The path to becoming a commercial truck insurance agent involves three things: getting your Property & Casualty license, building trucking-specific knowledge, and connecting with the right carrier markets. This guide walks through each step — including what it actually takes to build a sustainable book of business in this niche.

TL;DR

- A Property & Casualty license is all you need to sell commercial truck insurance — no separate trucking license exists

- Pre-licensing hours vary significantly by state (20 hours in California, 90 hours in New York)

- Trucking policies carry some of the highest premiums in commercial lines, with the average P&C commission rate at 11.5% across all lines

- The US has nearly 580,000 active motor carriers, giving specialists a large and stable client base

- New agents without direct carrier appointments can access trucking markets through wholesale brokers and MGAs

What Is a Commercial Truck Insurance Agent?

A commercial truck insurance agent sells policies to trucking businesses — owner-operators, fleet companies, and freight carriers — and must understand the federal regulatory environment that governs them. That means knowing FMCSA rules, DOT authority requirements, and how Form MCS-90 endorsements work.

Captive vs. Independent

There are two ways to operate:

- Captive agents work for a single carrier with a limited product range

- Independent agents and brokers can shop multiple carriers to find the best fit

The independent route matters more in trucking than almost any other niche. Many trucking risks are genuinely hard to place — new ventures, drivers with violations, specialty commodities — and having access to multiple markets is often the only way to get a client covered at all.

What Makes Trucking Different

That complexity also explains why trucking isn't just another commercial auto account. The regulatory and underwriting requirements are in a different category entirely:

- Federal filings are mandatory — every active trucking policy needs Form MCS-90 endorsements, DOT authority documentation, and compliance with FMCSA financial responsibility rules under 49 CFR Part 387

- Liability minimums are much higher than standard commercial auto — $750,000 for general freight, up to $5,000,000 for certain hazmat categories under 49 CFR 387.9

- Operational variety — long-haul, local cartage, refrigerated, hazmat, and owner-operators each require different coverage structures

- Underwriting is genuinely difficult: commercial auto loss ratios hit 77.58% in 2024, which is why carriers price and scrutinize these accounts so carefully

Why Specialize in Commercial Truck Insurance?

The Market Is Massive

The scale of the trucking market speaks for itself:

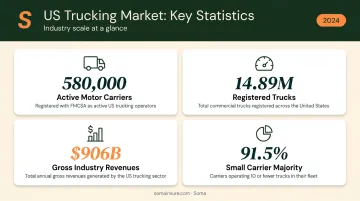

- 580,000 active US motor carriers registered with FMCSA as of June 2025

- 14.89 million single-unit and combination trucks registered in 2023

- Trucks moved 11.27 billion tons of freight in 2024, generating $906 billion in gross revenues

- 91.5% of carriers operate 10 or fewer trucks — meaning the market is dominated by small operators who need an agent, not an internal risk manager

That last point matters most. Small owner-operators and micro-fleets are clients who rely on an agent for guidance — they're not going direct.

The Earnings Case

Commercial lines agents consistently out-earn their personal lines counterparts. Independent agencies wrote 87.2% of commercial lines premiums in 2024 versus 39% for personal lines — reflecting where the money flows in this channel. With the average P&C commission running at 11.5%, and trucking premiums running high due to federal minimums and liability exposure, each policy generates meaningful income.

Run the math: 50 trucking clients, each paying $8,000 in annual premium, at 11.5% commission equals roughly $46,000 in annual commissions from that book alone. Add fleet accounts or grow to 100 clients, and you're looking at six figures from trucking coverage exclusively.

Less Competition, Stronger Retention

Most generalist agents avoid trucking. The regulatory complexity, DOT compliance requirements, and hard-to-place risks push most agents toward easier lines — which keeps the field less crowded for specialists. Agents who commit to the niche face less competition and, once they've earned a trucking client's trust, tend to keep them.

Trucking renewals require proactive attention — reviewing loss runs, checking CSA scores, adjusting coverage as fleets grow. That hands-on work is what separates a trusted advisor from a policy vendor.

Trucking Insurance Coverages Every Agent Must Know

Understanding this suite is what separates a trusted advisor from someone who just processes renewals.

