The forces driving this complexity are hitting simultaneously. Tariffs are pushing material costs higher. Severe weather events are reshaping deductible structures. Underwriters are scrutinizing project-specific risk controls more than ever. And a wave of MGA entrants has fragmented the market in ways that make carrier selection genuinely consequential.

This article breaks down what's actually happening in the 2025 builders risk market, what it means for coverage terms, and what contractors and developers should be doing right now to protect their projects.

TLDR: Key Takeaways

- Rates are softening in low-risk segments, but CAT-exposed and water-sensitive projects face tighter terms and higher deductibles

- Tariff-driven material cost increases are making static policy valuations dangerous—underinsurance is a real and growing risk

- On-site controls (IoT sensors, water shutoff systems) are now standard underwriter questions before binding coverage

- Submission quality directly affects the terms you receive—incomplete documentation leads to worse outcomes

- A specialized broker with multi-carrier access compresses weeks of market shopping into days

The Builders Risk Market in 2025: Growth Amid Uncertainty

The builders risk sector has grown into an $8.75 billion market—and according to a Munich Re analysis, the long-term trajectory remains strong. The catch: conditions in 2025 are anything but uniform.

A Split Market, Not a Uniform One

The headline story in H1 2025 is capacity expansion. New carrier and MGA entrants have increased available capacity, and according to WTW's Insurance Marketplace Realities 2025, construction project insurance rates are stabilizing—with flat to modest discounts available for best-in-class risks. Amwins similarly reports that markets were eager to write new business after capacity increased significantly over the prior 12 months.

Demand is diverging sharply, though. Multifamily construction starts fell 25% in 2024 to approximately 355,000 units—a meaningful drag on overall activity.

Data centers, semiconductor plants, infrastructure, and large public works projects have picked up the slack. Contractor backlogs are holding near 8.5 months, according to Construction Dive reporting on ABC data.

Regional Variation Matters

The market experience differs substantially by geography:

- Florida and Gulf Coast: Conditions have improved meaningfully compared to recent years, with more capacity available and competitive deal flow returning—though catastrophe sublimits remain a feature of most placements

- Louisiana: Still difficult, largely due to legal and litigation-related concerns

- West Coast: Continued pressure from high replacement cost valuations and CAT exposure (wildfires, flooding)

- Northeast and Midwest: Competitive conditions have returned more quickly

The Quota-Share Shift on Large Projects

Large, complex projects in the $400–$600 million range that previously required a single carrier to absorb the full risk are now increasingly placed on quota-share arrangements, spreading exposure across multiple insurers. The shift reflects the scale of modern construction—and carriers' clear preference for distributed risk at the high end of the market.

Key Forces Reshaping Builders Risk Coverage

Tariffs, Inflation, and Valuation Risk

Material cost volatility is creating a specific and underappreciated risk for contractors: underinsurance. When a project's insured value is locked in at the start of construction and costs spike mid-build, the gap between the policy limit and actual replacement cost becomes the contractor's problem.

ABC reports that tariffs drove construction materials prices up 2.8% in 2025. AGC data shows two in five contractors have raised prices in response to tariff-related cost increases on steel, aluminum, and other key materials.

Carriers are paying attention. Gallagher's late 2025 market update notes that elevated material and labor costs have made many insured property values outdated, with underwriters actively scrutinizing agreed value and replacement cost terms.

What this means practically:

- Static, completed-value assumptions set at project inception leave contractors exposed to underinsurance gaps

- Insurers want to see general conditions costs included in submitted values

- Extended timelines (projects running 30+ months instead of 24) compound the exposure

Price escalation clauses in construction contracts (provisions that adjust contract price based on objective cost metrics) are now relevant to underwriters, not just project owners. Insurers want to see these provisions in place as evidence that cost-increase risk is being actively managed rather than ignored.

Catastrophe Exposure and Weather-Related Losses

Material cost risk is only part of the picture. Severe weather has become an equally dominant loss driver in builders risk, and the 2024–2025 data makes the trend hard to argue with. NOAA recorded 27 confirmed billion-dollar weather and climate disaster events in 2024. Globally, severe convective storms generated $61 billion in insured losses in 2025 — the third-highest total on record for that peril category.

The underwriting response has been structural, not just pricing-related:

- Named-storm deductibles on coastal projects can run into millions of dollars on large builds

- Water damage deductibles of $500,000 to $1 million are common on larger projects

- CAT-related sublimits are being applied not just on Gulf Coast projects but increasingly on high-value projects nationwide

The geographic scope of CAT underwriting scrutiny has expanded well beyond the Gulf Coast. Projects in regions with flooding, hail, or wildfire exposure are now subject to the same elevated deductibles and sublimits that once applied only to coastal builds — a shift contractors in those markets may not yet have priced into their risk assumptions.

How Underwriting Is Changing: Higher Deductibles and Tighter Terms

The most important shift in the 2025 builders risk market isn't happening in the rate column. It's happening in the structure of policies themselves.

From Premium Adjustments to Structural Changes

Underwriters are increasingly managing exposure through:

- Higher deductibles and more granular sublimits

- Project-specific review of risk controls before binding

- More detailed valuation requirements at submission

- Tighter terms on water damage, even when base premiums stay flat

CRC Group's 2025 property market data confirms that frame non-CAT builders risk rates have continued to decline, with markets willing to reduce water damage deductibles for well-documented risks. For large towers, data centers, and CAT-exposed projects, though, project-specific placements face more volatile terms and heavier documentation burdens.

The Self-Insurance Reality of High Deductibles

When deductibles reach six figures, the insured is effectively self-funding the first loss. That changes the economics of risk management entirely — contractors can no longer rely on post-loss recovery for the most common damage categories.

