That gap — between what your property policy covers and what your business actually loses — is precisely what business interruption (BI) insurance is built to fill.

Restaurants face this exposure more acutely than almost any other business type. You can't serve food remotely. Revenue stops the moment the kitchen does, while obligations keep accumulating. This guide covers what BI coverage actually pays for, what it won't, how to size your coverage correctly, and what to do when a claim becomes necessary.

TL;DR

- BI insurance replaces lost net income and pays continuing fixed costs (rent, payroll, utilities) while a covered event keeps your restaurant closed.

- It's rarely included in standard property insurance. You need to add it as an endorsement or through a Business Owner's Policy (BOP).

- Floods, earthquakes, pandemics, cyberattacks, and voluntary closures are not covered under standard policies without specific endorsements.

- Coverage limits should reflect your peak-season revenue, all fixed costs, and a restoration timeline based on worst-case reality, not best-case assumptions.

Why Restaurants Are Especially Vulnerable to Business Interruptions

Most businesses can absorb a disruption with some combination of remote work, reduced hours, or temporary relocation. Restaurants can't. The moment the kitchen goes offline, revenue goes to zero — while obligations don't.

Fire Risk Is Higher Than You Think

According to NFPA data from 2018–2022, eating and drinking establishments in the US averaged approximately 15,000 fires per year, resulting in nearly $215 million in annual property losses. That frequency reflects something most restaurant owners already know instinctively: commercial kitchens run hot, operate under constant time pressure, and accumulate grease in ways that create real fire exposure.

Thin Margins Leave No Buffer

The National Restaurant Association reports that food and labor costs have each risen 35% since 2019, and pre-tax profit margins for independent restaurants typically sit around 5%. That leaves almost nothing in reserve to absorb even a short closure.

Disruptions Beyond Physical Damage

Physical property damage isn't the only closure trigger restaurants face. A single piece of failed equipment — a walk-in compressor, a hood suppression system, a gas line — can shut down service until repairs are complete. Other triggers include:

- 96% of operators reported supply delays or shortages of key items in a 2021 National Restaurant Association survey — a supplier failure can halt service with no property damage at all.

- Health authorities can shutter a restaurant on the spot following an inspection finding, regardless of how the kitchen looked the day before.

- Mandatory evacuations, road closures, or disaster cordon zones can cut off access to a physically undamaged location.

Each of these scenarios stops revenue cold — and none of them require a fire or a flood to trigger. That's precisely the gap business interruption insurance is designed to fill.

What Business Interruption Insurance Covers for Restaurants

BI coverage bundles several distinct protections into one policy. Understanding each component helps you identify gaps before a loss occurs.

Lost Business Income

This is the core function. When a covered peril forces closure, BI insurance replaces the net income the restaurant would have earned during the shutdown period. Insurers use historical financial records — typically one to two years of pre-loss income and expense data — to project what earnings would have been.

This is why clean, current bookkeeping isn't just good accounting practice. Restaurants with organized financial records consistently recover more and recover faster than those without.

Continuing Operating Expenses

Closing the doors doesn't stop the bills. BI coverage pays the fixed costs that keep accruing during a shutdown:

- Rent or mortgage payments

- Loan repayments

- Core employee payroll

- Minimum utility costs

- Insurance premiums

- Property taxes

Without this coverage, every closed day comes straight out of reserves or pushes you toward missed payments.

Extra Expense Coverage

Many policies include reimbursement for reasonable additional costs incurred to minimize the interruption. For restaurants, relevant examples include:

- Renting a temporary commissary or ghost kitchen space

- Expedited shipping costs for replacement equipment

- Advertising to notify customers of temporary relocation or reduced service

The intent is to offset the cost of staying operational, even partially, while repairs are underway.

Civil Authority Coverage

If a government authority orders an area closed — a mandatory evacuation, a road closure following a nearby disaster — this provision compensates for lost income even when the restaurant itself isn't physically damaged. The Insurance Information Institute notes civil authority coverage generally doesn't extend beyond two consecutive weeks, so it's designed for short-term access restrictions, not prolonged shutdowns.

Contingent Business Interruption

This covers income lost when a key supplier suffers a covered loss that disrupts their ability to serve you. If your primary food distributor experiences a warehouse fire and can't fulfill orders for three weeks, contingent BI can cover that revenue gap. It's particularly relevant for restaurants with single-source supplier relationships or those relying on a shared commissary kitchen.