Primary Auto Liability

The foundational, federally mandated coverage. FMCSA minimum limits under 49 CFR 387.9:

| Operation Type | Minimum Limit |

|---|---|

| For-hire carriers, general freight (GVWR 10,001+ lbs) | $750,000 |

| Oil, hazardous waste, certain hazmat | $1,000,000 |

| Specified high-risk hazmat categories | $5,000,000 |

No trucking operation can legally run without meeting these thresholds. The MCS-90 endorsement is attached to the motor carrier's liability policy — not issued per vehicle — and serves as the federal backstop ensuring payment to injured members of the public.

Physical Damage

Covers the truck and trailer themselves (comprehensive and collision). Lenders require it on financed equipment, and values vary widely based on age, type, and fleet size. This is often where owner-operators underinsure — a costly mistake when a $150,000 rig gets totaled.

Motor Truck Cargo

Covers freight in transit, defined as an inland marine form covering loss of property either by common carrier or on the insured's own vehicles. Coverage limits and exclusions vary by commodity. Shippers and freight brokers routinely require minimum cargo limits in their contracts — agents need to check those requirements at intake.

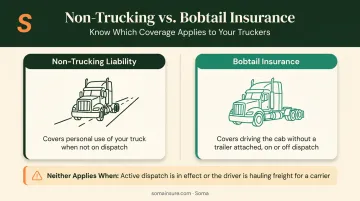

Non-Trucking Liability (Bobtail Insurance)

These two terms get conflated constantly — knowing the difference matters at the point of sale:

- Non-trucking liability covers an owner-operator using the truck for personal tasks — not while dispatched or hauling for a carrier

- Bobtail insurance specifically covers driving without a trailer

- Neither applies when the driver is operating on the motor carrier's behalf or hauling property

Explaining this distinction clearly at the point of sale prevents coverage gaps and builds credibility.

Additional Coverages to Know

- Occupational accident insurance — a workers' comp alternative for owner-operators classified as independent contractors

- Trailer interchange — covers non-owned trailers under a trailer interchange agreement

- General liability — covers premises and operations exposure beyond the vehicle itself

Agents who can walk a prospect through all of these — not just the primary liability line — earn the trust that turns a one-policy account into a long-term book.

How to Become a Licensed Commercial Truck Insurance Agent: Step-by-Step

Step 1: Obtain Your Property & Casualty License

There is no separate trucking insurance license. Commercial truck insurance falls under the standard Property & Casualty license issued by each state. The process:

- Meet eligibility requirements — typically 18+ years old

- Complete pre-licensing education — hours vary significantly by state:

- California: 20 hours property + 12 hours ethics

- Illinois: 20 hours per line of authority

- Texas: at least 40 hours for general lines P&C

- New York: 90 hours for P&C

- Pass the state licensing exam — Kaplan reports a 94% first-time pass rate for students using structured exam prep

- Complete background check and fingerprinting

- Submit your license application — states generally take 7–10 days to review after submission

Check your state's Department of Insurance or NIPR for exact requirements. Don't assume the hours — they range from 20 to 90 depending on where you operate.

Step 2: Build Trucking-Specific Knowledge

A P&C license gets you in the door. Becoming a trucking specialist requires a separate layer of industry knowledge:

- FMCSA regulations and DOT authority requirements

- How MCS-90 endorsements function in practice

- How underwriters rate trucking risks (years in business, safety scores, commodity type, radius of operation)

- The American Trucking Associations (ATA) — their publications and events are among the best resources available

The fastest way to accelerate here is talking directly to underwriters who specialize in commercial transportation. They'll tell you what makes a risk appealing or problematic more efficiently than any textbook.

Step 3: Get Appointed With Carriers or Partner With a Wholesale Broker

Direct carrier appointments work for established agents with a proven book. Standard carriers have production requirements that make it difficult for new agents to get appointed for trucking specifically.

The wholesale broker/MGA route is the practical path for agents starting out. Wholesale brokers and MGAs that specialize in commercial transportation provide access to markets — including hard-to-place accounts — without requiring individual carrier appointments.

Soma places complex and hard-to-insure commercial trucking risks — including new ventures, drivers with violations, specialty commodities, and hazmat haulers — through carrier partners including Chubb, Progressive, Kemper, and Ascend. DOT and FMCSA filings are handled in-house, which matters when clients need regulatory compliance alongside their coverage.

For agents who need broader market access quickly, working with a wholesale brokerage that already holds these carrier relationships is a more direct path to writing business than building individual appointments one by one.

