This is where Motor Truck Cargo Insurance and On-Hook Coverage come in — two distinct, specialized policies that fill critical gaps commercial auto simply doesn't address. The confusion between them is common, and the consequences of choosing wrong (or skipping one entirely) can mean absorbing five- or six-figure losses out of pocket.

This guide breaks down exactly what each coverage does, who needs it, and how to decide which one fits your operation.

TL;DR

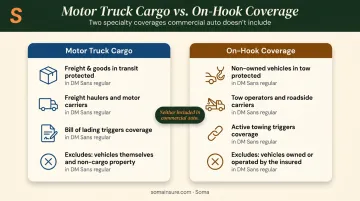

- Motor Truck Cargo Insurance protects freight or goods in the carrier's care, custody, and control while in transit

- On-Hook Coverage protects non-owned vehicles while being towed, hauled, or transported by your tow truck

- Neither is included in a standard commercial auto policy — both require separate purchase

- Freight haulers need Motor Truck Cargo; tow operators need On-Hook; some businesses need both

- The deciding factor is simple: what is your truck actually carrying?

Motor Truck Cargo vs. On-Hook Coverage: Quick Comparison

| Motor Truck Cargo | On-Hook Coverage | |

|---|---|---|

| What it protects | Goods/freight owned by a shipper or customer | Non-owned vehicles physically attached to or loaded on your tow truck |

| Who it's for | Freight haulers, trucking companies, for-hire carriers | Tow truck operators, roadside recovery services |

| When it triggers | When cargo is in the carrier's care, custody, and control during transport | While a vehicle is being towed or hauled |

| Common perils covered | Collision, fire, theft, vandalism | Collision, fire, theft, explosion, vandalism |

| Key exclusion | Doesn't cover the carrier's own property | Doesn't cover the operator's own vehicles |

| Included in commercial auto? | No | No |

Both coverages fill the same gap: the ISO Business Auto Coverage Form explicitly excludes property in the insured's care, custody, or control. Without these specialized policies, a damaged load or towed vehicle becomes an out-of-pocket loss — and those claims can reach six figures.

What Is Motor Truck Cargo Insurance?

Motor Truck Cargo Insurance is a legal liability coverage that protects a motor carrier against loss or damage to freight in their care, custody, and control. Under federal law — specifically 49 U.S.C. § 14706, the Carmack Amendment — carriers are liable to the freight owner for actual loss or damage to goods transported under a receipt or bill of lading. Motor Truck Cargo Insurance is what covers that liability.

In practical terms, coverage applies when cargo is lost, damaged, or stolen during loading, transit, or unloading. Coverage typically follows the bill of lading: if goods aren't documented on a shipping receipt, bill of lading, rate confirmation sheet, or contract of carriage, the policy likely won't cover them.

What It Covers in Practice

Common covered perils include:

- Accidents and collision

- Fire and vandalism

- Theft during transport

- Removal expenses and earned freight charges (policy-dependent)

Why Skipping It Is Costly

The financial stakes are real. According to CargoNet, the average value per cargo theft in 2025 was $273,990 — up 36% from 2024. That figure reflects theft alone, not physical damage from accidents or mishandling.

Beyond the dollar amount, a single uncovered claim can:

- Trigger a lawsuit from the shipper under the Carmack Amendment

- Damage long-term shipper relationships

- Cost the carrier contract renewals and future freight business

- Create a contractual compliance problem — Uber Freight requires at least $100,000 in cargo liability for FTL carriers, and most freight brokers set similar minimums

For most carriers, Motor Truck Cargo coverage is a contractual requirement. Freight brokers and shippers routinely include cargo minimums in their carrier agreements, and operating without it means losing access to loads.

Who Needs It

- Flatbed, dry van, refrigerated (reefer), and tanker carriers

- Car haulers transporting vehicles as freight

- Household-goods carriers (federally required to file cargo insurance evidence with FMCSA)

- Owner-operators not covered under a motor carrier's policy

- Any for-hire trucker operating under a bill of lading

Real-world example: A flatbed carrier hauls a load of industrial machinery. During a sharp turn, the load shifts and is destroyed. Motor Truck Cargo Insurance covers the value of the destroyed goods up to policy limits (minus the deductible). Without it, the carrier absorbs the full replacement cost — or faces a Carmack Amendment lawsuit from the shipper.

What Is On-Hook Coverage?

On-Hook Coverage (sometimes called on-hook cargo liability) protects non-owned vehicles from damage while they're being towed or hauled by your tow truck.

The coverage applies only while the vehicle is physically attached to your towing equipment — not before loading, and not once it's been stored at a facility.

This distinction matters. A common point of confusion is mixing up On-Hook with Garagekeepers Legal Liability:

- On-Hook applies during towing — while the vehicle is being hauled

- Garagekeepers applies after towing — when the vehicle is stored at a shop, lot, or service location overnight

The two coverages are sequential — each picks up where the other leaves off.

The Commercial Auto Gap

Standard commercial auto liability covers damage caused by your tow truck — not damage to the vehicle being towed. Without On-Hook, a customer's vehicle damaged during loading or transport becomes the operator's out-of-pocket problem — no standard commercial auto policy fills that gap.