What's Not Covered: Key Exclusions Restaurant Owners Must Know

Understanding exclusions may be more valuable than understanding what's covered. These are the gaps that cause the most financial pain.

The Physical Damage Requirement

Standard BI policies only activate when a covered peril causes direct physical damage to the insured property. Slow seasons, reputation damage from a bad review, staff walkouts, or an owner's decision to close temporarily — none of these trigger coverage. The damage must be sudden, unexpected, and caused by a covered event.

Flood and Earthquake Exclusions

Standard commercial property insurance excludes both floods and earthquakes, which means BI coverage tied to those policies has the same gaps. A restaurant that floods and can't operate for two months gets zero BI benefit under a standard policy. Restaurants in coastal, riverine, or seismically active areas need separate flood and earthquake policies to fill these gaps.

Pandemic and Virus Exclusions

COVID-19 produced the largest wave of restaurant BI litigation in history. As reported by Reuters in early 2023, every federal appellate court that addressed the issue ruled that commercial all-risk policies did not cover pandemic-related income losses — with 9 of 10 state high courts agreeing. The core ruling: government-ordered closures without physical property damage did not satisfy the coverage trigger.

The data tells the story clearly:

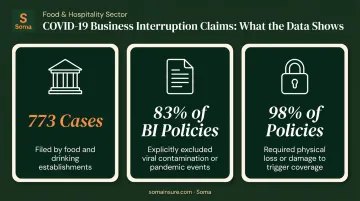

- The University of Pennsylvania's Covid Coverage Litigation Tracker recorded 773 cases filed by food services and drinking places — the highest of any industry. Most failed.

- A 2020 NAIC data analysis found 83% of BI policies explicitly excluded viral contamination or pandemic.

- 98% of policies required physical loss to trigger coverage — a bar pandemic closures couldn't meet.

Most insurers have since made these exclusions even more explicit.

Cyberattack-Related Closures

In April 2023, a ransomware attack on NCR's Aloha POS platform disrupted operations at restaurants across the country. Standard BI coverage provided no relief — there was no physical damage to the insured premises. As restaurants increasingly depend on digital ordering, payment processing, and reservation systems, a cyber event can effectively close the business.

Standard BI won't respond to that. A separate cyber liability policy — which can include business interruption from cyber events — is the right tool for this risk.

Voluntary Closures

Renovations, planned maintenance, and seasonal closures are excluded. If you shut down on your own terms — for any reason — there's no BI payout. Coverage only activates when an unexpected covered event forces your hand.

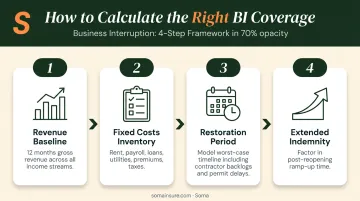

How to Calculate the Right Coverage Amount for Your Restaurant

Underinsuring is the most common BI mistake. Here's how to size coverage correctly.

Step 1: Establish Your Revenue Baseline

Calculate 12 months of gross revenue across all income streams: dine-in, takeout, delivery, catering, and private events. Don't rely on a simple monthly average.

If your restaurant earns 40% of annual revenue during a summer peak or holiday season, your coverage needs to reflect what a closure during those months would actually cost. An averaged-down figure will consistently underestimate peak-period loss.

Step 2: Inventory Your Fixed Costs

List every expense that continues regardless of whether you're open:

- Rent or mortgage

- Loan and equipment lease payments

- Core payroll (key staff you'd retain during a closure)

- Minimum utility costs

- Insurance premiums

- Property taxes

Your coverage limit needs to be sufficient to cover both projected lost net income and these ongoing obligations simultaneously.

Step 3: Model a Realistic Restoration Period

The period of restoration is the window during which BI benefits are paid — from the date of loss until the property is repaired and operational. Standard policies may cap this at 12 months, but real-world recoveries regularly exceed that timeline due to:

- Commercial kitchen equipment sourcing delays

- Contractor backlogs in post-disaster environments

- Building permit and health inspection timelines

- Supplier and staffing reconstitution

Model for the worst case. Contractor backlogs and permit delays compound fast — select your restoration period length with that reality in mind.

Step 4: Consider an Extended Period of Indemnity

Physically reopening doesn't mean you're immediately earning pre-interruption income. Rebuilding customer traffic, re-engaging regulars, and restoring online review scores takes time.

The extended period of indemnity endorsement covers income losses during this ramp-up phase. Standard BI policies include up to 60 days of extended business income after repairs are complete; endorsements are available in 30, 60, or 90-day increments beyond that to match how long your specific recovery will realistically take.