How to Build and Grow a Commercial Trucking Book of Business

Pick a Starting Niche

Trucking is not monolithic. Start focused:

- Owner-operators (high volume, simpler accounts)

- Regional fleets (more complex, larger premiums)

- Refrigerated carriers or specialty commodities

- A specific geographic corridor or freight type

Becoming the known expert in one segment is more valuable than being a generalist across all of them.

Network Where Truckers Actually Are

- ATA events and regional trucking association meetings

- Freight broker conventions and logistics industry gatherings

- Relationships with dispatchers — they interact with owner-operators daily and can be strong referral sources

- Truck stops and fuel stop bulletin boards (genuinely effective for owner-operator outreach)

Go Beyond the Policy

The most effective truck insurance agents understand DOT compliance pressures, driver shortage issues, and rising equipment costs. Showing up at renewal with knowledge of what's changed — new drivers, new routes, a recent inspection score — signals that you're actually paying attention. Clients notice. That's what generates referrals.

Retain Clients Through Proactive Service

Trucking renewals are not automatic. Rates shift, carrier appetite changes, and clients who feel ignored shop around. Agents who build higher retention rates consistently do a few things right:

- Review coverage proactively before each renewal cycle

- Flag regulatory changes before clients ask about them

- Advocate for clients during claims rather than going silent

One retained fleet account is worth more than five new owner-operators you have to replace next year.

How Much Do Commercial Truck Insurance Agents Make?

According to the Bureau of Labor Statistics, insurance sales agents earned a median annual wage of $60,370 in May 2024, with the top 10% earning more than $135,660. These figures cover the broader occupation — not trucking specifically — but they establish the baseline.

Commercial lines agents generally outperform that median due to higher premium accounts. With the average P&C commission at 11.5%, trucking's high premium levels translate directly to larger per-policy earnings.

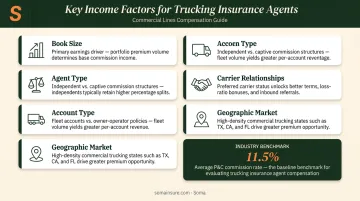

Key income factors:

- Book size — the primary driver; larger books compound quickly

- Independent agents typically earn higher commissions than captive agents, but carry their own overhead

- Fleet accounts generate more revenue per client but take longer to close than owner-operator policies

- Trucking specialists with established carrier relationships command better terms and more referrals

- High-freight-volume states like Texas, California, and Florida offer greater client density

Beyond individual income, the field itself is expanding. Employment in insurance sales is projected to grow 4% from 2024 to 2034, with roughly 47,000 annual openings. Trucking specialists enter that market with an edge most generalists lack: deep familiarity with a high-premium, high-complexity segment that takes years to learn.

Frequently Asked Questions

How much do commercial truck insurance agents make?

Insurance sales agents earned a median of $60,370 annually in May 2024, with the top 10% exceeding $135,660. Agents focused on trucking — where premiums are substantially higher than personal lines — tend to land toward the upper end of that range as their book grows.

Is being a commercial truck insurance agent worth it?

For agents who commit to learning the niche, yes. Trucking offers higher premiums per account, less competition from generalist agents, and strong retention once clients trust you. Most specialists report that a focused first 12–18 months pays dividends for years after.

What license do you need to sell commercial truck insurance?

A Property & Casualty insurance license issued by your state. There's no separate trucking-specific license — commercial truck insurance falls under the standard P&C line of authority. Requirements vary by state, so check your state's DOI or NIPR for specifics.

How long does it take to become a commercial truck insurance agent?

The licensing process itself takes roughly 2–8 weeks, depending on your state's pre-licensing hours and exam scheduling. Building enough trucking-specific knowledge to operate confidently as a specialist takes additional months of focused learning beyond the exam.

What types of coverage does a commercial truck insurance agent sell?

Core coverages include primary auto liability (federally mandated), physical damage, motor truck cargo, non-trucking/bobtail liability, and occupational accident insurance. The specific combination depends on whether the client is an owner-operator, regional fleet, or long-haul carrier.

Do I need trucking industry experience to become a truck insurance agent?

No prior trucking experience is required to get licensed. Agents who learn FMCSA regulations, DOT compliance, and how trucking operations run will consistently outperform those who treat trucking accounts like standard commercial policies.