Covered perils under On-Hook typically include:

- Collision

- Fire and explosion

- Theft

- Vandalism

Important Limitations

- Does not cover vehicles owned by the towing operator

- Does not apply to personal items inside the towed vehicle (that's a different coverage)

- Does not cover vehicles stored at a facility after towing (that's Garagekeepers)

A terminology quirk affects Texas and Virginia specifically: what most states call On-Hook Towing Insurance is labeled Garagekeepers Legal Liability in those two states — while what other states call Garagekeepers is referred to as Storage Location Insurance there. The terminology is inverted, which creates real confusion when operators move between states or shop coverage across markets.

Who Needs It

- Tow truck operators and roadside recovery services

- Auto club contractors and rotational towing services

- Auto salvage haulers

- Repossession companies

- Any operator contracted to tow non-owned vehicles

Real-world example: A towing company responds to an accident and winches a customer's SUV onto a flatbed. During loading, the vehicle rolls and sustains body damage. On-Hook Coverage pays for the repairs up to policy limits. Without it, the towing company writes the check.

Motor Truck Cargo vs. On-Hook Coverage: Which Do You Need?

The answer comes down to one question: what is your truck carrying?

- Hauling goods or freight for a shipper? → Motor Truck Cargo

- Towing or transporting someone else's vehicle? → On-Hook Coverage

- Both? → You may need both

Decision Framework

| Your Operation | Coverage You Need |

|---|---|

| Freight carrier operating under a bill of lading | Motor Truck Cargo |

| Required by brokers or shippers to carry cargo coverage | Motor Truck Cargo |

| Tow truck operator, roadside recovery | On-Hook Coverage |

| Vehicle repossession or salvage hauling | On-Hook Coverage |

| Towing business that also hauls freight or equipment | Both |

One nuance for car haulers: they typically use Motor Truck Cargo with auto-specific endorsements — not On-Hook. Progressive's auto-hauler coverage places transported vehicles under Motor Truck Cargo during loading, transit, unloading, and while waiting at terminals. On-Hook is designed for tow operations, not auto transport carriers.

Where Soma Fits In

Soma places trucking insurance for owner-operators, regional fleets, and long-haul carriers through carrier partners including Chubb, Progressive, Kemper, and Ascend. A single placement can cover motor truck cargo, physical damage, driver liability, trailer interchange, and more.

Soma also handles DOT and FMCSA filings as part of the trucking program, which matters for carriers who need to meet federal compliance requirements alongside their cargo coverage. For towing operators and businesses whose operations span both freight and vehicle recovery, Soma can place coverage across both lines — reducing the risk of gaps between policies.

Conclusion

Motor Truck Cargo and On-Hook Coverage protect fundamentally different things. One applies to the freight inside your trailer. The other applies to the vehicle attached to your tow hook. Relying on your commercial auto policy alone for either leaves real, uninsured exposure — especially if you're hauling freight or towing customer vehicles.

Review your current policies against the scenarios in this guide. If your coverage doesn't match your actual operations, Soma's Risk Management Team can assess your exposure, identify what's missing, and place the right coverage quickly. Submit a quote request through Soma's contact form — the team has handled thousands of trucking and complex commercial placements.

Frequently Asked Questions

What is on-hook liability coverage?

On-Hook Coverage protects damage to non-owned vehicles while they are being towed or hauled by your tow truck. It applies only while the vehicle is physically connected to or loaded onto towing equipment — not during storage. Without it, damage to a customer's vehicle during towing is the operator's uninsured liability.

Is motor truck cargo a liability coverage?

Yes. Motor Truck Cargo is a legal liability coverage protecting the motor carrier's obligation to the freight owner for loss, damage, or theft of goods in the carrier's care, custody, and control. That liability stems from the Carmack Amendment, which holds carriers responsible for actual loss to goods transported under a bill of lading.

Is on-hook coverage the same as motor truck cargo?

No, they cover completely different exposures. Motor Truck Cargo covers freight or goods being transported for a shipper; On-Hook covers non-owned vehicles being towed. Note that Texas and Virginia use the term "Garagekeepers Legal Liability" for what most other states call On-Hook Towing Insurance.

Do I need both motor truck cargo and on-hook coverage?

Most operators need only one. Freight haulers need Motor Truck Cargo; towing operators need On-Hook. If your business spans both — hauling freight and towing customer vehicles — you may genuinely need both coverages to avoid leaving one exposure unaddressed.

Does commercial auto insurance cover cargo damage or towed vehicles?

No. Standard commercial auto policies explicitly exclude property in the carrier's care, custody, or control. That exclusion covers both freight inside the trailer and vehicles being towed — making specialized Motor Truck Cargo or On-Hook policies necessary for any operator with that exposure.

What does motor truck cargo insurance not cover?

Common exclusions include cargo not listed on shipping documents, intentional acts, and losses from inherent vice, wear and tear, or ordinary leakage. Policies also typically exclude war, terrorism, and nuclear events. Review your specific policy exclusions and ask about endorsements for high-value or specialty commodities.