Customizing Your Policy for Restaurant-Specific Risks

Coverage Add-Ons Worth Considering

A standard BOP or basic BI endorsement won't address every restaurant-specific exposure. These additions are worth discussing with your broker:

Utility Interruption Endorsement A standard BI policy typically won't cover income loss from an off-premises power failure. If a grid outage spoils your walk-in inventory and halts all kitchen operations for three days, you're absorbing that loss without help. A utility services endorsement can extend BI coverage to include power, water, and communications outages originating outside your property.

Ordinary Payroll Endorsement — Understand the Trade-off Some policies offer an ordinary payroll exclusion endorsement that reduces premiums by removing payroll coverage for non-essential staff. The savings can be meaningful — but the trade-off is real. Restaurants that release trained kitchen and front-of-house staff during a closure often face a harder reopening:

- Longer ramp-up times before full service resumes

- Higher recruiting and onboarding costs

- Service quality gaps that hurt early post-reopening revenue

Weigh those costs against the premium reduction before opting in.

Cyber Liability with Business Interruption As noted earlier, standard BI coverage doesn't respond to cyberattacks. Some policies pair cyber liability with business interruption coverage for cyber events — worth adding for any restaurant processing customer payment data through digital systems.

A broker who understands hospitality operations can surface options a generalist will miss. Soma's hospitality program — placed through specialty markets including Markel, Nationwide, and Liberty Mutual — is built for restaurants, bars, and event venues, including operations that standard markets often decline. That access matters when you're trying to add endorsements a generic BOP won't even offer.

Filing a Business Interruption Claim: What to Do When the Kitchen Closes

Notify Your Insurer Immediately

Late notification is one of the most consistent reasons for claim denial or reduced payouts. Review your policy's notice provision now — before a loss occurs — so you know the required timeline and format. Many policies require formal notice within 30 to 60 days of the loss, and missing that window can void your claim entirely.

Document Everything from Day One

Insurers evaluating a BI claim will typically request:

- Two years of tax returns and financial statements

- Monthly profit-and-loss records

- Payroll records

- Utility bills and lease agreements

- Repair invoices and contractor communications

- Vendor correspondence documenting supply disruptions

Restaurants with clean, organized records recover faster and more fully. Gaps in financial documentation give adjusters room to undervalue the claim — and they will.

Work With Your Adjuster Proactively

The adjuster's job is to evaluate the claim and determine the payout. Treat every interaction as part of the record:

- Keep a written log of all conversations, including dates and what was discussed

- Confirm next steps in writing after each call or meeting

- If the claim is complex or contested, consider engaging a public adjuster or BI attorney — they're paid a percentage of the recovery, and they often secure significantly more than policyholders who go it alone

Frequently Asked Questions

Why should restaurants consider business interruption insurance?

Restaurants face higher-than-average closure risks from fire, equipment failure, and supply disruption, combined with profit margins of around 5% that leave almost no cash reserve. Fixed costs — rent, payroll, loan payments — keep accruing the moment revenue stops, making BI insurance a financial survival tool.

What qualifies for business interruption insurance?

The standard trigger is direct physical damage to the insured property from a covered peril — fire, storm, vandalism, and similar events. Events without physical damage, including pandemics, voluntary closures, and most cyber incidents, typically do not qualify under standard policies.

Is business interruption insurance included in a standard restaurant insurance policy?

No. BI coverage is generally not automatic — it must be added as an endorsement to a commercial property policy or bundled into a Business Owner's Policy (BOP). Coverage terms, limits, and waiting periods vary significantly by insurer.

What is the waiting period in a business interruption policy?

Most BI policies have a waiting period of 48 to 72 hours after the loss before benefits begin. Some policies use a dollar deductible instead.

Does business interruption insurance cover cyberattacks or utility outages?

Standard BI policies exclude losses from cyberattacks and off-premises utility failures unless specific endorsements are added. Restaurants using POS systems or digital ordering should ask their broker about cyber liability coverage with BI and a utility services interruption endorsement.

How do I calculate how much business interruption coverage my restaurant needs?

Start with 12 months of gross revenue, add your continuing fixed costs (rent, payroll, loan payments), and set a restoration period based on a realistic worst-case repair timeline — factoring in equipment lead times, contractor availability, and permitting delays. Ask your broker whether an extended period of indemnity endorsement fits your revenue volume.