A contingent claim is triggered when a carrier's motor truck cargo policy denies, lapses, or fails to adequately respond to a cargo loss or damage claim, and the freight broker or 3PL is subsequently drawn into legal or financial responsibility for that loss.

Does contingent cargo insurance cover cargo theft?

Most contingent cargo policies cover theft as a named peril. However, high-risk, theft-prone commodities — electronics, pharmaceuticals, tobacco, precious metals — may be excluded or require a broader form policy. Review your policy language carefully before binding.

Is contingent motor truck cargo insurance the same as contingent cargo liability insurance?

The terms are often used interchangeably, though some insurers distinguish them: contingent motor truck cargo typically covers domestic ground freight, while contingent cargo liability may extend to multi-modal or broader logistics operations. Confirm the scope with your insurer before binding.

How much does contingent motor truck cargo insurance cost?

Premiums depend on annual freight volume, commodity types, claims history, and policy limits. Market minimums generally range from $1,500 to $3,500, but these figures vary widely. Work with a specialist broker to get accurate pricing for your operation.