A water intrusion event on a large project with a $750,000 deductible doesn't become an insurance claim. It becomes an internal financial event.

Water Damage Is Getting Specific Attention

Insurers are now asking targeted, project-specific questions before binding coverage:

- How are temporary water systems isolated when work stops?

- Is overnight monitoring in place?

- How quickly can shutoff protocols be executed if a leak is detected?

Underwriting has moved from retrospective claims processing to pre-loss risk qualification. Underwriters treat contractors with documented protocols and installed systems as materially lower risks than those without.

Technology's Growing Role in Risk Assessment

Loss prevention technology now directly shapes builders risk underwriting decisions—affecting pricing, available terms, and maximum foreseeable loss calculations on complex projects.

IoT and Water Monitoring

Insurers are now distinguishing between contractors who have real-time monitoring systems in place and those who don't. IoT sensors for water flow detection, heat monitoring, and site access are becoming part of how underwriters assess maximum foreseeable loss on complex projects.

The impact can be significant. According to Munich Re's analysis, documented water controls can move a project's maximum foreseeable loss calculation from $20 million down to $1 million—a reduction that directly affects pricing and available terms.

Technology platforms specifically addressing this include:

- Water flow monitoring and automated shutoff systems that can trigger within minutes of a detection event

- Deductible buy-down programs tied to technology implementation, allowing contractors to reduce high water damage deductibles through demonstrated controls

- Data center-specific builders risk solutions (Zurich recently launched a product with operational property and weather parametric features for data center builds)

The Broader Risk Engineering Picture

Beyond water controls, underwriters are watching how contractors adopt AI-powered construction management platforms, digital twins, and predictive analytics tools. These aren't yet underwriting requirements, but sophisticated insurers are using them to distinguish higher-quality risks on complex projects.

Contractors using these tools are building a documentation trail that supports better coverage terms—even if the direct pricing impact is still emerging. Key tools gaining underwriter attention include:

- AI-powered construction management platforms that flag schedule and safety risks in real time

- Digital twins that provide ongoing site visibility and loss scenario modeling

- Predictive analytics tools that document proactive risk management decisions

What Contractors and Developers Should Do Now

Start Risk Planning Before Financial Close

Risk management planning — site-specific flood and wildfire exposure review, water mitigation protocols, monitoring system installation — needs to happen during project design, not at the administrative stage just before funding closes.

Underwriters use granular data: flood zone designations, wildfire maps, storm histories, and elevation data. The more of this documentation that's ready at submission, the better the outcome.

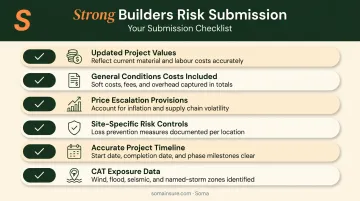

Invest in Submission Quality

Incomplete submissions are one of the most consistent sources of poor coverage outcomes. Gallagher's late 2025 market update specifically notes that firms with strong documentation and QA/QC oversight receive preferred pricing and retention terms.

A strong submission includes:

- Updated project values that reflect current material and labor costs

- General conditions costs properly included in insured values

- Evidence of price escalation provisions in the construction contract

- Site-specific risk controls (monitoring systems, shutoff protocols, security)

- Accurate project timeline, including any anticipated extensions

- CAT exposure data (flood zone, wind zone, proximity to water)

Work With a Broker Who Knows This Market

The builders risk market's fragmentation—with MGA entrants, quota-share structures, and segment-specific pricing—means that carrier selection has real consequences. A broker without deep market relationships may get quotes from three or four markets. A specialized broker with access to hundreds of carrier partners can find the right fit for projects that don't fall neatly into standard appetites.

Soma places builders risk coverage for general contractors, subcontractors, specialty trades, and developers through carriers including Chubb, Liberty Mutual, and Kinsale. Submissions move quickly — no waiting weeks while files sit in underwriting queues — across the full range of construction exposures: builders risk, contractor liability, installation floater, completed operations, and wrap-up programs (OCIP/CCIP).

For complex or CAT-exposed projects, simultaneous access to multiple carrier markets is often the only way to find competitive terms.

Frequently Asked Questions

How much does builder's risk insurance cost?

Builders risk premiums vary based on project type, location, construction materials, coverage extensions, and current market conditions. There is no standard benchmark rate—costs depend heavily on CAT exposure, project complexity, and the specific terms required. Speak with a specialized broker to get an accurate indication for your project.

Who typically buys builder's risk insurance?

Either the property owner or the general contractor can purchase the policy, depending on what the construction contract specifies. Lenders and AIA contract documents commonly require the owner to carry all-risk coverage, and the cost is typically passed through to the owner regardless of who holds the policy.

Does builder's risk insurance cover collapse?

Most builders risk policies are written on an all-risk basis and can cover collapse if caused by a covered peril such as wind or fire. Collapse resulting from faulty workmanship, design defects, or earth movement is typically excluded—policy language varies, so confirm with your broker before assuming collapse is covered.

Is builder's risk insurance required by law?

Builders risk is not generally required by federal or state law. It is, however, commonly required contractually—by lenders, government contracts, FHA/HUD loan programs, and standard owner-contractor agreements. On any financed or formally contracted project, the absence of coverage will typically halt the deal.

How are tariffs and inflation affecting builder's risk insurance in 2025?

Rising material costs mean policies can become undervalued mid-project if insured values aren't updated. Carriers and contractors are responding with price escalation clauses and more frequent revaluations—submitting accurate values at inception and updating them as costs change is now essential to avoiding an underinsurance gap at claim time.